What’s Anglo worth? For now it’s less than the sum of its parts

As BHP Group considers its next move, there’s one big question facing the mining world’s bankers, analysts and executives at rival producers: What’s Anglo American Plc actually worth?

Anglo’s shares are trading about 8% above the price implied by BHP’s initial proposal, which was swiftly and firmly rejected, and Bloomberg reported on the weekend that the larger firm was considering an improved offer.

But how high can BHP go? The world’s biggest miner needs to thread the needle with an offer that can win over Anglo investors while maintaining the support of its own shareholders — especially given the company’s history of disastrous dealmaking.

And while BHP’s bid is driven by its interest in Anglo’s huge copper business, the company produces a hodgepodge of other commodities from diamonds to platinum and coal — each with different market dynamics and degrees of attractiveness. BHP wants Anglo to spin off its majority stakes in two South African miners even before a deal takes place, and has suggested it would put other unwanted pieces up for sale as well.

Diversified dilemma

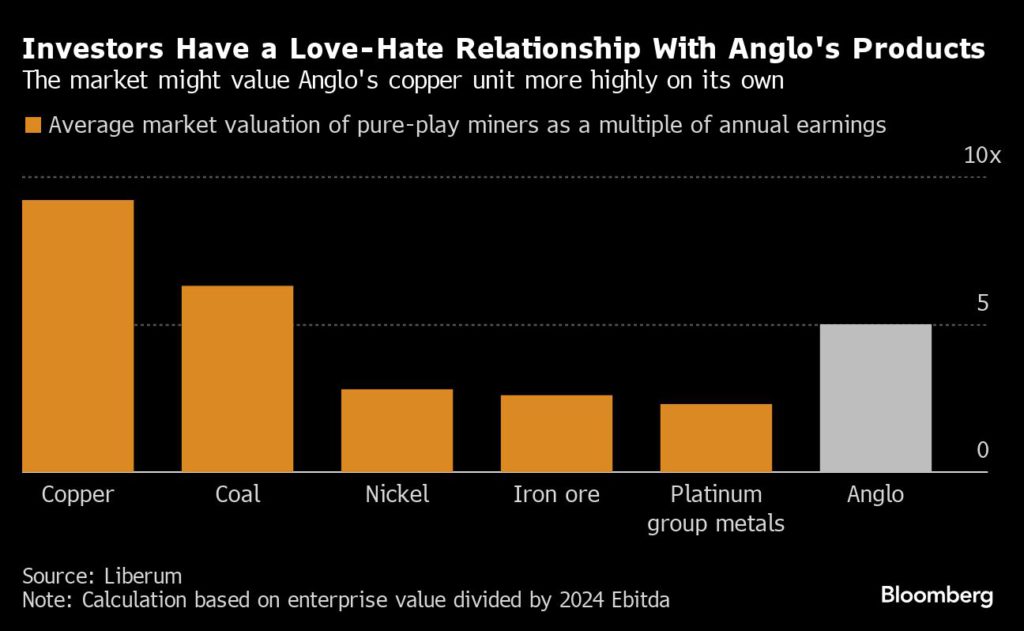

The mining industry can be loosely divided into two types of companies: “pure plays,” which focus on one particular metal such as copper or gold, and “diversified” miners — conglomerates like BHP and Anglo that produce a wide range of often-unrelated commodities.

Pure plays in a certain market tend to trade at similar multiples of their earnings, making them easier to value.

But things get a lot messier when it comes to diversified miners, each with a unique combination of commodities under a single management and corporate structure. The diversification helps makes the companies more resilient to demand shocks in any single market, but also means that investors don’t get the full benefit of price rallies if group earnings are weighed down by weakness in other parts of the business.

In Anglo’s case, its particularly unusual mix of niche commodities — it’s the only large miner with big diamonds and platinum operations, for example — are seen as one of the reasons that the company hasn’t been successfully targeted in the past. The iconic De Beers business in particular could be difficult to value, as its only real competitor is Russia’s sanctioned diamond miner.

Even in the absence of a blowout offer from BHP or another rival, Anglo is under pressure to convince shareholders that it can realize more of the latent potential in its portfolio.

Bloomberg reported last week that activist hedge fund Elliott Investment Management has emerged as a top-ten shareholder, and Anglo was already reviewing its businesses even before the BHP bid, in an effort to turn a corner after a series of disappointments that sent its shares plunging.

There are growing expectations that even if Anglo rejects its suitors’ advances, the company could end up being broken down to realize the value of the sum of its parts.

All about copper

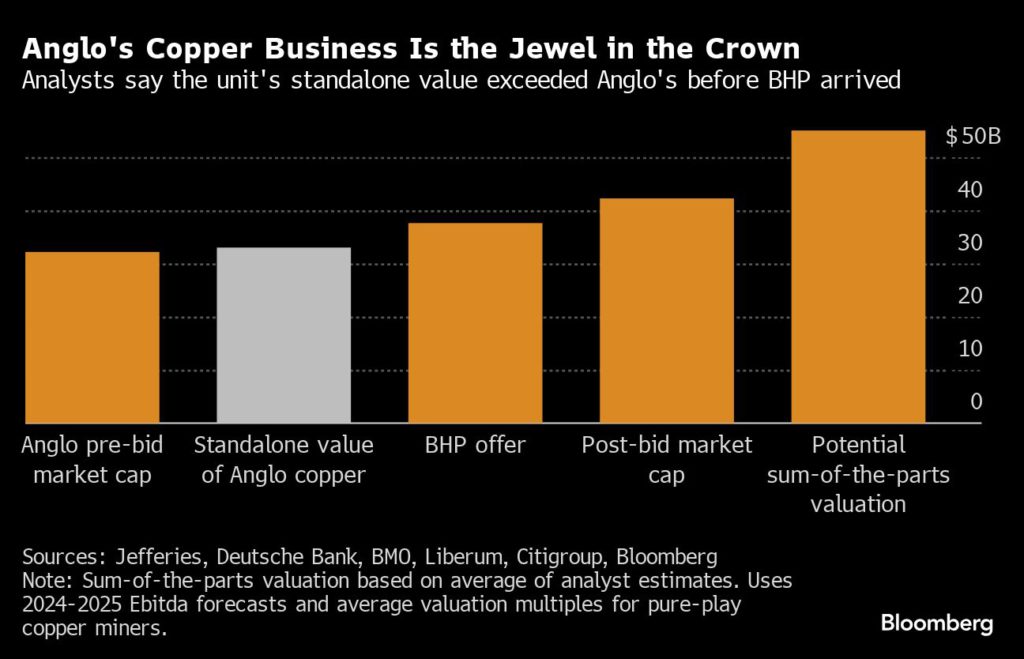

There’s no doubt that Anglo’s South American copper business is the crown jewel. In fact, analyst estimates suggest that the copper business — if it were split out into a standalone, pure-play company — would probably have a higher valuation than Anglo’s entire market capitalization just before Bloomberg broke the news of BHP’s approach.

The question is what other suitors will be willing to pay for the rest of Anglo’s businesses.

The listed South African iron ore and platinum businesses, which BHP wants Anglo to spin off, trade at much lower multiples to earnings than Anglo’s high-flying copper business probably would on its own.

Still, Anglo has some of the world’s best coking coal assets in Australia, while its Minas Rio iron ore mine in Brazil also holds appeal to BHP. While part of the rationale for the deal is to dilute BHP’s dependence on the steelmaking ingredient, Anglo produces a very high-quality iron ore product which is increasingly in demand and would improve the sort of material BHP could offer its customers.

That could leave BHP with more room to bump up its offer — while other iron ore majors like Rio Tinto could also be interested.

Buy or build

One factor is particularly crucial in determining where the ceiling for incoming bids might be: The difference between the cost of buying Anglo and the typical investment needed to build a copper mine from scratch.

Construction costs have surged in recent years and projects frequently face lengthy delays and stiff local opposition, which helps increase the appeal of buying existing mines instead.

On the other hand, pure-play copper miners tend to trade at relatively high multiples — even before the usual takeover premiums are factored in — and the mining industry has been punished by investors in the past for overpaying in a series of disastrous deals.

That’s partly why Anglo is now being viewed as an attractive target: production missteps across its mining portfolio sent its shares tumbling over the past year while other copper miners have rallied.

It’s over a decade since BHP pursued a deal of this size, but there is one recent purchase that might be instructive: the company last year acquired Australian copper miner Oz Minerals for $6.4 billion.

Even if BHP is only interested in Anglo’s copper, its initial bid is still about 13% lower than the price-per-ton of copper it paid for Oz’s mines, according to Bloomberg calculations.

Analysts and traders surveyed by Bloomberg suggested BHP would need to offer between £28 and £35 per share, with the average estimate coming in at £30.43 — about 15% higher than where Anglo’s shares were trading Thursday.

And after Anglo rejected BHP’s multi-step deal structure, there’s also the potential that a rival might be better positioned to make a higher, simpler offer.

“From what we have seen so far the proposal does not reflect the value of the assets or the growth pipeline,” John Teahan, portfolio manager of the Redwheel Climate Engagement Strategies, said in an emailed statement. “It appears a rather opportunistic bid due to the recent weakness in the Anglo American share price, but the move may spur further interest.”

(By Mark Burton)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments