Rio Tinto plays chancy round of Mongolian roulette

December 9 is shaping up to be a big day for Jakob Stausholm. Just ahead of his two-year anniversary as Rio Tinto’s chief executive, he will learn the fate of the mining giant’s tortuous efforts to buy out minority investors in Turquoise Hill Resources, the majority owner of a flagship project in Mongolia. Success would give the growth strategy a real boost; failure could mean senior heads roll.

Oyu Tolgoi, a $10 billion copper and gold mine near the Chinese border, is an epic saga dating back more than a decade. When it eventually scales up, it will be the world’s fourth largest excavator of the red metal. It has long been saddled with an unwieldy corporate structure, which involves Mongolia controlling 34% and Canada-listed Turquoise Hill, in which Rio holds a majority stake, owning the rest.

Cleaning up that structure prompted Stausholm to take two expensive steps. With Mongolia’s entire GDP a mere $15 billion, the country’s equity stake was only made possible by over $2 billion of historic loans owed to Turquoise Hill. The costs of repaying that debt and the accrued interest meant Ulaanbaatar stood to wait decades before receiving dividends from its own project. To stem political blowback regarding Rio’s alleged poor performance as the mine’s operator, Stausholm agreed a year ago to write off that debt.

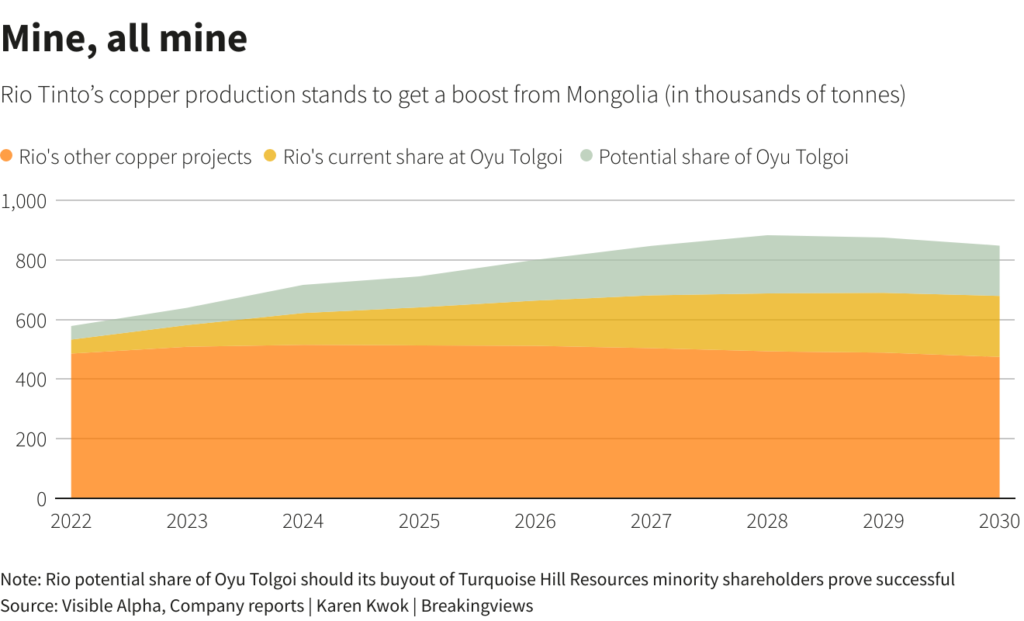

Buying out the Turquoise Hill minority shareholders is Stausholm’s other initiative. Rio’s 51% ownership means it already consolidates $4 billion of the related Oyu Tolgoi debt onto its balance sheet. A successful deal would allow it to keep more of the earnings and increase Rio’s global copper production by 50% to around 900,000 tonnes by 2028. It also would be a way to rid Rio of similar complaints about its operational performance from the minority shareholders.

The process has been a shambles. Before Stausholm’s first offer in March, Turquoise Hill shares had been trading around C$25 ($18.35) apiece, valuing the equity at $3.7 billion. Some owners, including Pentwater Capital Management, which now holds a 15% stake, spurned the initial 36% premium. They also dismissed a sweetened C$40 bid. Even when Rio divulged its final offer of C$43 a share in September, valuing the company at $6.7 billion, Pentwater and another refusenik, SailingStone Capital, demurred. Determining the fair value has multiple answers, but the dissenters have come close to reaching the simple majority of non-Rio shareholders needed to block the deal.

Then things got really silly. In desperation, Stausholm deployed a peculiarity of Canadian securities law allowing Pentwater and SailingStone to have their Turquoise Hill valuations determined by an arbitration process, in return for sitting out the vote. While it wasn’t certain that process would award them much more, other shareholders feared the risk of an exclusive sweetheart deal was too great. Canadian regulators decided to investigate, which delayed the ballot yet again. On Nov. 18, Rio reversed course and scrapped the whole side deal.

Stop digging

Stausholm looks somewhat foolish, but he is not in a hopeless position. Arguably, the minority shareholders will have to accept the C$43. If they don’t, the shares could fall back to C$25. Considering that pure-play mining stocks such as First Quantum Minerals and the copper price itself have both retreated by 15% since March, Turquoise Hill’s stock price might even drop to around C$20.

The Rio boss also has a stick, however. Due to cost overruns and delays, Oyu Tolgoi faces a funding gap exceeding $3.6 billion. Regardless of what happens at the ballot box, Stausholm will need money to get the project back on track. One way to do so is with a rights issue, which gives Stausholm the chance to kill two birds with one stone.

Imagine minority shareholders vote down the offer, but Rio then has Turquoise Hill issue fresh equity. Extending the due date on a chunk of its debt while raising, say, half the funding gap in shares at a 40% discount to Turquoise Hill’s current C$42 price would dilute Pentwater from 15% to 10%, on Breakingviews calculations. The viability of renegotiating the borrowing terms is controversial, however. If Rio had to raise the full $3.6 billion at a shrunken C$20 a share and Pentwater once again declined to participate, its stake would slump to 5%.

Given the buyout mess, Stausholm may regret not opting for a rights issue at the onset. It was always apparent Pentwater might have Rio over a barrel. The battle has damaged Rio’s board. With minimal net debt, the miner had enough cash to buy more Turquoise Hill equity.

Even so, it’s easy to see why Stausholm took a chance. Acquiring the other 49% of Turquoise Hill is the only way to truly simplify Oyu Tolgoi. If the roster of pesky investors simply sold their rights, Rio might have wound up with even more difficult partners, while still having to deal with an independent board.

Those factors may save the Rio CEO if he loses the takeover vote, but a failed buyout could still put pressure on Bold Baatar, the head of copper. He played a key role in negotiating the recent deal with the Mongolian government. At the same time, in a potential sign of where the blame might fall, only Baatar was included in the company’s Nov. 18 press release ending the ill-fated side deal with investors, whereas Stausholm appeared alongside Baatar in the September offer announcement.

The wider lesson is not that developing-world mining projects are fraught with difficulty; they are what big miners like Rio do. Rather, the episode illustrates the need for a leader with the wits and the gall for roulette. Rio shareholders soon will see just how well Stausholm plays.

Context news

Turquoise Hill Resources shareholders are scheduled to vote on Dec. 9 on whether to accept Rio Tinto’s offer to buy the 49% of the company it doesn’t already own.

Rio needs to secure two-thirds support from voting Turquoise Hill shareholders, including its own 51% stake, and a simple majority of the rest of the voting shareholders.

The bid stands at C$43 ($31.64) a share, or just over $3 billion, after Rio twice sweetened it. Pentwater Capital Management and SailingStone Capital Partners, which own respective 15.2% and 2.2% stakes in Canada-based Turquoise Hill, have resisted the offers.

Rio operates the Oyu Tolgoi copper and gold mine in Mongolia.

(By George Hay and Karen Kwok; Editing by Jeffrey Goldfarb and Streisand Neto)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments