LME’s twilight zone absorbs stocks build

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

London Metal Exchange (LME) stocks of aluminum fell by 132,500 tonnes over the course of 2020.

This is a surprising outcome, given the size of the covid-19 hit to global manufacturing activity. The last time metals demand suffered a similar collapse was during the Global Financial Crisis of 2009, when LME aluminum stocks almost doubled to 4.6 million tonnes.

That, however, was a credit crisis. The covid-19 crisis isn’t. There has been no pressing need for the physical supply chain to deliver unsold metal to the market of last resort.

Rather, surplus metal is being stored in the off-exchange statistical shadows. Happily, we now get to see some of it thanks to the LME’s “off-warrant” stocks reporting initiative.

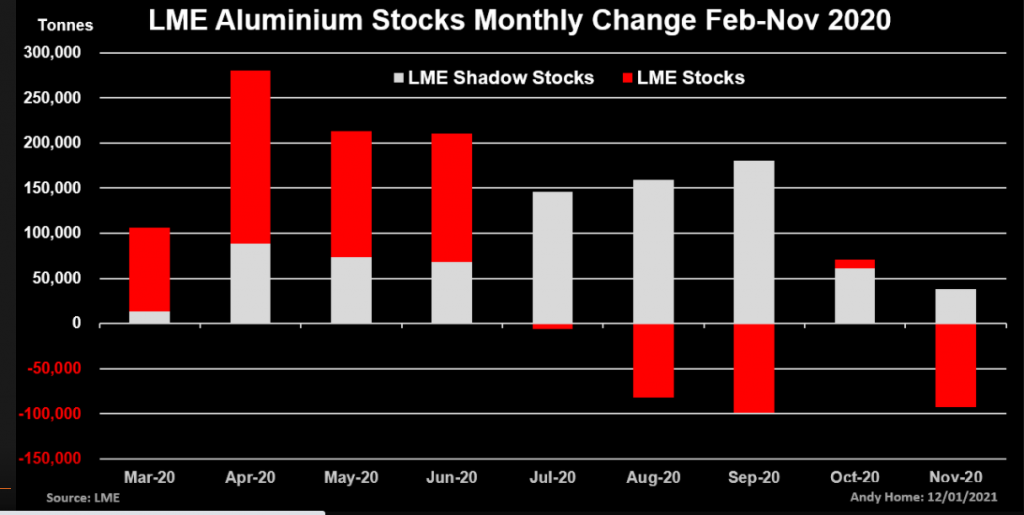

The amount of aluminum sitting in this LME twilight zone grew by 829,000 tonnes between February and November, by which stage shadow inventory of 1.66 million tonnes exceeded visible exchange stocks of 1.37 million.

Total LME aluminum stocks, registered and shadow, surged by 1.12 million tonnes over the same period, which seems a more accurate inventory reflection of last year’s turmoil.

The inventory picture is still far from complete. There is undoubtedly much more metal sitting in the deeper storage shadows but tracking these LME twilight stocks offers some important clues to current market dynamics.

Twilight zone

It’s important to understand what the LME’s “off-warrant” monthly report, released with a one-month time-lag, can and can’t throw light on.

The report captures metal that is being stored under an agreement requiring the use of LME-registered warehouses, or an agreement explicitly providing for potential future LME warranting.

The exchange originally included a voluntary reporting category but, not surprisingly given the commercial sensitivities of the physical supply chain, has received “very little data”.

It has reserved the right to try to encourage more voluntary reporting through a possible warranting fee adjustment.

So the report can’t capture metal that is being privately stored with no intention of, or contractual reference to, LME delivery.

But it does open up the twilight LME warehousing zone that has emerged over the last decade in response to high on-exchange storage fees.

Such LME shadow storage is a neat cost-benefit compromise – cheaper than on-warrant storage but without the higher financing costs of totally off-market storage.

Financing banks like knowing stocks can be immediately fungible if necessary and shadow stocks can often be “delivered” onto LME warrant at the stroke of a keyboard.

This is why the LME’s daily stocks report can be so “noisy” as large tonnages circulate between on-warrant and off-warrant inventories in search of cheaper warehousing deals.

Shadow stocks

The LME’s daily stocks reports represent one of the few hard datasets in the industrial metals markets, but they have lost much of their signaling power as shadow warehousing has grown.

The new monthly report is intended to provide “visibility over a broader set of material”, allowing the market to trade on “the basis of a more holistic supply story”, the LME has said.

Which it does.

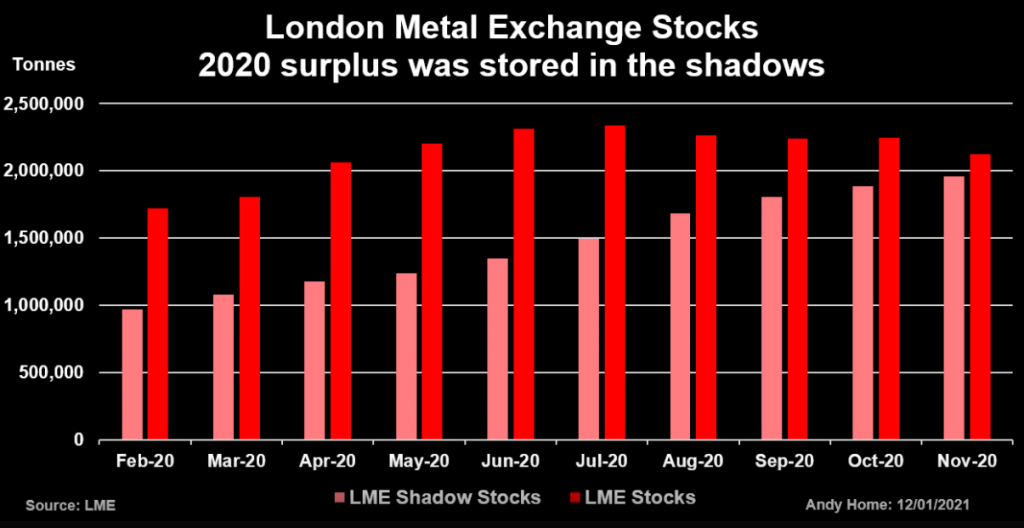

The report reveals the existence of a twilight stockpile almost as big as that showing up in the LME’s daily figures. Total shadow inventory was 1.96 million tonnes at the end of November, compared with registered stocks of 2.13 million.

The first 10 months’ data show that while LME registered stocks of all metals grew by 407,000 tonnes through November, the increase in shadow stocks was a larger 985,000 tonnes, much of it aluminum.

Month-on-month changes in shadow stocks can be difficult to interpret, given the circular movement on and off warrant as metal owners seek out cheaper storage deals.

However, broader trends can be discerned, such as last year’s big off-exchange build in aluminum stocks, which makes market optics look a lot less bullish than LME-registered stocks suggest.

Mixed signals

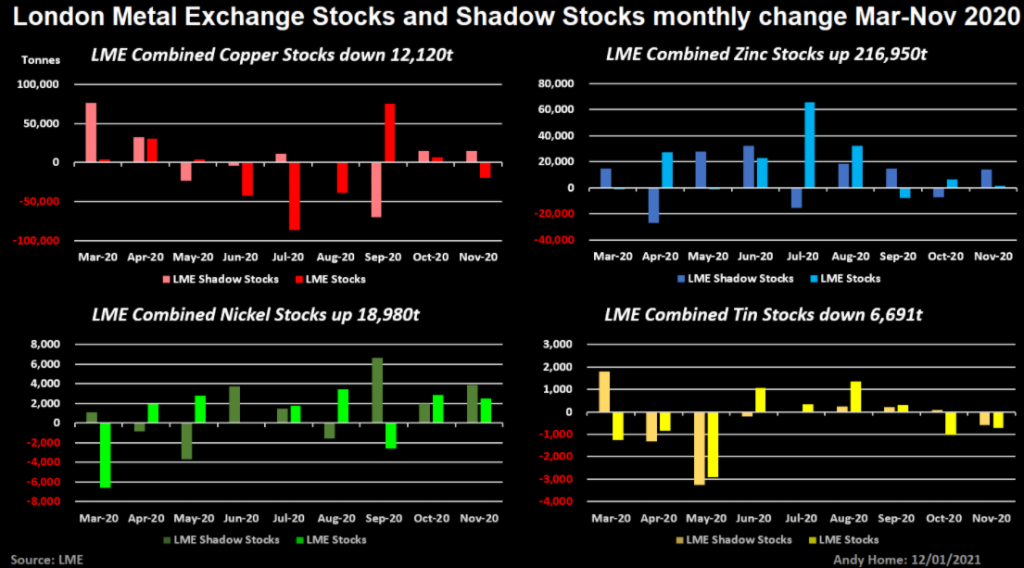

Shadow stocks of zinc, lead and nickel also increased over the February-November 2020 period even as on-warrant inventory rose.

In the case of zinc, a 145,300-tonne increase in LME stocks was complemented by a further 71,650-tonne build in shadow tonnage.

Off-warrant zinc stocks totalled 97,312 tonnes at the end of November. The largest concentration – 58,240 tonnes – was at New Orleans, a perennial favourite for physical zinc traders due to its geographical insulation from regional premium markets.

Tin sits at the bull end of the stocks spectrum, with both LME and shadow stocks declining last year

Off-warrant nickel stocks grew by 12,900 tonnes between February and November, complementing a smaller 6,100 rise in registered stocks.

Shadow stock builds simply reinforce bearish optics in such markets, all of which are thought to have registered significant supply-demand surpluses last year.

On the flip side, shadow stocks movements of both copper and tin accentuate the bullish optics of falling on-exchange inventory.

The LME twilight zone held 130,460 tonnes of copper at the end of November, compared with on-exchange stocks of 149,925 tonnes.

Shadow stocks built by 54,900 tonnes through November 2020, but that only partly compensated for the sharp decline in registered stocks. Combined LME copper stocks actually fell by 12,120 tonnes between February and November.

That attests to the scale of buying from China, which has effectively cleared the rest of the world’s covid-19 surplus.

Tin sits at the bull end of the stocks spectrum, with both LME and shadow stocks declining last year.

LME tin stocks slumped by 74% to just 1,860 tonnes over the course of 2020. Inventory has shrunk further to just 1,660 tonnes over the first days of 2021 with time-spreads flaring out in response.

Anyone looking for relief from off-warrant inventories may be disappointed, however. As of the end of November there were precisely zero, compared with a March peak of over 4,841 tonnes.

It doesn’t mean there’s no tin “out there” being stored in warehouses away from the LME, but it does mean that the twilight zone is depleted.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments