Miner M&A spotlight may shift to Teck and Freeport

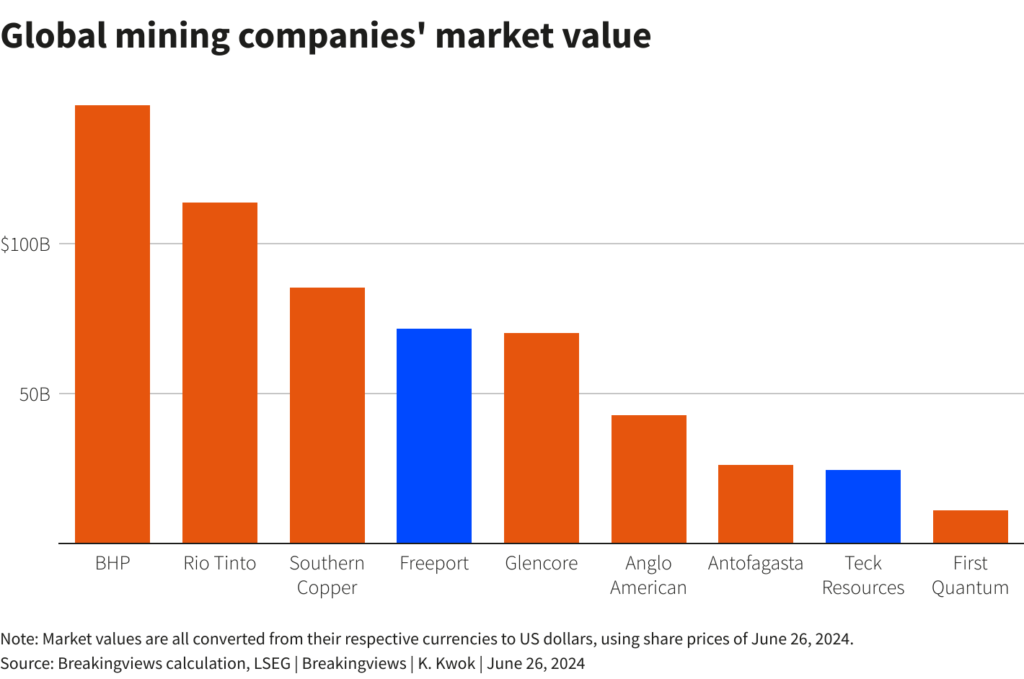

Mining bankers are all dressed up with nowhere to go. Now that BHP’s attempt to take over the non-South African parts of rival Anglo American has hit the skids, the question is where the M&A spotlight is next going to fall in a sector newly buzzing with intrigue. The smart money right now seems to be on something involving Canada’s $25 billion Teck Resources, or $72 billion New York-listed Freeport-McMoran.

BHP’s Anglo interest, which petered out on May 29, has focused everyone’s minds on copper. Demand for the red metal is robust given its key role in the energy transition and an artificial intelligence-related data centre boom, but supplies are constrained. BHP boss Mike Henry’s three rebuffed takeover proposals for Anglo, the last of which valued the target at $47 billion, suggest big miners reckon it’s cheaper to buy new supplies than invest in new ones.

That said, it’s not immediately obvious who’s next on the block. Henry could wait the mandatory six months and have another pop at Anglo, but he’d still have to work out how to separate the UK-listed miner’s juicy copper mines from the other bits he doesn’t want. Anglo boss Duncan Wanblad, meanwhile, is unlikely to be an M&A aggressor — his successful defence against BHP requires him to spend the next year or so hiving off problem areas like diamonds. Rio Tinto, the other big global mining beast, was assumed to be waiting to pounce on other targets while BHP was distracted swallowing Anglo — which it now isn’t.

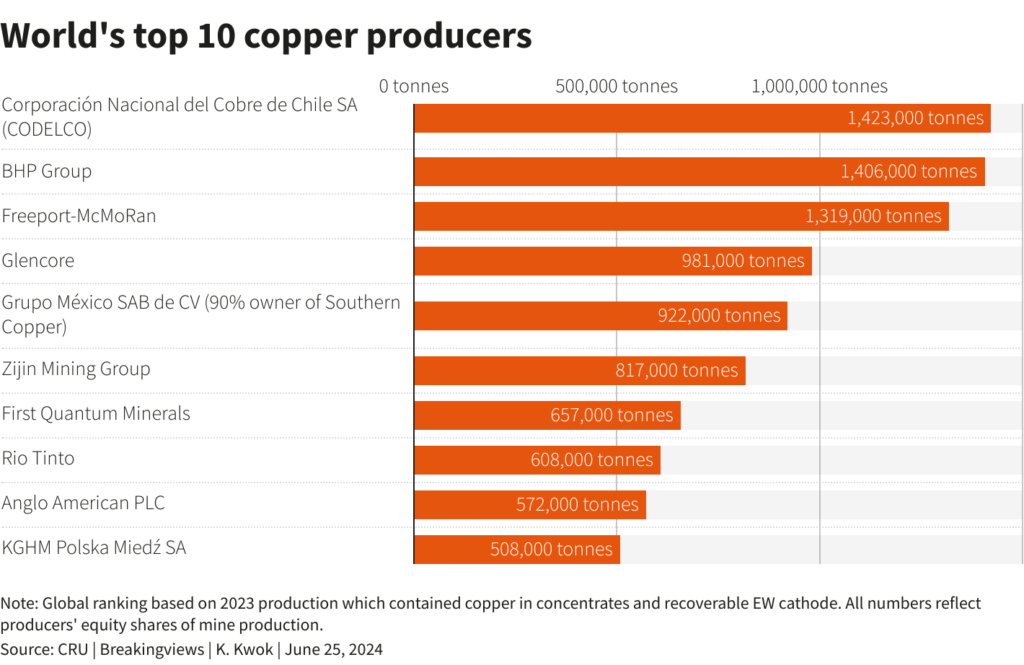

The picture doesn’t necessarily get any clearer in the next echelon down. Major copper-focused players include $26 billion Antofagasta, whose shares have doubled in the last two years, and $85 billion Southern Copper. These boast annual production of over 600,000 tonnes and 900,000 tonnes respectively. But Antofagasta is 65% owned by Chile’s Luksic family, which isn’t showing signs of selling, and Southern Copper is 90% held by Grupo México – led by Mexican tycoon Germán Larrea Mota-Velasco. Canada’s $11 billion First Quantum Minerals had over 700,000 tonnes of annual copper output last year, but its Cobre Panamá mine in the Central American state has been embroiled in a spat with the domestic government.

Freeport, which is in contrast largely held by institutional investors, looks a more promising M&A candidate. CEO Kathleen Quirk, who took the reins this month, needs to find ways to make her equity story more exciting: analysts expect Freeport’s copper production to barely increase in the next five years at 1.3 million tonnes annually, according to estimates polled by Visible Alpha. She also recently conceded in a Financial Times interview that acquisition, while not her priority, was an effective way to boost copper output.

Teck is alluring for a starker reason. Boss Jonathan Price’s copper production could roughly double to nearly 600,000 tonnes by 2028, according to analysts estimates using Visible Alpha data, and Teck’s 60% copper EBITDA margin forecast for 2025 exceeds Freeport’s 45%. While the Keevil family exerts an Antofagasta-style grip on the shareholder register, its special voting shares will flip to common stock in five years. After he completes the sale of Teck’s steelmaking coal business to Swiss rival Glencore, Price’s group will become a hugely attractive target.

The catch for interested parties is that this allure is substantially already in the prices of the more focused base metal players. Freeport’s shares have gained 360% in the past five years, compared to 17% for less copper-exposed Rio, BHP and Anglo. After deducting the earnings generated by coal, Teck is trading at 12.4 times the remaining EBITDA analysts estimate it to generate in 2024, using Visible Alpha data, with Southern Copper at 14.6 times and Freeport and Antofagasta at 7 times. Add a premium on top of that and Henry and his more diversified miner peers will be at severe risk of overpaying: BHP, Rio and Anglo trade on average at just 5 times, so the danger is they hand all the synergy benefits to their targets’ shareholders.

This doesn’t mean Teck and Freeport have no hope of being involved in big M&A. That’s because they could use their expensive shares to become acquirers. There are plenty of options. Teck’s $25 billion value gives it nearly the same market capitalization as Antofagasta, while Vale’s base metal business was valued at a similar price when it sold a one-tenth stake to shareholders including Saudi Arabia last year. Price, or his counterparts at Freeport or Southern Copper, could use their equity to broker an all-share merger with one of this cohort.

Anglo and Glencore could be in play too. After spinning off its coal, diamond and platinum businesses, Anglo would be smaller, but more exposed to base metals. Value its $3.8 billion of estimated copper EBITDA in 2024 at the same level as pure metal players like Freeport, and it would be worth $27 billion. Wanblad may also feel the need to spin out his base metals business pre-emptively if he fails to deliver Anglo’s restructuring plan by 2025. Meanwhile, Glencore is trading at only 4.6 times 2024 EBITDA. If it decided to spin off its massive coal businesses, the likes of Freeport might fancy what’s left behind — analysts estimate Glencore’s own copper business will generate $4.8 billion of EBITDA in 2024, implying a potential valuation nearing $35 billion on Freeport’s 7 times multiple.

It’s not impossible antitrust hurdles lie in the path of any Teck or Freeport M&A splurge. The Canadian government, after all, wasn’t overly welcoming towards Glencore’s bid for the entirety of Teck in 2023. Rather than engage in risky M&A, Teck or Freeport may yet prefer to spend resources on new technologies to squeeze more copper out of their own existing projects. Still, it wasn’t at all clear BHP would swoop for Anglo due to the complexity of the political backdrop, and it did so anyway. Copper watchers should stay tuned for further fireworks.

Context news

Freeport-McMoRan chief executive Kathleen Quirk said in a Financial Times interview published on June 17 that reducing the sector from scores of groups into a small number of giants could be an effective way to buoy supplies needed to cut emissions in the decades ahead.

Quirk took charge as chief executive of Freeport on June 11. Glencore’s deal to buy Teck’s coal mines is expected to close in the third quarter.

(The author, Karen Kwok, is a Reuters Breakingviews columnist. The opinions expressed are their own.)

(Editing by George Hay and Streisand Neto)

More News

Gold price drops 3% on US jobs data beat

Spot prices fell as much as 4% to $4,880 per ounce, before parsing some losses.

February 12, 2026 | 10:09 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Bill warby

Why will nobody buy the 49% of the woodsmith mine