Lithium’s next big risk is grand supply plans falling short

Electric-vehicle makers are hoping that an imminent wave of lithium supply will bring relief for their expansion plans after a two-year squeeze, but the battery metal’s die-hard bulls warn of more pain to come if producers fail to deliver.

Rampant lithium demand has caught many forecasters by surprise, with booming global EV sales causing consumption to double over the past two years. With suppliers unable to keep pace, a blistering price rally sent the total spot value of lithium consumption rocketing to about $35 billion in 2022, up from $3 billion in 2020, according to Bloomberg calculations.

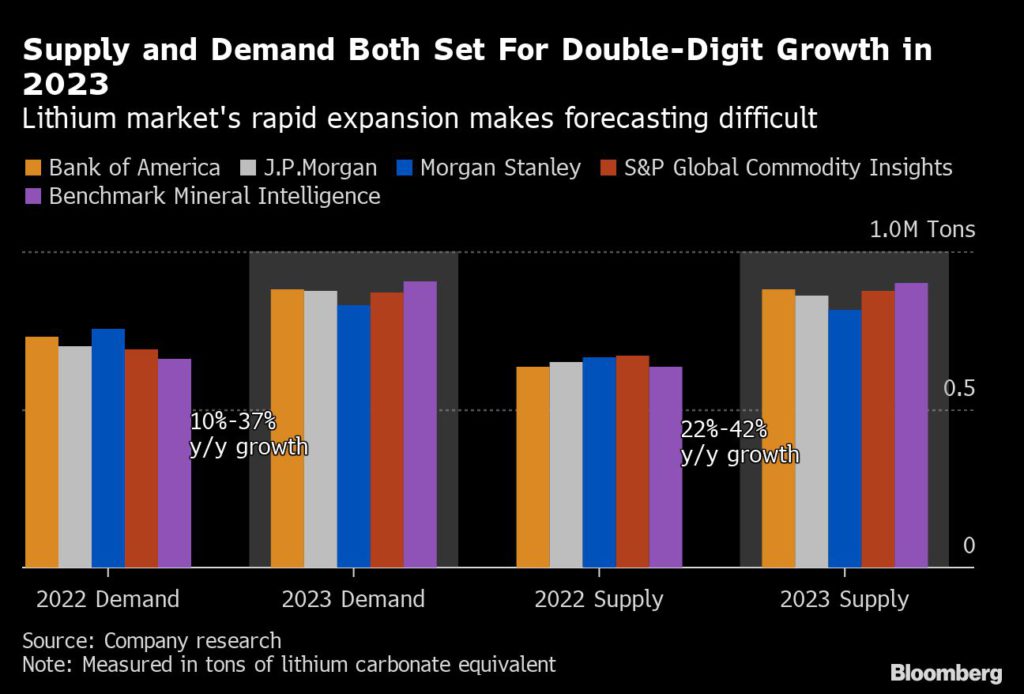

Some bearish lithium-watchers say fast-growing supply, rather than dizzying demand, will be the decisive factor in 2023. Five analyst forecasts reviewed by Bloomberg point to a much more balanced global market after clear shortages in 2022, while BYD Co., China’s top EV seller, is counting on a lithium surplus.

But there are many skeptics who warn of fresh tightness if miners from Chile to China and Australia hit hurdles in launching daunting volumes of new supply. The reviewed forecasts peg production increases of between 22% and 42% in 2023: a breakneck pace for any complex extractive industry.

“I really don’t think there’s any reason to believe that so many tons can magically appear this year to return the market to balance,” Claire Blanchelande, a lithium trader at Trafigura Group, said by phone from Geneva. “The pain is not over yet.”

At stake is the pace at which the world’s vehicle fleet adopts battery power. Lithium-ion battery costs rose last year for the first time in the EV era, according to BloombergNEF. Elon Musk bemoaned lithium’s “insane” rally and said high raw material costs were among Tesla Inc.’s biggest headwinds.

Not matched

There’s broad agreement that lithium supply is heading for a major increase in 2023 as a wave of expansions or new projects get up and running. The more bearish voices say that supply wave will hit the market just as China’s withdrawal of generous EV subsidies causes demand to cool, creating a mismatch that could trigger a sharper fall in prices.

Average prices this year are likely to fall about 8% from average 2022 levels, according to the mean of five forecasts reviewed by Bloomberg.

The divisive issue is whether less-established producers will be able to deliver in full, defying a range of regulatory, technical and commercial challenges. The extraordinary pace of lithium’s expansions – across both demand and supply – has made forecasting the market a contentious pursuit.

“2023 is when lithium becomes what I call a volume game,” said Chris Berry, president of House Mountain Partners, a consultant to the battery-materials sector. “We need to see a supply response from both existing producers and near-term producers who will need to execute flawlessly in the face of sustained lithium demand.”

Softer market

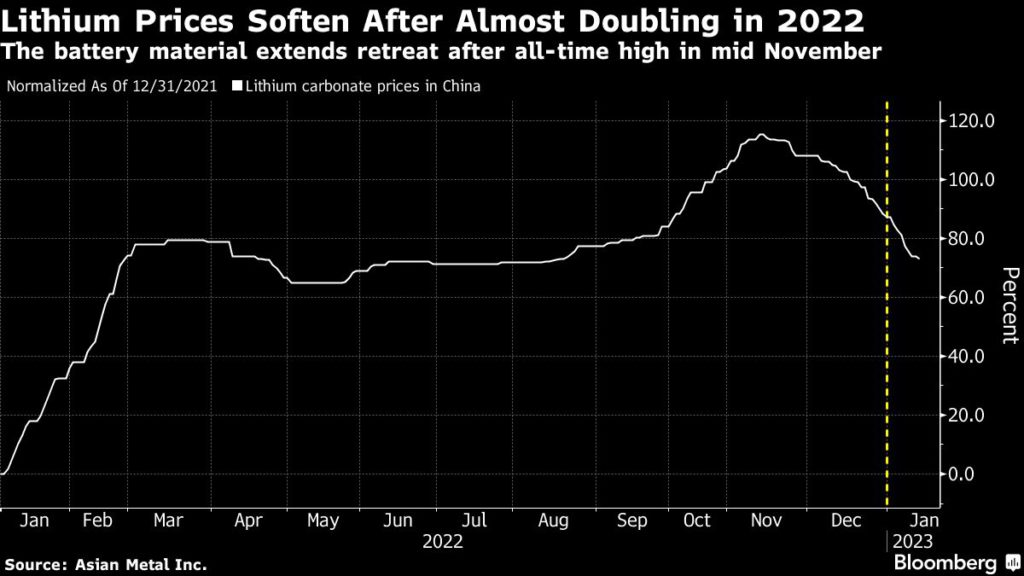

Lithium prices have already come down about 20% from an eye-popping record in November, in an early sign of respite for buyers. Lithium carbonate in China fell to 480,500 yuan a ton ($71,500) on Jan. 13, the lowest since August.

“I think you’re going to see a short dip in spot prices in 2023 but I don’t see that as a problem,” Joe Lowry, founder of advisory firm Global Lithium. “If we were talking five years ago today, the biggest issue that lithium industry had was lack of investment. Now the most significant problems are permitting and project execution.”

A cause for optimism on supply is that the largest increases will be coming from veteran top producers like Albemarle Corp. and Chile’s SQM that are considered more likely to succeed. But they only account for about a third of anticipated increases in 2023, according to data from BMO Capital Markets.

The next tier down is a small army of nascent lithium producers who will need to prove they can get up and running. And beyond those, there’s unconventional new sources like lepidolite — a lithium-bearing mineral that’s emerging in China as a serious option. JPMorgan Chase & Co. called it “one of the largest threats” to prices.

But it’s also a controversial topic, with some specialists saying it’s costly and environmentally harmful to convert in large volumes for battery use.

“We will see more lepidolite be brought online in China in 2023,” Cameron Perks, analyst at Benchmark Mineral Intelligence said. “But we won’t see as much as being predicted by others. Give it five or 10 years, and it will increasingly become an important part of the market.”

All of this means the path to supply and cost relief for carmakers is fraught, even before considering the demand side of the ledger.

No collapse

For now, China’s withdrawal of EV credits, as well as uncertainties over the pandemic and global economy, are weighing on the outlook. But a faster-than-expected reopening of China’s economy, and the rest of the world escaping a deep slump, could yet deliver an upside surprise.

“The market consensus and the consensus that I would agree with is that in 2023 pricing is likely to plateau, with perhaps some potential for downside but by no means do I see any sort of a pricing collapse,” said Berry of House Mountain Partners.

(By Annie Lee and Mark Burton)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments