Tesla trounced by obscure EV suppliers with 200% returns

Producers of battery metals and specialist chemicals for electric cars are outpacing sector leaders like Tesla Inc. in the stock market as prices of key commodities climb due to tight supply and wider adoption of zero-emission vehicles.

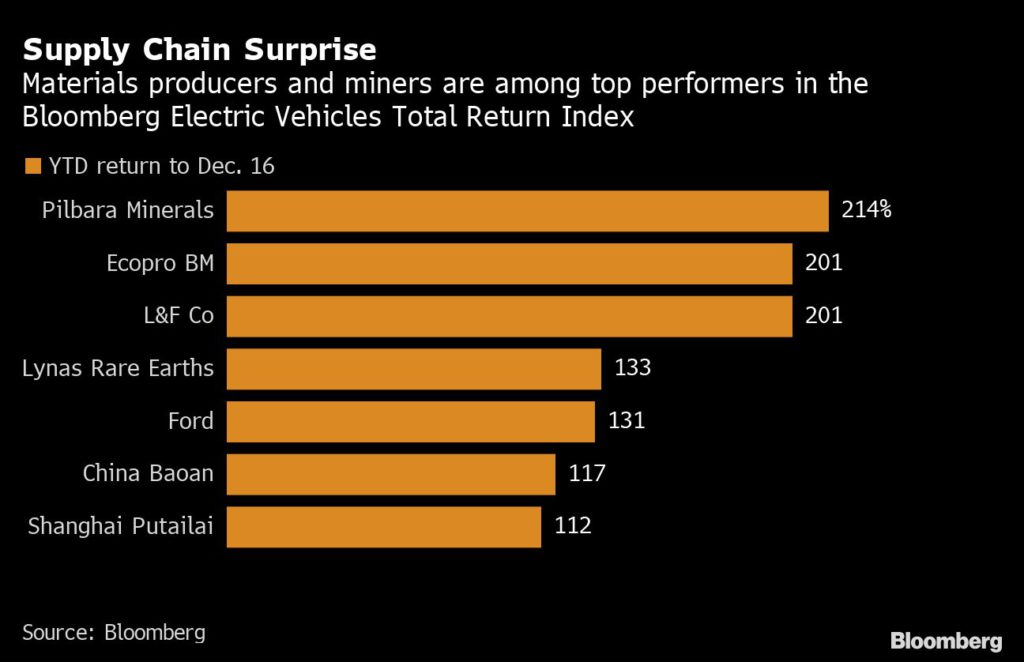

Pilbara Minerals Ltd., a Perth-based supplier of lithium raw materials, jumped more than 210% this year to Thursday’s close, while Ecopro BM Co. and L&F Co., both South Korea-based producers of cathode active materials, have risen more than 200%. The companies lead advances on the Bloomberg Electric Vehicles Total Return Index, which tracks 69 businesses including automakers and technology developers worth more than a combined $2 trillion.

“It’s proven to be the case that the raw materials are scarce, and pretty quickly the margin has been pushed upstream,” said Pilbara’s Chief Executive Officer Ken Brinsden. The mining company, which has supply deals with firms including battery giant Contemporary Amperex Technology Co. Ltd., slashed output in mid-2019 as prices cratered, and has since rebounded on lithium’s revival, expanding operations and acquiring a rival producer’s project.

Battery production capacity is being added faster than supply chains can grow, leading to severe deficits of some components, and shortages of materials like copper foil. With demand so strong, miners and chemicals producers have been able to hike prices and swell profits.

“Investors are are paying more attention to components and metals suppliers as they look for hidden gems along the battery supply chain,” said Horace Chan, a Hong Kong-based chemicals analyst at Bloomberg Intelligence.

L&F, which supplies battery makers including LG Energy Solution and SK On Co., expects earnings to rise in 2022 and plans to increase annual production capacity from its plants in South Korea to as much as 200,000 tons in 2025 from 40,000 tons this year, CEO Patrick Choi said in an interview. The company will also seek to increase production overseas.

Cathodes, typically the most expensive part of a lithium-ion cell, are one of four major components in every battery, alongside the anode material, electrolyte and separator. Analysts forecast L&F’s sales to triple to 1 trillion won ($850 million) this year. For 2022, sales will be at least 2 trillion won, Choi said.

Lynas Rare Earths Ltd., an Australian-listed producer of rare earths with a plant in Malaysia, is another top performer on the Bloomberg index, rising about 132%. Tesla has advanced about 32% this year.

Battery factories can be proposed and constructed within about 18 months, whereas mines can typically take 7 years or longer to bring online, indicating that supply of raw materials is likely to remain constrained and prices will stay high, Pilbara’s Brinsden said.

“There is likely to be more pain and heartache. The supply can’t respond as quickly as people assume and that’s happening at the same time as demand is ballooning,” he said. “There’s no such thing as a quick fix for the industry.”

High metals prices can be problematic for companies like L&F too, and that’s spurring efforts on battery recycling to recover raw materials from spent packs, according to Choi.

L&F set up a partnership in October with Redwood Materials Inc., the battery recycler created by Tesla co-founder J.B. Straubel, to collaborate in Europe and the U.S. “Now everyone is talking about shortage of metals used for batteries,” Choi said. “But if recycling is realized, let’s say about 80% of cathode in used cells can be extracted and re-used for new EVs a decade later.” That would ease supply burdens and lower costs to as little as 60% of current levels.

While battery makers have plans to continue major expansions, there are risks for L&F in keeping pace with that growth and potentially saturating the market, as rival suppliers also build capacity, according to Choi.

L&F will consider “which one we should prioritize between profitability and growth,” he said. “Our near-term goal is to increase alliances with potential partners in the U.S. and Europe first and boost our presence in the industry.”

(By Heejin Kim and David Stringer, with assistance from Annie Lee)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments