Lithium market struggles to recover after epic boom and bust

A stuttering recovery in lithium prices is providing a fresh reminder of why the dramatic rally of recent years was followed by an even more breathtaking collapse: a fast-expanding industry that is more prepared than ever to keep pumping out supplies.

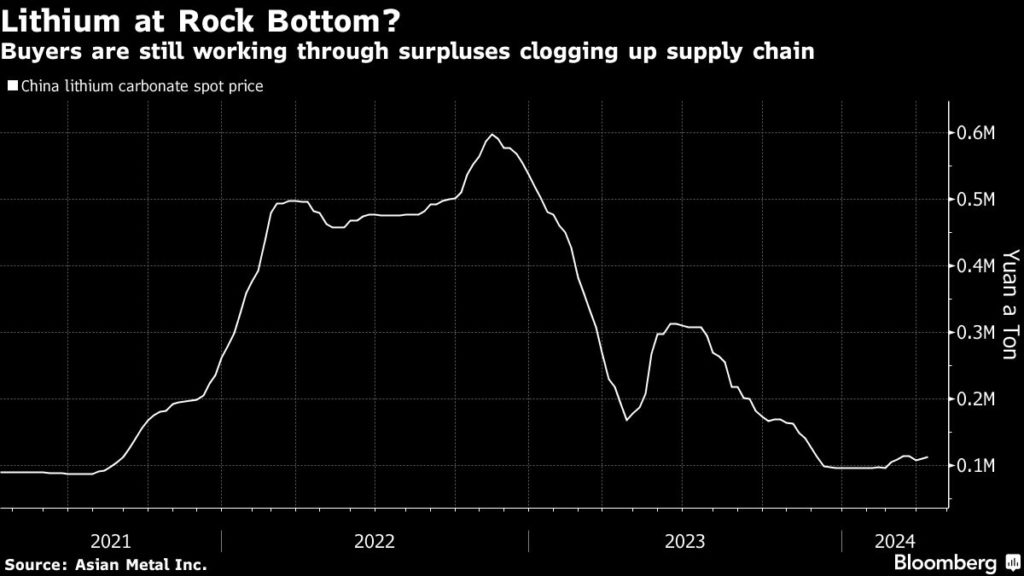

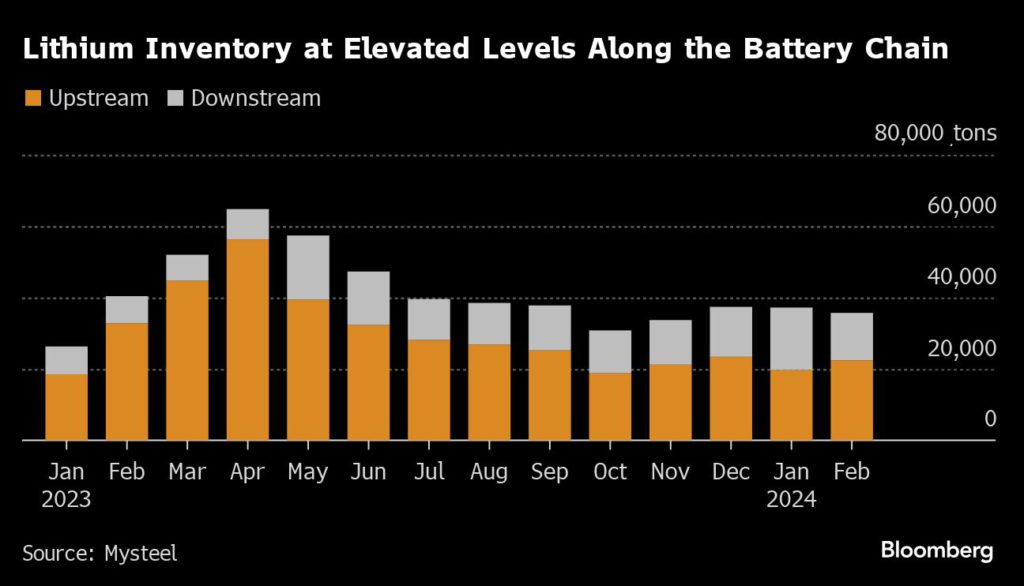

Prices have bottomed out but have struggled to meaningfully rebound, partly because miners, refiners and carmakers are still working through a mound of surplus stock clogging up the supply chain. And while some projects and mines were hurt by the pricing plunge, several of the biggest producers insist they’ll keep expanding into the glut, further clouding the outlook for an eventual recovery in prices.

A vital component in rechargeable batteries, lithium has been thrust into the global spotlight as one of the world’s most important commodities. The boom and bust of the past three years has exposed a once-niche and tiny market that is evolving and adjusting in real time to the unprecedented rollout of electric vehicles across the globe.

For much of the past year, that has meant reconciling a massive new wave of supply that caught many by surprise, while evidence mounts that EV demand is coming in weaker than expected.

Now, a key question facing the industry is whether it’s doomed to repeat the cycle over again. Sharp spikes and plunges make planning difficult for both miners and their customers, but a prolonged bear market on the other hand would put pressure on smaller producers and increase concentration among a handful of powerful suppliers.

While many analysts and miners still expect prices to rebound substantially over the next few years as demand gathers pace, a faster flow of supply from a more diverse global mining base could mean the next boom-and-bust cycle will be shorter and less extreme — perhaps pointing to a maturing market.

“When the thing turns, will there be a ridiculous spike like there was last time? I hope not,” said Joe Lowry, founder of advisory firm Global Lithium LLC. “You’re just going to bring in more garbage into the system and more volatility, which makes it harder for everybody.”

For many lithium bulls, the sudden swing to a global surplus has meant coming to terms with the idea that Elon Musk may have been right: there’s a “ridiculous” amount of lithium around the world, and the true supply constraint lies in refining it into battery-grade chemicals. There is also a growing awareness among producers that pricing blowouts increase the likelihood that carmakers seek to avoid lithium altogether in their future batteries.

As EV demand and investment exploded early this decade, the lithium industry initially struggled to keep up. Forecasts of huge shortages drove panic buying among carmakers, which rushed to ink supply deals and even bought directly into mining projects to guarantee access to metal. Prices soared to once-unthinkable levels, prompting warnings that excessive costs would put the very future of the EV industry at risk.

But then the bubble popped. The high prices drew a wave of supply, including from new, small scale producers in places like China and Australia, which operate at high costs but can quickly switch on and off depending on the strength of the market.

Prices collapsed, falling as much as 84% from the peak, as companies that had frantically stocked up were now stuck with massive inventories they are still working through. The result was an effective buyers strike that dragged on for a large part of last year.

The industry is still sitting on a big volume of inventory — of mined ores, lithium chemicals, batteries and electric-vehicles themselves — although a bounce in Chinese prices over the past month signaled that some buyers at least are making a tentative return.

Lithium miners have been hit hard by the plunge — top producer Albemarle Corp. reported a loss in the fourth quarter, while others have also seen their earnings plunge dramatically.

But for some of the key players, the biggest lesson from the recent boom and bust is that the industry needs more, stable lithium supply to ensure a healthy market.

SQM, the second-largest lithium miner, says it’s still plowing ahead with planned expansions and operating at full capacity. In fact, Chile’s finance minister said recently that the country is aiming to double production, arguing that the risk of renewed shortages and price spikes is more dangerous for the industry than a prolonged oversupply.

Lithium’s bright long-term demand outlook and its strategic importance to carmakers and governments could also underpin ongoing funding of new projects even in a depressed price environment.

And while worries about the appeal of EVs have risen recently in some Western markets, Chinese car manufacturers and battery-makers are pressing on with huge expansions. Against that backdrop, Zijin Mining Group Co., said last month it’s planning acquisitions of “ultra-large mines or mining companies with global influence” to boost business in lithium and other metals.

For car- and battery-makers, the past three years have provided a lesson in how efficiently the mining industry is able to bring on new supply when it’s needed, reducing the imperative for panic buying and rushed dealmaking during times of tightness.

Current low prices have led to some mine closures, but there’s a newfound recognition across the industry that supply could be brought back into the market almost as quickly as it’s being removed.

“It’s still a market where supply is set to outpace demand growth,” said Morgan Stanley analyst Amy Gower. “We are starting to see a supply reaction but we need to stay in this pain zone for a little bit longer.”

(By Mark Burton, Annie Lee, James Attwood and Yvonne Yue Li)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments