Short squeeze fears grip tin as LME says it’s watching market

Supply ruptures from Southeast Asia to Africa. The rise of artificial intelligence. A “big bull” with a dominant position. This potent cocktail has put an often-overlooked metal, tin, at risk of a short squeeze after a price spike this month.

Tin on the London Metal Exchange has surged in April, and its 25% advance in 2024 puts it well ahead of more closely-watched commodities like copper or crude oil.

A swathe of different factors lies behind the metal’s rapid ascent. Disruptions have hit tin supply in major producers Indonesia, Mynamar and Democratic Republic of Congo, while analysts say demand from electronics will expand as the world’s AI boom demands more computing power.

But market chatter in recent weeks has focused on the role of a single, bullish trader that’s tightening its grip on LME tin. That entity is holding at least 40% of long positions on tin for May delivery, according to regular exchange data that doesn’t identify holders.

That level of concentration hasn’t been seen since 2017, and equates to at least 90% of the volume now held in LME warehouses. Holders of short positions could find themselves in a tight spot as the May contract approaches expiry.

Necessary controls

“Some market participants feel there could be a risk of a squeeze,” said Ding Wenqiang, senior analyst at one of China’s largest metal researchers, Mysteel.com. “They are paying close attention to the movements of the big bull in the May contract.”

Commodities markets, especially less liquid ones like tin, are prone to periodic short squeezes where prices surge as shorts are forced to cash out of loss-making bets. The 2022 drama that gripped the nickel world was a prominent example.

The LME acknowledged tightness in the tin market and said in an email that it’s monitoring the market closely. “The LME has the necessary controls in place to ensure continued market orderliness,” it said, citing limits on nearby spreads, delivery deferral procedures and mechanisms to control volatility.

Driving forces

Indonesia, the biggest global tin exporter, has reduced shipments amid licensing delays and a high-profile corruption probe that has ensnared many tin smelter executives and traders. Flows from war-torn Myanmar, the world’s No.3 producer, have slowed, while there have also been disruptions in the Democratic Republic of Congo due to armed unrest.

On the demand side, the growth of the global AI sector is a potential boon for metals used in electronics and electrification. Huge numbers of new data servers and computing systems will be needed, boosting tin consumption because it’s used in soldering.

“Every data byte and every electron travels through hundreds of solder joints that connect it all together,” Jeremy Pearce, head of market intelligence and communications at the International Tin Association, said by email. While it’s challenging to give demand estimates at this stage, he said, the basic view is that much more tin will be needed in computing and communication systems.

LME tin inventories fell 47% so far this year to 4,045 tons, and the metal’s spot price recently flipped to a premium against the three-month futures contract — a structure known as backwardation that indicates a tight market.

The benchmark tin contract climbed to the highest since June 2022 on Friday, while open interest reached the most since 2015. Prices were little changed on Wednesday at $31,810 a ton.

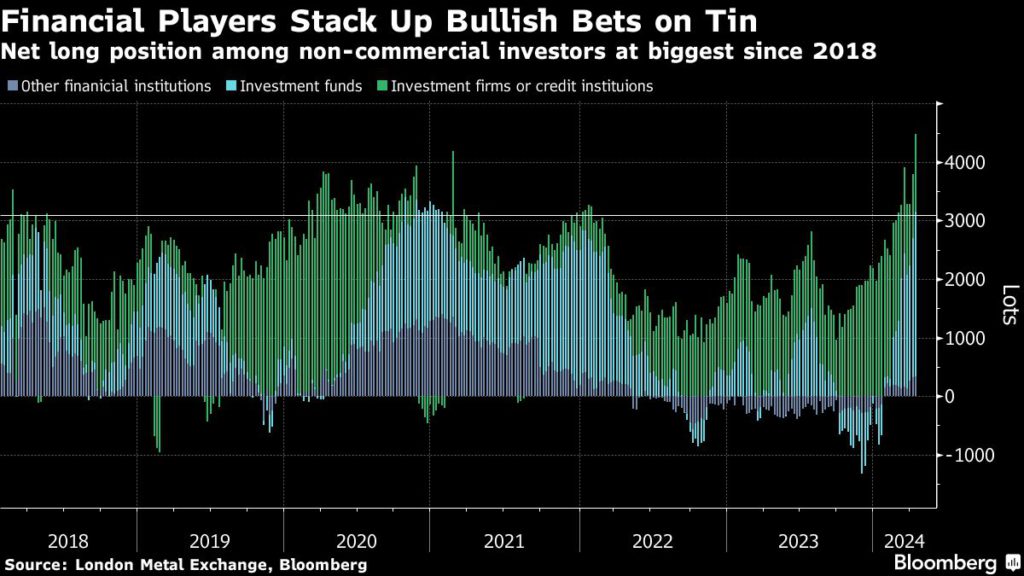

There are clear signs that speculative bets have been building, with hedge funds, assets management firms and other financial institutions entering the market.

The aggregate net-long position held by these financial investors rose to the highest level since the LME started publishing such data in 2018. And the combined long position held by these traders, who rarely participate in physical tin trading, now accounts for 69% of all bullish bets, according to the exchange’s latest summary of trader commitments.

China factor

In previous bouts of tightness in the tin market, exports from China have helped to plug a supply gap and rebalance the market. But, while inventories in China have been rising and prices are relatively weaker, the discount to the world market isn’t yet big enough to spur exports, Mysteel’s Ding said.

Finally, the LME’s recent removal of two Chinese tin smelters from its list of “good for delivery” brands has deepened market concerns about a squeeze on supply. The LME had said in January that it planned to delist 10% of brands due to non-compliance with the exchange’s responsible-sourcing rules.

“The LME’s decision to cancel the delivery qualifications of two Chinese brands earlier this month also weakened expectations for Chinese supply to ease tensions in the market,” Ding added.

(By Alfred Cang)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments