The ECB awakens. Will gold feel the force?

Lagarde opened the door to an interest rate hike, which gave the European Central Bank a hawkish demeanor. Does it also imply more bullish gold?

The ECB has awoken from its ultra-dovish lethargy. In December 2021, the central bank of the Eurozone announced that its Pandemic Emergency Purchase Program would end in March 2022. Although this won’t also mean the end of quantitative easing as the ECB continues to buy assets under the APP program, the central bank will be scaling down the pace of purchases this year. Christine Lagarde, the ECB’s President, admitted it during her press conference held last week. She said: “We will stop the Pandemic Emergency Programme net asset purchases in March and then we will look at the net asset purchases under the APP.”

She also left the door open for the interest rates to be raised. Of course, Lagarde did not directly signal the rate hikes. Instead, she pointed out the upside risk of inflation and acknowledged that the macroeconomic conditions have changed:

We are going to use all instruments, all optionalities in order to respond to the situation – but the situation has indeed changed. You will have noticed that in the monetary policy statement that I just read, we do refer to the upside risk to inflation in our projection. So the situation having changed, we need to continue to monitor it very carefully. We need to assess the situation on the basis of the data, and then we will have to take a judgement.

What’s more, Lagarde didn’t repeat her December phrase that raising interest rates in 2022 is “very unlikely”. When asked about that, she replied:

As I said, I don’t make pledges without conditionalities and I did make those statements at our last press conference on the basis of the assessment, on the basis of the data that we had. It was, as all pledges of that nature, conditional. So what I am saying here now is that come March, when we have additional data, when we’ve been able to integrate in our analytical work the numbers that we have received in the last few days, we will be in a position to make a thorough assessment again on the basis of data. I cannot prejudge what that will be, but we are only a few weeks away from the closing time at which we provide the analytical work, prepare the projections for the Governing Council, and then come with some recommendations and make our decisions.

It sounds very innocent, but it’s worth remembering that Lagarde is probably the most dovish central banker in the world (let’s exclude Turkish central bankers who cut interest rates amid high inflation, but they are under political pressure from Erdogan). After all, global monetary policy is tightening. For example, last week, the Bank of England hiked its main policy rate by 25 basis points and started quantitative tightening. Even the Fed will probably end quantitative easing and start raising the federal funds rate in March. In such a company, the ECB seems to be a reckless laggard. Hence, even very shy comments mean something in the case of this central bank. The markets were so impressed that they started to price in 50 basis points of rate hikes this year, probably in an exaggerated reaction.

Implications for gold

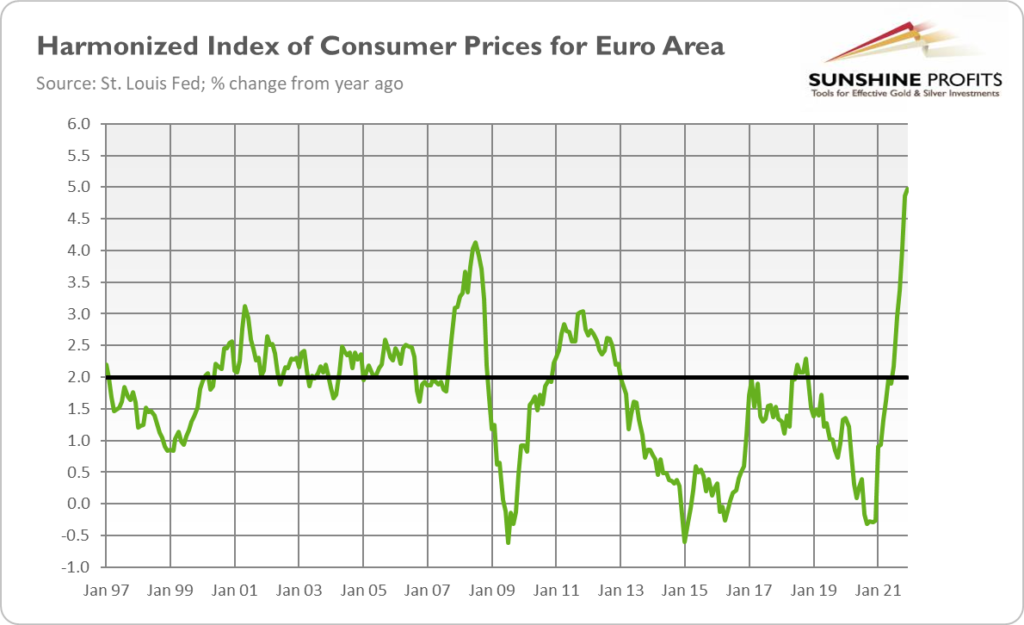

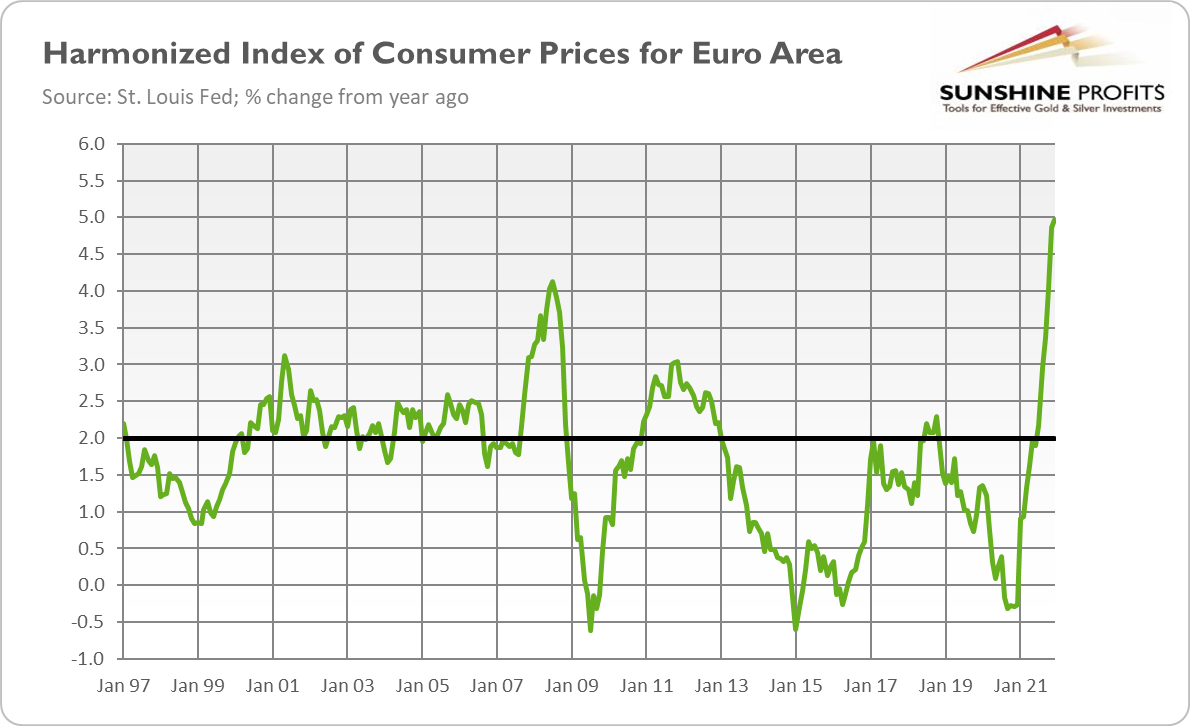

What does the latest ECB monetary policy meeting mean for the gold market? Well, maybe it wasn’t an outright revolution, but the ECB is slowly reducing its massive monetary stimulus. Although the euro area does not face the inflationary pressure of the same kind as the US, with inflation that soared to 5% in December and to 5.1% in January (according to the initial estimate), the ECB simply has no choice. As the chart below shows, inflation in the Eurozone is the highest in the whole history of euro.

Additionally, in the last quarter of 2021, the GDP of the euro area finally reached its pre-pandemic level, two quarters later than in the case of the US. Europe is back in the game. The economic recovery strengthens the hawkish camp within the ECB. All of this is fundamentally bullish for gold prices.

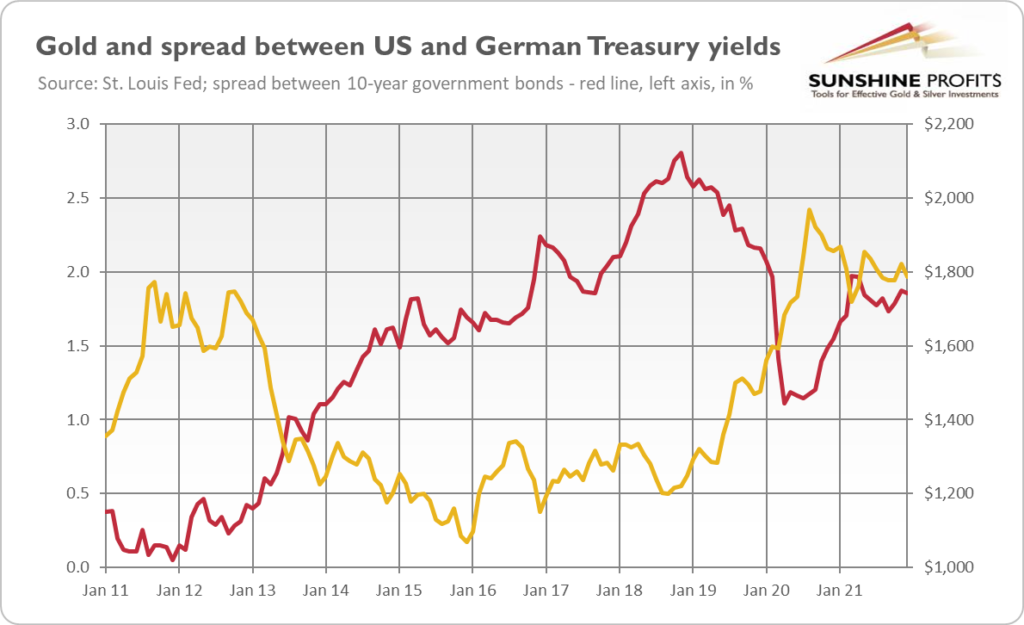

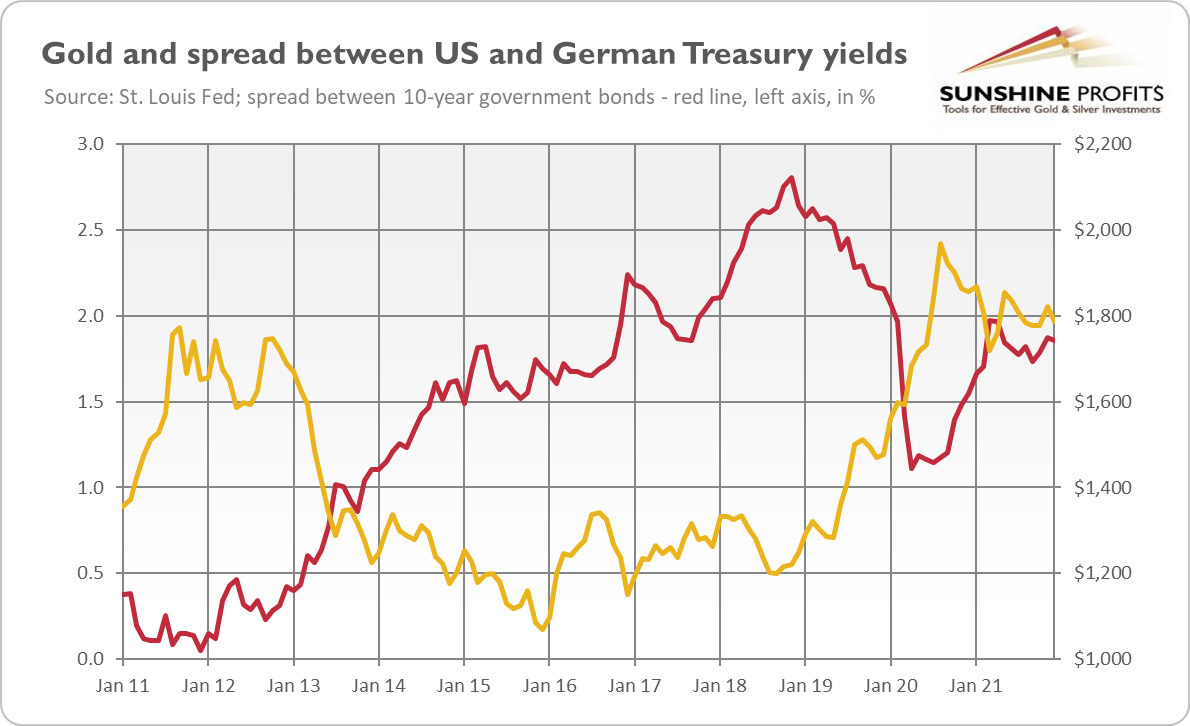

To be clear, don’t expect that Christine Lagarde will turn into Paul Volcker and hike interest rates in a rush. Given the structural problems of the euro area, the ECB will lag behind the Fed and remain relatively more dovish. However, German bond yields have recently risen, and there is still room for further increases. If the market interest rates go up more in Europe than across the pond, which is likely given the financial tightening that has already occurred in the US, the spread between American and German interest rates could narrow further (see the chart below).

The narrowing divergence between monetary policies and interest rates in the US and in the Eurozone should strengthen the euro against the greenback – and it should be supportive of gold. As the chart above shows, when the spread was widening in 2012-2018, gold was in the bear market. The yellow metal started its rally at the end of 2018, just around the peak of the spread.

On the other hand, if the divergence intensifies, gold will suffer. Given that Powell is expected to hike rates as soon as March, while Lagarde may only start thinking about the tightening cycle, we may have to wait a while for the spread to peak. One thing is certain: it can get hot in March!

(By Arkadiusz Sieron)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

{kind=link}

{kind=link}

Comments