No new year resolution for out-of-favour copper market

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

New year but same old problems for Doctor Copper.

The copper market remains decidedly out of favour among the investment community with fund positioning extremely light by historical standards.

London Metal Exchange (LME) three-month metal briefly broke back up above the $10,000-per tonne level last week but collapsed again on Friday.

Last trading around $9,650, the copper price seems too high to attract fresh buying but global inventory is too low for bears to dare short it.

The resulting lack of resolution has seen trading volumes on all three major venues fall in recent months as speculators chase more enticing narratives in other metals such as nickel, aluminum and zinc.

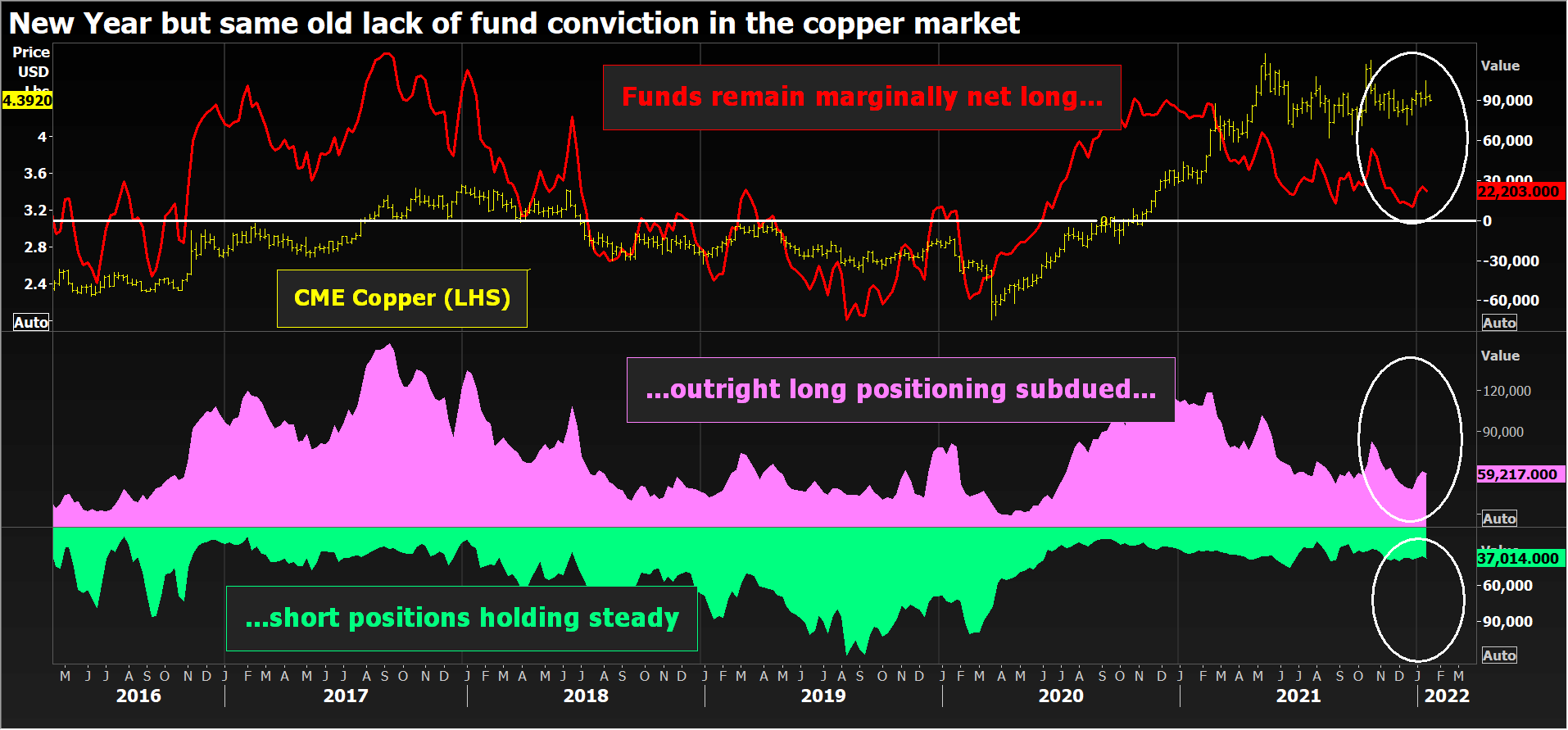

/cloudfront-us-east-2.images.arcpublishing.com/reuters/GRHWR4YQTFJNZDHD6CGDJWFVDE.png)

Money manager positioning subdued

Money managers remain net long of the CME copper contract but bull enthusiasm is low at 22,203 contracts, according to the latest Commitments of Traders Report showing the state of play at the close of Jan. 11.

This time last year, when copper was trending strongly higher, the collective bull positioning stood at 76,449 contracts. The record high was set in 2017 at 125,376 contracts.

Recent shifts in money manager positioning have been almost exclusively derived from the long side with fund short positions little changed over the last two months.

The lack of investor participation is mirrored in the London market, where the money manager net long of 29,912 contracts is a long way off last February’s record high of almost 48,000 contracts.

It’s worth noting that LME broker Marex Spectron, which uses its own methodology to track speculative flows, estimates funds are running net short of copper to the tune of around 24,000 lots. Funds are also short of aluminum – but to a lesser extent than copper – and net long all the other core LME metals, according to Marex.

Trading volumes slump

Copper’s fall from grace among fund players is also clear to see in sliding volumes across all three major trading venues – LME, CME and the Shanghai Futures Exchange (ShFE).

Activity on the LME’s copper contract shrank by 7.0% last year, making it the second poorest performer among the London market’s core base metals suite.

Only tin fared worse, registering a 15% year-on-year slump in volumes, reflecting the soldering metal’s combination of record high pricing and record low inventories.

The CME copper contract saw the second year of anemic growth, futures volumes up just 1.1% last year on 2020 levels.

Activity on the ShFE contract grew by a more robust 12% last year but the headline figure flatters to deceive, reflecting high volumes in the first half of the year as activity recovered from the previous year’s COVID-induced slump.

The big picture was of falling copper volumes across the board in the second half of 2021. In December, average daily volumes were down 16% year-on-year on the LME, 25% on the CME and 44% on the ShFE.

The latter two saw some offset from higher options volumes, suggesting investors were looking to express a view on copper price direction without committing to an outright futures position, a trading strategy typical of a range-bound market.

Conflicted narrative

Copper’s twin problems are directionless trading and a lack of convincing narrative at current elevated prices.

The market has been largely unaffected by the power crunches in China and Europe which have excited speculative interest in metals such as aluminum and zinc.

Nor is there any consensus as to what the next major move might be.

Goldman Sachs remains firmly in the bull camp, targeting copper to hit $12,000 per tonne on a 12-month basis.

The bank is forecasting a supply-usage deficit of 197,000 tonnes this year. Given that global visible exchange inventory stood at 190,000 tonnes at the end of December, there is the potential for scarcity pricing such as seen on tin, which continues to hit record price highs on a regular basis.

Others, however, are not convinced.

Citi, which is a longer-term bull, thinks that copper is due to a significant price correction, targeting an 8% decline over the next one or two months.

Core to the bank’s view is an expectation that Russian shipments of copper will accelerate after the expiry of a temporary 10% export tax.

Citi estimates Russia accumulated around 150,000 tonnes of copper stocks in the four months after the tax was introduced in August. That metal should hit the market over the first quarter of this year, lifting depleted LME stocks and simultaneously depressing market sentiment, the bank argues.

LME stocks jumped by 6,550 tonnes to 92,850 tonnes on Monday, largely thanks to 4,175 tonnes of arrivals at Rotterdam, which might be evidence of this destocking already happening.

Time-spreads have calmed since the exchange was forced to step into the market in October, the benchmark cash-to-three-months period closing last week at a minimal backwardation of $12.50 per tonne.

Inventory could be a key determinant of whether copper breaks up or down from its current holding pattern.

But it’s clear that funds are waiting for a stronger signal before recommitting to Doctor Copper.

(Editing by Jane Merriman)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments