Traders stuck in LME queue vent fury at warehouse’s fee hike

The London Metal Exchange is looking into a sharp administrative fee hike at warehouse operator Istim Metals, after receiving complaints from traders who say the increased cost is putting them under pressure and fueling distortions in the aluminum market.

Istim is one of the main operators in the LME’s warehousing network, which plays a crucial role in the plumbing of global metals markets by allowing traders to make or take delivery of metal when their futures contracts expire.

The company’s warehouses at Port Klang in Malaysia have become the focal point for the aluminum market, holding more than three quarters of LME stocks. However, traders seeking to withdraw metal this year have been stuck in months-long queues after a trading play in May when Trafigura Group delivered huge amounts of aluminum into the warehouses, only to see it quickly ordered back out by a number of banks and hedge funds.

The LME has received several complaints after Istim raised the cost of re-delivering cargoes into its warehouses to $50 a ton, according to people familiar with the matter who asked not to be identified discussing private information.

Warehousing companies typically charge between $5 and $10 a ton, and traders have told the LME that the move is driving up the price of some aluminum contracts and raising costs for traders looking to exit money-losing futures positions, the people said.

The uproar over the Istim fee hike is the latest twist in a long-running history of stockpile battles among traders and warehouse companies in the LME’s aluminum market. Warehouses charge storage fees from owners of the metal, and often enter into “rent sharing” deals with traders delivering large volumes.

Queues to take delivery from Istim warehouses in Port Klang have soared this year since the Trafigura deliveries — by the end of July the wait time had stretched out to 280 days.

The fee that Istim has raised applies to cases where traders have ordered metal out of the LME network, but then decide to re-register — or “re-warrant” — it back into the system.

Traders who hold inventories typically sell offsetting positions in futures markets to hedge against price fluctuations while the metal is in storage or transit. But the lengthy delays mean that some traders are looking to buy those futures contracts back and extend their hedges to later months while they wait for the metal to emerge.

In normal market conditions, it costs little or nothing to roll the positions because the expiring contracts that traders are buying back tend to be cheaper than the later-dated ones they’re selling.

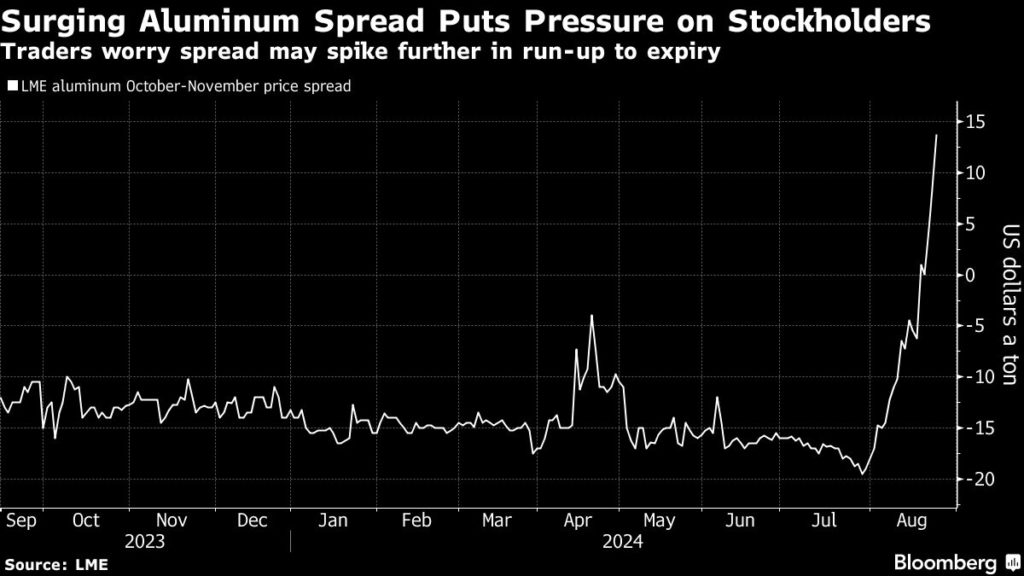

But LME aluminum contracts expiring in October have started trading at premiums to those maturing a month later, and so traders looking to roll their contracts over that period would be doing so at a loss. The October-November spread jumped to a $14.50 premium on Friday, up from a $19 discount in late July.

In such a scenario, traders would typically just re-register their metal to close out the hedges, rather than rolling them forward at a loss.

But some have complained to the LME that the Istim fee hike means they’d face even greater costs re-warranting the metal, and as such they risk becoming stranded with loss-making futures positions. In private conversations, the LME has told traders that it is looking into the issue, people familiar with the matter said.

A representative for Istim Metals declined to comment.

A spokeswoman for the LME declined to comment on the complaints or the status of any investigation into Istim, but pointed to rules which state that warehousing companies cannot impose “unreasonable” fees that have a manipulative, distortive or disorderly effect on the market. The relevant rules state that warehouses will be reported to the UK’s financial regulator if the LME finds indications of market abuse.

“Clause 9.3.1 (ii) of the LME’s warehouse agreement specifically prohibits warehouses imposing unreasonable charges for depositing metal,” the spokeswoman said in an emailed statement. “The LME would investigate any concerns of this nature which are brought to its attention.”

While other aluminum price spreads are still trading at discounts, there’s growing nervousness that the October-November spread could spike further as it approaches expiry. LME data shows that one party has bought at least 30% of the outstanding October aluminum contracts — a long position that’s valued at least $1.8 billion dollars — and traders worry they may need to offer increasingly steep premiums to incentivize the company to sell those positions back.

(By Mark Burton, Archie Hunter and Alfred Cang)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments