Nickel’s sizzling rally cools, but not over yet

Nickel’s spectacular rally over the last month, based on ore shortages and robust demand from China’s stainless steel mills, still has momentum, but as supplies rise and demand dwindles, prices will retreat.

Prices of nickel on the London Metal Exchange, near 14-month highs at around $16,000 a tonne, have climbed 10% since Oct. 2 and 45% since March, when coronavirus lockdowns and stalled manufacturing activity hit prices of industrial metals.

Faced with Indonesia’s ban on nickel ore exports since January, China’s nickel pig iron (NPI) producers have been using stocks they acquired before the ban took effect.

“It’s the climax of the Indonesia ban, it’s going to get extremely expensive to produce nickel in the next couple of months,” said Citi analyst Oliver Nugent.

“China’s NPI producers…will keep trying to outbid each other for the available units, until they can’t afford to.”

Citi’s 0-3 month target for the nickel price is $16,500, while for 6-12 months its forecast is $14,000.

Also likely to undermine nickel prices is Indonesia’s NPI output, expected to rise to between 690,000-800,000 tonnes next year from 560,000-600,000 tonnes this year.

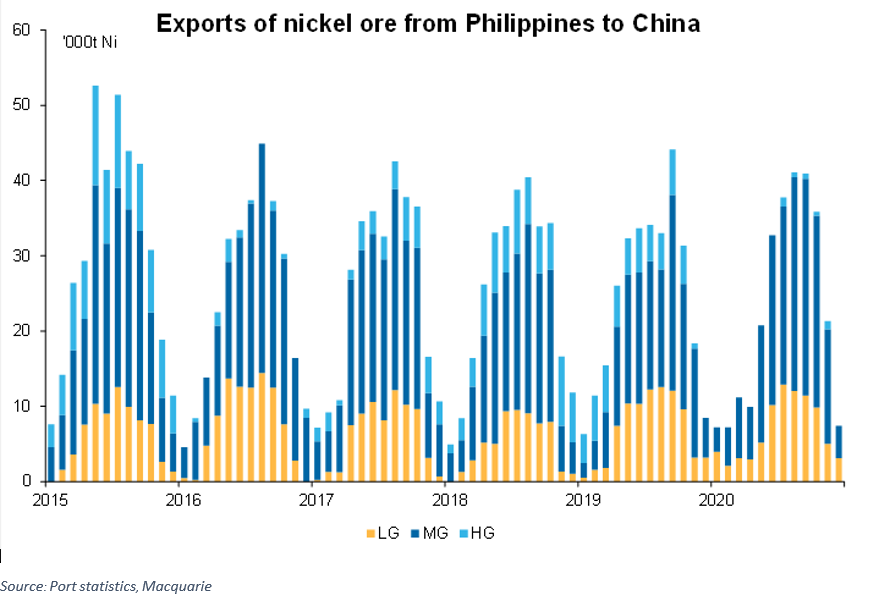

But before then, shortages of nickel ore will be aggravated by the rainy season in the Philippines, which is likely to disrupt supplies until at least January, after which exports typically resume.

Robust demand from stainless producers, accounting for about two-thirds of global nickel demand estimated at around 23 million tonnes this year, has boosted prices.

“Preliminary soundings on October (stainless steel) production suggest it will remain solid at near record levels with Indonesian production rising to new record highs,” said Jim Lennon, a metals strategist at Macquarie.

“However, over the past month stocks have started to rise again…and stainless steel price rises have stalled.”

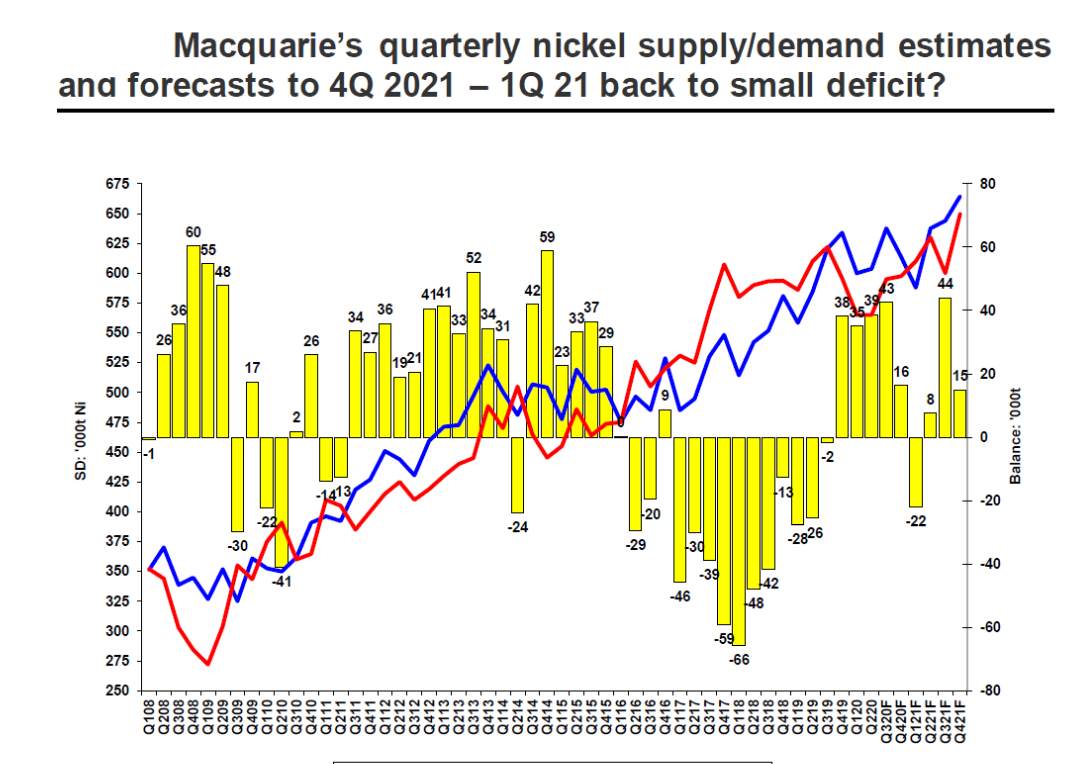

Macquarie expects the nickel market surplus to shrink to below 20,000 tonnes in the fourth quarter from a surplus above 40,000 tonnes in the third quarter. It expects a small deficit in the first quarter of next year before surpluses reappear.

(By Pratima Desai; Editing by Barbara Lewis)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments