Palladium surges above $2,400. Is it sustainable?

A new day, a new record in palladium! Is there any stopping it from reaching another high? What’s next in store for the white metal?

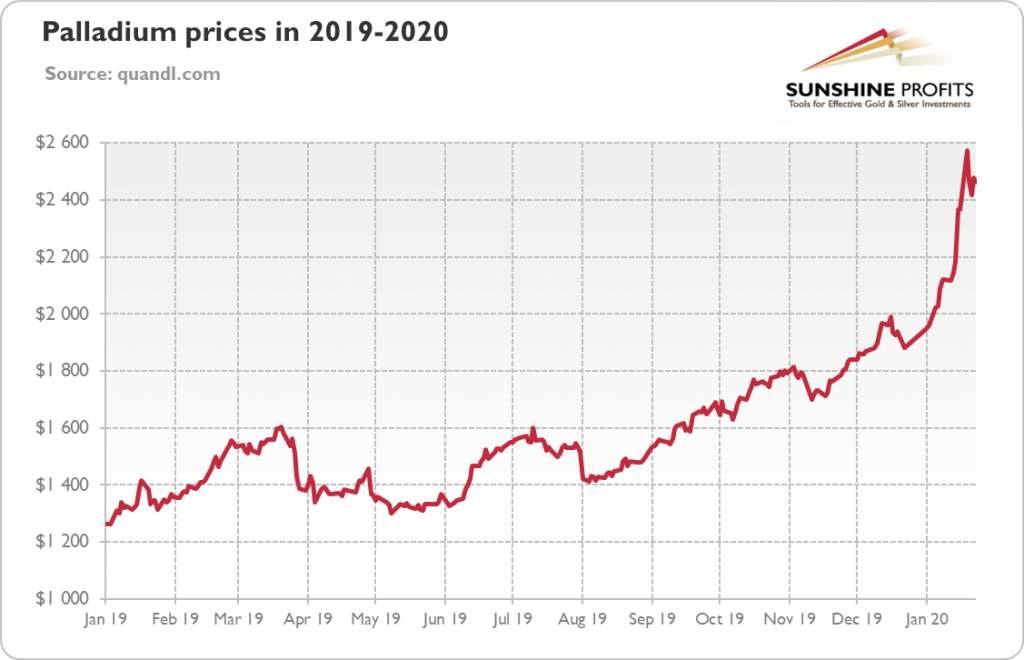

If you thought gold had a good year, you were wrong. OK, maybe not wrong, but palladium enjoyed larger gains. Just look at the chart below, which shows the price of palladium. As you can see on the chart below, this metal gained almost 50 percent in 2019, rising from $1,270 to $1,900!

And if you thought gold started 2020 well, you were also wrong. OK, maybe not wrong, but palladium was the real star (although not as great a star as rhodium which has gone really supersonic recently). Let’s look at the chart below once again – the white metal skyrocketed from $1,900 to almost $2,500 in January!

Actually, palladium has reached a record high, as the chart below shows. Compared with April 1990, when our data series starts, the price of palladium increased almost twentyfold, from around $130 to almost $,2,500. It means that palladium is currently more expensive than gold or platinum!

Surprised? You shouldn’t be! After all, we wrote as early as in the July 2017 edition of the Market Overview that

the price of palladium should be supported in the near future. We know that the above-ground stocks of palladium are relatively plentiful (and may be greater than the market expects), but market deficits at such heights cannot last indefinitely – and when the market eventually tightens, prices will need to rise.

And in March 2019, we again commented on palladium, writing that it had better prospects than platinum:

the underlying structural deficit grew last year and, what is more important, is expected to widen in 2019, which will not be without significance for the price of palladium (…)

And given that the latter metal [palladium] has better fundamentals (platinum market is in structural surplus, while palladium market is in deficit), it still seems to be a better investment choice. Although it is true that the automotive demand for platinum should stabilize in the near future, and the rising price discrepancy should make platinum more attractive as catalyst, the autocatalyst producers say that they are not seeing broad-based substitution from palladium to platinum. Hence, the outlook for platinum improved, but the path for the palladium is still better.

It turned out that we were right again. As we explained in the past, the underlying cause of the spectacular rise in the price of palladium boils down to the fact that demand has been greatly outpacing supply. And why have we seen structural deficits? The first reason is the rise in the automotive demand for palladium due to the tighter emission legislation and stricter vehicle testing regimes. The key here is that palladium – in contrast to platinum used mainly in diesel engines which are out of favor – is used predominantly in gasoline vehicles (and in hybrid electric vehicles, which tend to be partly gasoline-powered). Second, South Africa’s output of palladium has recently decreased due to power outages at local mines and tense political situation in this major producer of palladium.

Implications for the future

Where is the palladium market heading? Well, given that it’s likely to remain in structural deficit, price may go further north. However, the price chart of palladium looks parabolic, so – if history of parabolic price movements teaches us anything – it appears unsustainable. So, the correction is likely – actually, the price of palladium has already declined to $2,265 and the decline won’t end at this level.

More generally, platinum might now the better choice than palladium at current prices. This is because the big hit from the Volkswagen diesel scandal has been already absorbed in the platinum prices. And with palladium trading twice as more than platinum, the substitution should kick in, supporting platinum relative to palladium.

(By Arkadiusz Sieron)

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Trading Alerts.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments