Russell: Commodity outperformance switching to energy from metals

(The views and opinions expressed herein are the views and opinions of the author, Clyde Russell, a columnist for Reuters.)

The rally in commodity prices is likely to see a shift from metals to energy resources, such as crude oil, liquefied natural gas (LNG) and coal, according to the latest forecasts from the Australian government.

While the June quarter report from the Department of Industry, Science, Energy and Resources doesn’t foresee a major retreat in the prices of metals such as copper, iron ore, zinc, aluminum and nickel, it does forecast stronger performances from energy commodities.

The headline number from the report is that Australia’s commodity exports are expected to reach a record A$310 billion ($235.3 billion) in the 2020-21 fiscal year that ends on June 30.

This is up some 6% from the previous record in 2019-20, and the outlook remains positive with the government forecasting a further 7.7% gain to A$334 billion in 2021-22.

Australia is the world’s largest exporter of iron ore, LNG and coking coal used to make steel.

It ranks second behind Indonesia for thermal coal and third in shipments of copper ore, and is a major producer of both aluminum and alumina, the raw material used to make the refined metal.

Overall, the outlook is for steady to lower prices for metals, with battery metals lithium and nickel being exceptions

Australia is also the world’s third-largest gold producer and the biggest net exporter of the precious metal, and is a top supplier of battery metals such as nickel and lithium.

Iron ore is the heavy hitter of Australia’s resource exports, with the country responsible for 53% of the world’s exports, or more than double that of number two Brazil’s 21% share.

It has also been a stellar performer in the 2020-21 year as robust Chinese demand collided with supply issues as the coronavirus pandemic affected shipments from Brazil and number three exporter South Africa, and Australia experienced some weather disruptions.

This sent the spot price from a 2020 low of $79.60 a tonne to a record high of $235.55 on May 12, with the steel-making ingredient largely holding on to its gains, ending at $217.75 on June 25.

The Australian government forecasters tend to be cautious in their price assumptions and they expect iron ore to average $137 a tonne in 2020-21, before retreating to $129 in 2021-22 and $100 in 2022-23.

Australia’s iron ore exports are expected to be around 871 million tonnes in 2020-21, before rising to 904 million in 2021-22 and 954 million in 2022-23.

This extra supply will drive prices lower, especially as China, the world’s biggest buyer of iron ore, is forecast to keep imports largely steady over the coming years.

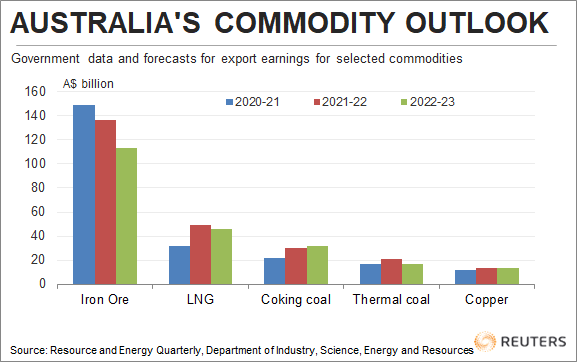

Overall, the report forecasts the value of iron ore exports to decline from A$149 billion in 2020-21 to A$137 billion in 2021-22 and A$113 billion in 2022-23.

For copper, the forecast is that the industrial metal has already had its run, and the next couple of years will see consolidation, with the price retreating from its recent record above $10,000 a tonne to an average $8,579 in 2021-22 and $7,994 in the following fiscal year.

Australia’s export earnings from copper are forecast to be largely steady at A$13 billion in both 2021-22 and 2022-23.

It’s a similar story for other metals with prices and earnings expected to be fairly stable to gently higher for aluminium and alumina, nickel and zinc.

Lithium export revenue is forecast to surge to A$2.5 billion in 2022-23 from A$900 million in 2020-21, but this because of a 53% jump in output.

Bullish energy

In contrast to the steady picture for metals, the outlook for energy commodities seems brighter, with LNG a standout as export earnings are forecast to rise from A$32 billion in 2020-21 to A$49 billion in 2021-22 and stay at A$46 billion in 2022-23.

This is because prices are forecast to rise from A$7.80 a gigajoule, equivalent to $5.61 per million British thermal units (mmBtu), to A$11.2 a gigajoule in 2021-22, or about $8.06 per mmBtu.

Australia isn’t a major producer or exporter of crude oil, but even its modest exports are forecast to rise to A$10.9 billion in 2021-22 from A$7.7 billion in 2020-21.

This would mean that LNG and crude oil combined will earn more than the total for coking and thermal coal, even though both coal grades are forecast to see strong export revenue growth.

Earnings from coking coal, used to make steel, are expected to rise to A$30 billion in 2021-22 from A$22 billion the prior year, while those for thermal coal, used for power generation, are forecast to increase to A$21 billion from A$17 billion.

Given volumes are forecast to be largely steady, the gains are all down to higher prices.

Overall, the outlook is for steady to lower prices for metals, with battery metals lithium and nickel being exceptions, while LNG, crude oil and coal are set to perform strongly.

Another point worth making is that the Australian government’s forecasts don’t exactly scream out that a commodity supercycle is underway, rather they point to a period of cyclical strength for energy and at best consolidation for industrial metals.

(Editing by Muralikumar Anantharaman)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments