Stubbornly resilient lithium supply remains hurdle to recovery

A persistent lithium glut and the prospect that some mines could be restarted if prices rise means the battery metal is unlikely to mount a significant recovery this year.

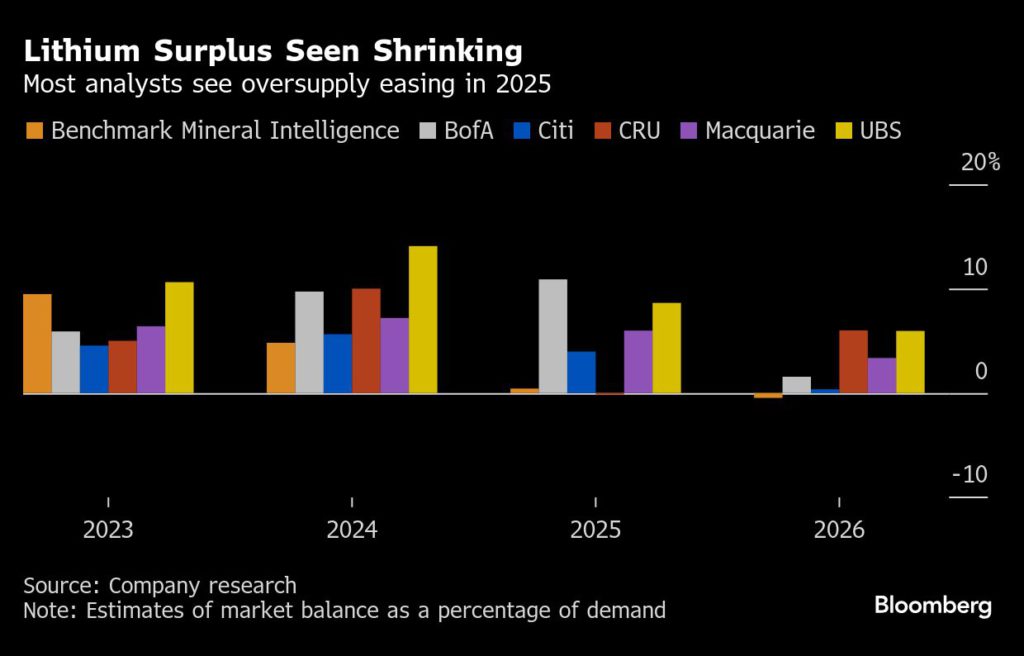

Lithium prices have plunged since late 2022 on oversupply and slower-than-expected growth in electric vehicle demand. The rout has resulted in some mining capacity being suspended, but most analysts still see a surplus this year, although they forecast it will be smaller than in 2024.

Underlying the reluctance to reduce supply — or the readiness to bring it back too soon — is the fact that demand is expected to rise rapidly over the longer term as the energy transition gathers pace. Geopolitical tensions — including the prospect of hefty tariffs — may also be encouraging miners to keep digging on fears the market could split into rival trade blocs.

“This swing supply dynamic could serve as a cap on price increases in 2025, as rapid restarts may lead to a more oversupplied market than currently forecast,” said Federico Gay, principal lithium analyst at industry consultancy Benchmark Mineral Intelligence.

Benchmark Mineral sees North Asian lithium carbonate prices at $10,400 a ton this year, the same as at the end of 2024, according to Fastmarkets pricing. The average of four analyst estimates for next year came in at $10,685.

| Lithium carbonate – North Asia | 2025 forecast |

|---|---|

| Benchmark Mineral Intelligence | $10,400 |

| Macquarie | $10,775 |

| S&P Global | $10,566 |

| UBS | $11,000 |

Some lithium producers struggling with shrinking margins suspended output or delayed expansions last year. That helped prices to stabilize from the middle of August, but it wasn’t enough to spur a meaningful rebound. There are now concerns that price rises could see mining quickly ramped up again, with Africa and China seen as the most likely places where this may happen.

“Operations that are producing at a reduced utilization rate could, however, restart in as little as a month,” said Thomas Matthews, analyst at CRU Group, citing the Greenbushes, Wodgina and Pilgangoora projects in Australia. “The market balance will be dependent on whether we see these operations ramping up, or whether more supply will be curtailed.”

There’s also new supply set to come onstream this year. Benchmark Mineral sees Zimbabwe, China and Argentina among countries where output will rise from last year, while CRU Group says capacity in Mali and Brazil is set to grow rapidly from a low base.

“New supply keeps hitting the market, at the same time as higher-cost, marginal operators are not shuttering operations in sufficient volumes,” Bank of America said in a note in November. “This is partially driven by strategy or geopolitics: producers do not want to curtail activity in a market that is growing exponentially.”

On the demand side, a shakier sales growth outlook for EVs, particularly in the US given President-elect Donald Trump’s enthusiasm for fossil fuels, also looks set to drag on lithium prices. BloombergNEF downgraded its forecast for EVs to make up 48% of new passenger car sales in the US by the end of the decade to just a third following the Republican clean sweep in November’s election.

“Global automakers and policymakers stand at a crossroads, debating whether to continue with electrification and embrace the new EV-era — packed by mostly China headquartered manufacturers with a huge head start — or to pace the transition,” Alice Yu, senior analyst at S&P Global Commodity Insights, said in a note last month.

The prospect of a trade war between the US and China could also lead to heightened volatility for lithium prices, with Beijing saying last week that it may add various technologies — some used for lithium refining and battery chemicals production — to its list of items that are subject to export controls.

“There are naturally some uncertainties,” CRU’s Matthews said. “Tariffs and export controls have been widely publicized. Repealing subsidies and relaxing emissions standards could also spell bad news for the market.”

(By Annie Lee)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments