Steel industry emissions to decline 30% by 2050 — report

Steel industry’s carbon emissions are expected to fall 30% by 2050 compared to 2021 levels, according to a new report by Wood Mackenzie.

Steel is a challenging sector to decarbonise. However, evolving green steel goals are altering the supply landscape and steelmakers are under pressure from stakeholders to reduce their reliance on conventional (highly polluting) blast furnace route and adopt low-emission alternatives.

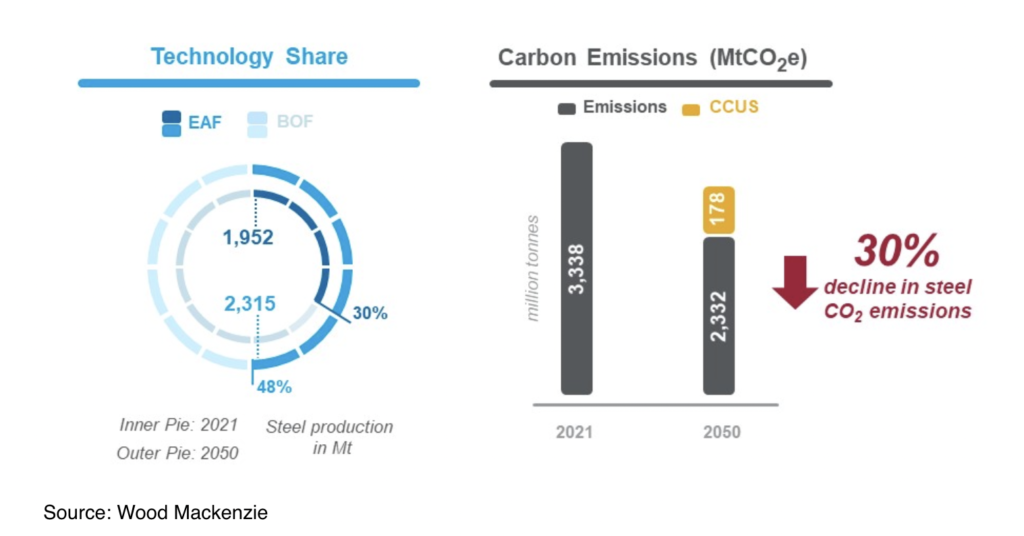

“The global share of electric arc furnace (EAF) in steelmaking is rising with policy shifts and increasing focus on scrap use. Basic oxygen furnace (BOF) output will decline 0.5% annually until 2050, whereas EAF output could increase 2.3% yearly in the same period. By 2050, EAF will account for 48% of the technology share used in steelmaking, up from 30% last year, making it almost on par with the traditional BOF method,” Wood Mackenzie research director Malan Wu said.

“Together with green hydrogen-based direct reduced iron (DRI), scrap use and adoption of carbon capture, utilisation and storage (CCUS), steel industry’s carbon emissions can decline 30% from current levels by mid-century.”

The scrap-EAF route is the least polluting among available technologies. This makes scrap a sought-after metallic by steelmakers. Scrap blending will potentially increase in the blast furnace route with quality enhancements and converter retrofits. DRI will also receive a boost, primarily due to commercial adoption of the hydrogen-based route.

The steel industry is expected to commence hydrogen use as early as 2027, with EU taking the lead. Hydrogen-based steel production will eventually account for 10% of the total steel output or 232 million tonnes (Mt) by 2050. Wood Mackenzie projects that 40% of DRI produced by mid-century will be hydrogen-based.

Carbon offset measures such as CCUS will lend further support. Wood Mackenzie believes that the steel industry will be able to capture, store and potentially utilise around 178Mt of the residual emissions. This will make up 5% emission savings of the 30% carbon emissions decline by 2050.

“Blast furnace gas emissions are complex, and it is challenging to separate carbon from them,” Wu said. We assume that technological advancement and bulk efficiencies will allow a maximum capture rate of about 20-25% in advanced economies such as the US and EU.”

“Capture rates can be improved by increasing the reliance on smelting reduction technologies such as HIsarna and Corex, that produce top-gas with much higher carbon concentrations. This will make it easier to separate carbon from other impurities. However, these technologies have yet to prove their commercial viability, even after being deployed in Asia and Europe.”

China is expected to take the lead in reducing absolute emissions. Wood Mackenzie estimates Chinese emissions to halve between 2021 and 2050, and a major proportion of emissions reduction will come from the projected fall in steel output.

Mature economies such as Japan, Korea, Taiwan, EU, UK and US will need to do more to curb emissions as developing nations will be slow adopters and small contributors to emissions cuts. These economies will abate emissions by nearly 50% from current levels while maintaining or increasing their steel output.

India and Southeast Asia will in turn worsen their emission profile as their crude steel production rises through the BF-BOF route. The aggregate emission intensity in these regions will improve as production triples and carbon emissions will in turn double from current levels. Decarbonisation initiatives in these regions will intensify in the second half of the forecast horizon.

“The onus will be on mature economies to decarbonise quickly. These economies will look to pare down emissions by switching to EAF, which is three-quarters less emission-intensive than the blast furnace route,” Wu said.

India and Southeast Asia, the key demand drivers, will buck this trend as most capacity additions are via the BF-BOF route. However, nearly two-thirds of incremental supply between 2021 and 2050 will materialise from India and Southeast Asia – cushioning the negative impact on hot metal.”

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments