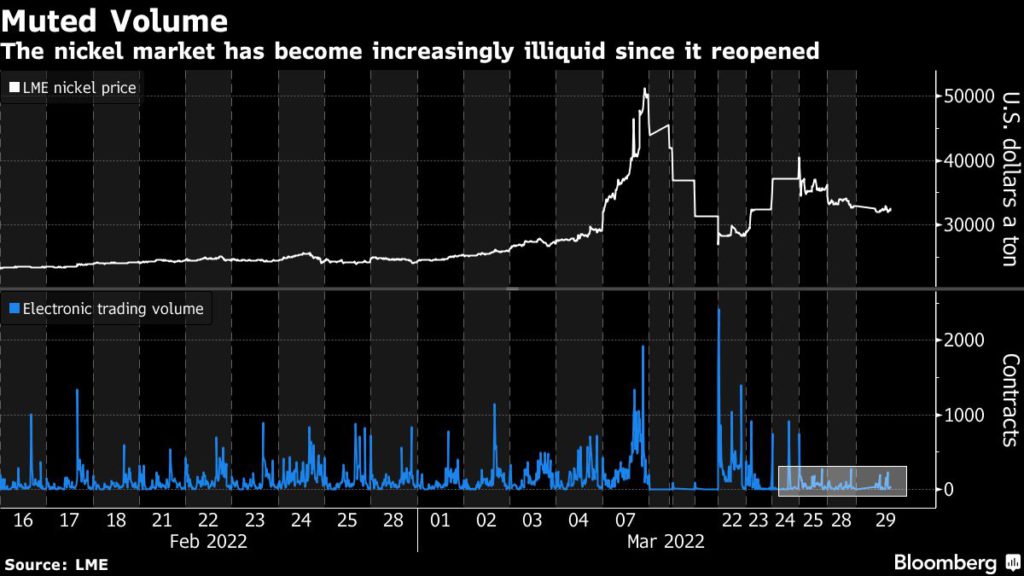

Nickel paralysis deepens as battered LME market barely trades

Nickel trading volumes continue to collapse on the London Metal Exchange in the wake of an historic short squeeze, setting up a liquidity crisis in the market for one of the most crucial industrial commodities.

The LME halted nickel trading and canceled nearly $4 billion worth of transactions earlier this month after prices spiked by 250% in under two days, as it sought to protect its brokers from huge margin calls owed by Tsingshan Holding Group Co. and other short position holders.

After a haphazard effort to restart trading, nickel has spent much of the past fortnight locked at the upper or lower limit of a new daily price cap designed to rein in the unprecedented volatility.

Yet the market has remained in near-paralysis, even on days when prices have been trading within the 15% daily limit. Fewer than 210 lots had traded in the first hour after the market opened at 8 a.m. on Tuesday, down nearly 60% from the 90-day average for that time of day before this month’s trading halt.

There was a small bump in trading activity in the afternoon as Russia announced that it will sharply cut military operations near Kyiv and Chernihiv, but electronic volumes remained depressed. Nickel traded 1.9% lower at $32,120 a ton at 3:11 p.m. London time, with fewer than 1,350 lots traded electronically. Aluminum dropped 5.3% to $3,422 a ton, as the prospects for a de-escalation in Ukraine eased anxiety over supply from Russia.

“The LME need a few sessions where nickel is trading like a proper commodity,” said Colin Hamilton, managing director for commodities research at BMO Capital Markets.

While Tsingshan owner Xiang Guangda started buying contracts on the LME last week to reduce his massive short bets, the businessman and his allies only reduced a portion of their total short position, and still held large bets on falling prices, Bloomberg reported last week. Many other industrial consumers and physical traders also have large short positions in the market.

The plunging liquidity represents an escalating crisis for producers and consumers who rely on the exchange to hedge their pricing risk.

Usage is growing rapidly in electric-vehicle batteries, and the illiquid trading conditions on the LME threaten to exacerbate volatility. That will hit car-makers — who’ve already seen a neck-breaking rally in battery metal prices over the past year — as well as the steel mills that account for the lion’s share of demand today.

The increasingly urgent question among core users is whether the 145-year-old exchange is still a viable mechanism for industrial companies seeking to hedge their price risk, as well as the traders and investors who have helped make nickel one of the bourse’s most successful contracts.

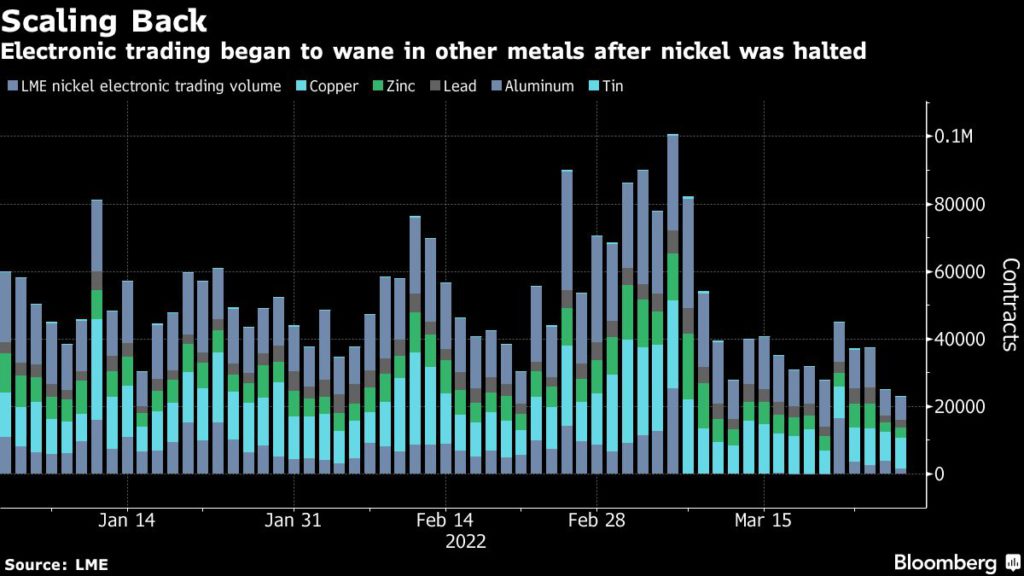

The trend isn’t limited to nickel either. Trading volumes have dropped significantly in the larger copper and aluminum markets since the LME’s controversial intervention earlier this month and the crisis has raised questions about the bourse’s status as the world’s benchmark futures market.

(By Mark Burton)

Read More: LME nickel price limps back but tensions are not going away

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments