Xi wants bigger returns, fewer headaches from African debt deals

When Chinese President Xi Jinping welcomes African leaders to Beijing this week, he’ll be holding a smaller checkbook and will have a clearer sense of what China wants in exchange: bigger returns and fewer headaches.

From Angola to Djibouti, for over a decade, China poured more than $120 billion of government-backed loans through its Belt and Road Initiative to build hydropower plants, roads and rail lines across the continent — as well as unparalleled influence. Those relationships helped Beijing lock down access to energy and minerals, while providing an outlet for its pent up industrial capacity.

But the infrastructure and diplomacy also came with accusations of debt traps, exploitation and corruption, charges that were bolstered when a wave of debt distress swept Africa in recent years and three countries defaulted, sparking lengthy restructurings. Some projects, like an unfinished $3.8 billion railway in Kenya that ends in an empty field, seemed to epitomize the failed promise of the BRI.

Despite those problems, the parade of African leaders arriving in Beijing for the ninth Forum on China-Africa Cooperation starting Wednesday attests to China’s role as the continent’s dominant foreign economic power. It’s the first such summit in Beijing since 2018, and it’s the biggest diplomatic event Xi is hosting this year, with participants expected to include Nigerian President Bola Ahmed Tinubu, Rwandan President Paul Kagame and South African President Cyril Ramaphosa.

Heading into the gathering, both sides expect the close ties forged by Beijing’s largess to continue. The difference now is that Xi, struggling to address his nation’s economic slowdown, is shifting China’s focus toward more opaque, public-private partnerships that can generate better returns while deflecting more of the blame if things go wrong.

“The heady days of big lending are done,” said Joshua Eisenman, a professor at the University of Notre Dame who studies China-Africa relations. “What comes next won’t be as big as before and it won’t be as grandiose. It’s going to be more profitable.”

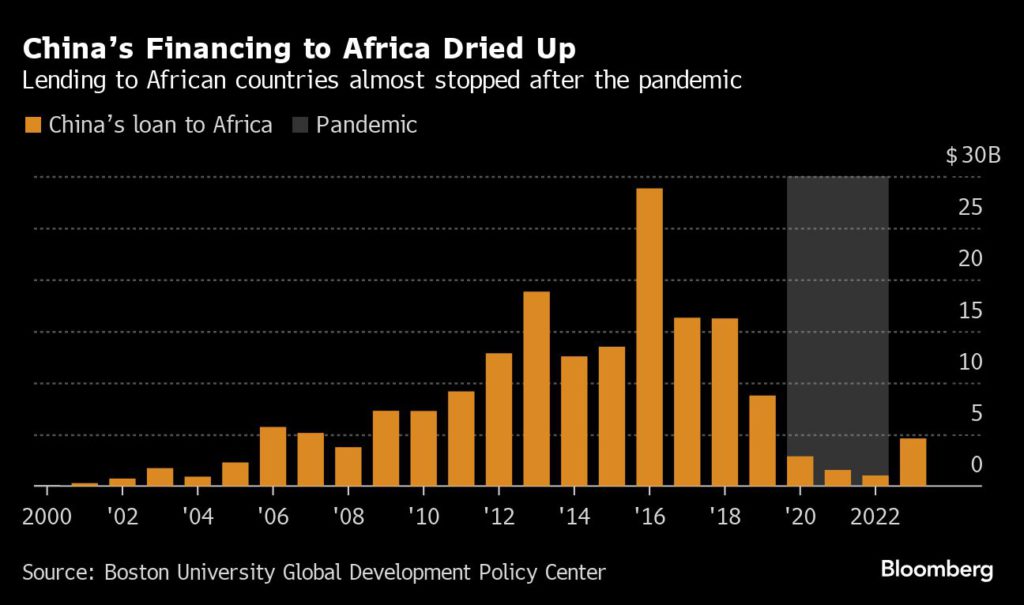

China’s traditional lending to Africa through its state-run policy banks exploded from $98.7 million in 2000 to a high of $28.8 billion in 2016, according to Boston University’s Global Development Policy Center, making it the world’s biggest bilateral creditor to Africa. Those figures declined in the following years and then plummeted during the pandemic before climbing to $4.6 billion last year.

Throughout that period, Beijing also lent through its commercial banks — but the balance is set to tip much further toward those profit-generating loans in the coming years. Some projects that typify China’s new approach include a $20 billion iron ore mine and railway in Guinea, a $5 billion oil pipeline in Uganda and Tanzania and a $400 million cash-for-oil loan in Niger that the military regime says it needs to “run the country.”

Zambia’s foreign ministry last week announced that President Hakainde Hichilema would be in Beijing to witness the signing of an investment deal to revitalize the 1,160-mile (1,870 km) Tazara railway, originally built in the 1970s as part of China’s first major aid project in Africa, connecting Tanzania and Zambia. Officials from the two nations have said little about how the $1 billion Tazara deal is structured, but it’s expected to rely on a public-private partnership model instead of public debt from one of China’s state-run banks.

African governments flocked to China in the 2000s in part because there were few options to get funding for the kind of major infrastructure they sorely needed. They also appreciated how China’s loans came without the environmental, human rights and other conditions that organizations like the World Bank and International Monetary Fund traditionally impose.

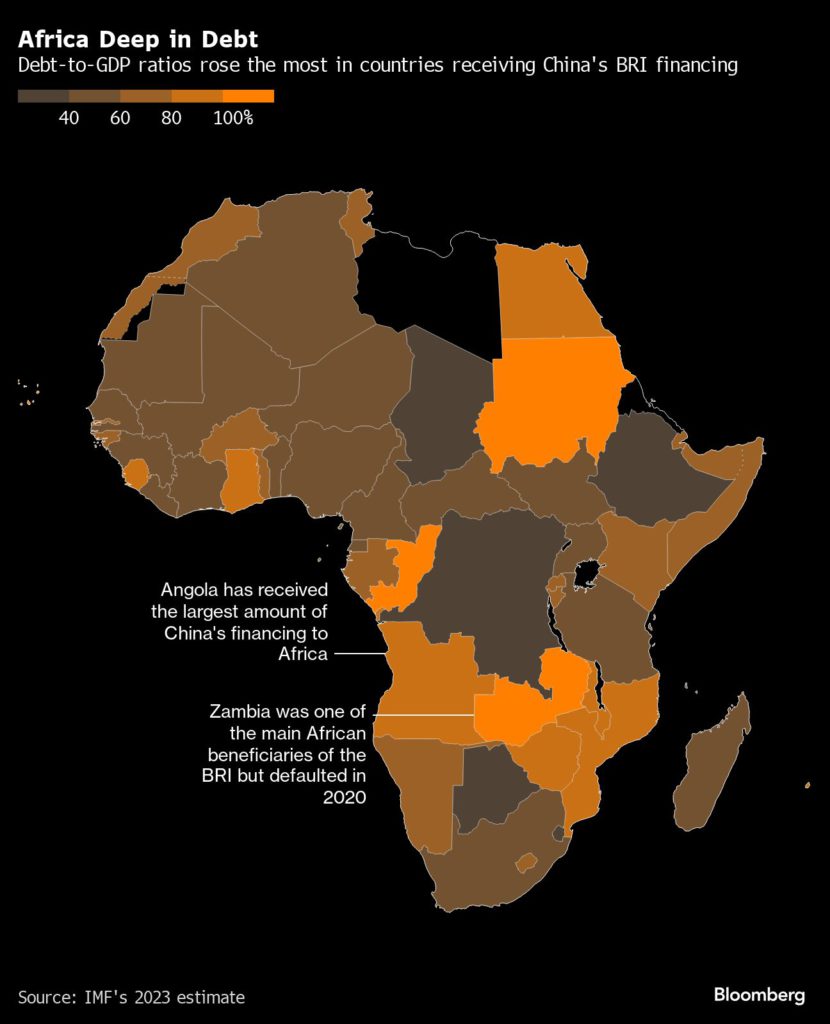

But the mounting debt soon began taking a toll on nations’ budgets, and many of the China-backed projects didn’t live up to expectations, a process exacerbated by the Covid-19 pandemic. When Zambia defaulted in 2020, the crisis put renewed scrutiny on China’s role in financing African nations. Ghana followed suit, while more than a dozen other African countries remain at high risk of debt distress. Angola took the most Chinese debt and now owes the country about $17 billion, more than one-third of all its external debt.

Some of the projects have been seen as successes. The $2 billion Kafue Gorge Lower Hydropower Station in Zambia — largely financed by the Export-Import Bank of China and the Industrial and Commercial Bank of China — is one example. The $1.5 billion expansion of the Hwange hydropower project in Zimbabwe, which has helped ease nearly daylong power outages in the country, is another.

But economists largely agree that with Chinese backing, many African nations overextended themselves. Some projects — such as an $823 million light rail project in Nigeria’s capital, Abuja — appear abandoned or barely functioning. Nigeria spends $50 million a year to pay off its loans for that project. During a visit to the rail line’s facilities last year, train cars sat locked away, cavernous stations were empty and the VIP lounge was full of bat and bird droppings.

After Zambia defaulted, a deal to restructure about $3 billion of debt nearly foundered as the Paris Club and China struggled to agree with fund managers on a deal that would distribute losses comparably. Talks over another $3.4 billion in debt, led by China Development Bank and ICBC, continue.

“I see China going through a learning process,” said Huang Yufan, a fellow at the China-Africa Research Initiative at the Johns Hopkins School of Advanced International Studies. “They realize the way they lent before doesn’t work anymore. They realize these governments can default and that they’re quite risky.”

That doesn’t mean Beijing is backing away.

China’s new strategy focusing on public-private partnerships allows cash-strapped African governments to continue borrowing without adding to their officially-declared sovereign debt.

Guinea’s $20 billion Simandou iron ore mining project is another example of the new model. The world’s biggest steelmaker, China Baowu Steel Group Corp., and aluminum producer Aluminum Corp. of China Ltd. are leading investors, along with Australia’s Rio Tinto Group. Chinese state firms control more than 40% of the shares across the pair of consortia developing the complex, while Guinea’s government holds a 15% stake.

The Simandou partners aim to produce 120 million tons of high-grade iron ore a year during the first phase, a volume that could exacerbate a market surplus and deliver greater power over pricing to the project’s largest consumer: China.

In central Africa, the Democratic Republic of Congo announced an agreement with China to build $7 billion in infrastructure by 2040, backed by the proceeds of a cobalt-and-copper mining joint venture known as Sicomines. The deal is a revamp of a 2008 resources-for-infrastructure agreement financed by the Export-Import Bank of China.

Sicomines was exempt from nearly all taxes and started producing billions of dollars’ worth of metal annually. But over 14 years, Exim Bank delivered only a portion of the infrastructure financing it promised and Congolese authorities said overbilling by Chinese contractors and local officials was rampant.

Under the new deal, the tax exemptions remain and the Chinese partners have linked infrastructure payments to the price of copper. If the price falls below $8,000 per ton, just under the average for the past five years, the payments decline. Payments are eliminated altogether if the price falls beneath $5,000.

In the end, the way many of these new deals are structured risks saddling future African governments with billions of dollars in less-transparent debt, says Brad Parks, executive director of AidData, a think tank at the College of William & Mary.

“What they’re doing is a lot of creative accounting to still borrow but through much more opaque mechanisms,” said Parks.

But the “willingness for more creativity” in financing projects “is a good thing” because it allows countries to still build critical infrastructure, said Hannah Ryder of Development Reimagined, a China-Africa focused think tank with offices in Nairobi, Beijing and London.

Such partnerships can still pose problems. Eric Lautier, the IMF representative in Zambia, warns of a “fiscal illusion” if there are clauses like minimum revenue guarantees that benefit creditors regardless of the project’s success.

“All infrastructure projects are risky by nature, and PPPs are no exception,” Lautier said of the public-private partnerships. “When not properly managed, they can pose significant fiscal risk.”

American officials believe Chinese policy banks overextended themselves and worry about the opacity of the new arrangements, according to people familiar with US policy.

Beijing disagrees. “The conclusions of ‘opaqueness’ and ‘high-costs’ are purely speculative,” China’s foreign ministry said in a statement. “China’s financing cooperation with Africa has always followed international rules, the principle of openness and transparency, and local laws and regulations.”

As African leaders arrived in Beijing ahead of the formal start of the summit, Xi began a long series of bilateral meetings in which he hit familiar themes. Welcoming Democratic Republic of the Congo President Felix Tshisekedi to the Great Hall of the People, he promised “high quality development” and touted “Chinese-style modernization.” He told Mali’s interim President Colonel Assimi Goita that China would continue to encourage its firms to invest in the nation, but asked its government to ensure their security.

Countries like the UAE, Saudi Arabia and Qatar filled some of the void left by China’s reduced largess in recent years. The US has also hosted its own summits for African leaders, the last taking place in Washington in late 2022. Companies from the US and Africa agreed on about $15 billion in deals at the time, including investments in cybersecurity and clean-tech energy, as well as promises to expand trade.

US officials say their deals — such as financing support for the $2.3 billion Lobito corridor rail project linking Congo, Zambia and Angola — won’t leave African nations mired in debt. But even American officials concede that when it comes to large-scale investments, African leaders see few alternatives to Beijing.

“Wherever I go, heads of state tell me, ‘I’m not choosing the path with the Chinese and increased debt,’” said Amos Hochstein, a senior White House adviser on energy and investment. “‘But if I have to make a choice between that investment or no investment, I will choose that investment every day,’” he said.

(By Neil Munshi and Peter Martin)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments