Lithium at two-year low hobbles US bid to loosen China’s grip on market

The lowest lithium prices in over two years are hampering a handful of miners that want to challenge China’s dominance in the market.

China controls most of the processing that makes the mineral usable in rechargeable batteries, leaving American vehicle makers vulnerable to supply disruptions if trade tensions escalate. With automakers from Tesla Inc. to General Motors Co. aiming to manufacture more electric cars at home, small companies are seeking to build the first U.S. lithium mines in decades as a step toward forming a local supply chain.

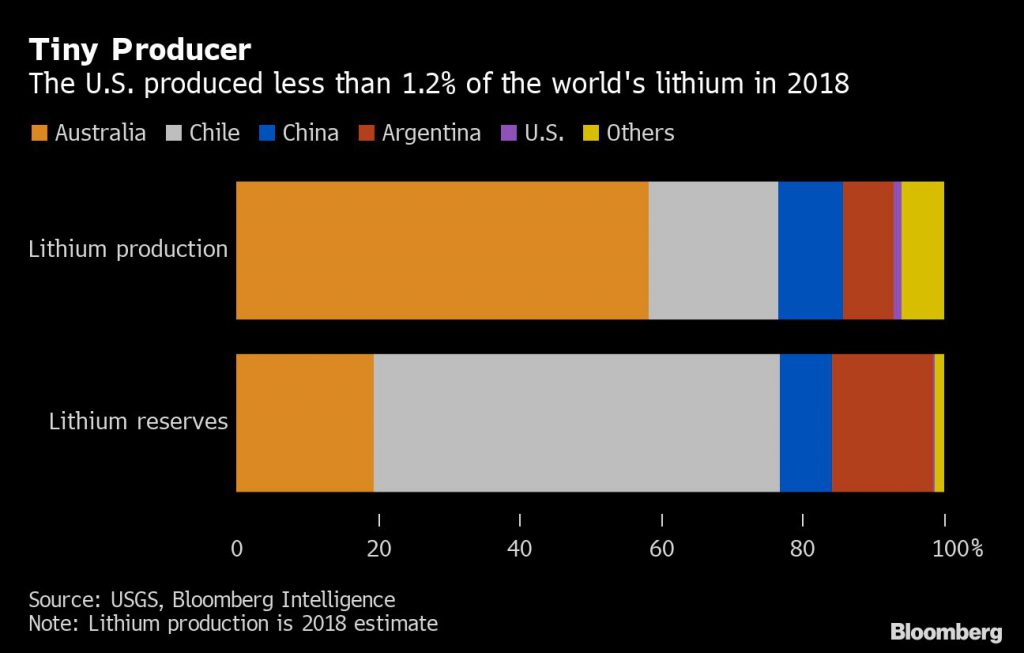

However, financing mines is proving a challenge after a rush of Australian supply dragged down prices by a third from a record in mid-2018. Companies also face stricter environmental rules and regulatory hurdles in the U.S., which currently accounts for just 1.2% of global lithium production.

“It’s a difficult environment,” said Keith Phillips, chief executive officer at Piedmont Lithium Ltd., which is going through the permitting process to build a lithium operation in North Carolina. “Those looking to raise capital now might be able to do it, but the terms won’t be as good as they might have been at some other point.”

While prices are now weak, lithium use will significantly jump by 2023 and the market could move into deficit around that year, according to Benchmark Mineral Intelligence estimates. All the supply from the globe’s major lithium miners Albemarle Corp., Soc. Quimica y Minera de Chile SA, Tianqi Lithium Corp. and Ganfeng Lithium Co. — companies that mine mainly in Australia, Chile and China — probably won’t be enough to meet demand.

“You can’t just depend on the majors, there’s a need for diversification,” said Andrew Miller, a lithium analyst at Benchmark Mineral Intelligence. “When battery production capacity starts being set up outside of China in the next three years or so, the urgency to have that supply outside of China becomes even more critical.”

Lithium mines take from three to five years to be built, which means that investment needs to flow into new projects within the next 12 to 18 months to fill the potential supply gap in the future, according to Miller. BloombergNEF estimates U.S. lithium cell manufacturing capacity will more than triple through 2025 as more battery manufacturing facilities are built near demand centers.

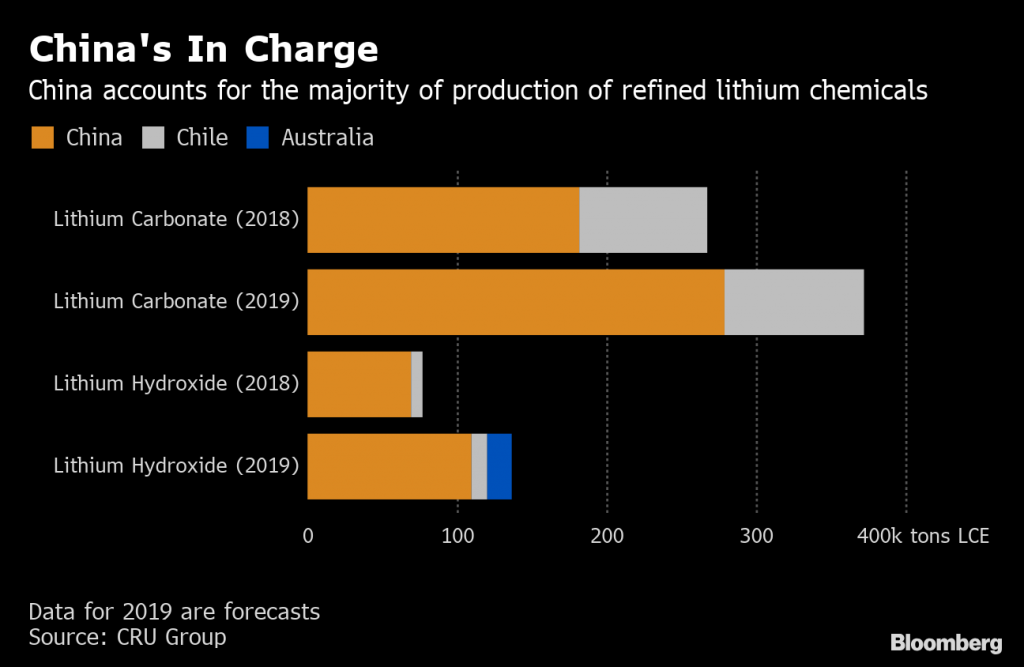

The U.S. accounts for just 186,300 metric tons of global lithium reserves, compared with 42.6 million tons in Chile and Australia’s 14.4 million. Most of the raw mineral is shipped to China where it’s converted into cathode that’s used in the manufacture of batteries that power everything from smartphones to EVs.

The companies are looking to make up for higher U.S. mining costs with proximity to manufacturing plants and by using new technology. Where electric car components come from will become increasingly relevant not only in terms of strategy, but also from an environmental perspective, the companies say.

Electric demand

“Automakers are going all in on electric,” said Robert Mintak, CEO at Standard Lithium Ltd. “They will need a supply chain and there’s going to be added value for any U.S. lithium resource that is able to produce high-quality, battery-grade material.”

Canada’s Standard Lithium is testing new technology to produce high-quality material and hopes to make a decision to start commercial production by mid-2020. Perth, Western Australia-based Piedmont Lithium says it could start producing lithium chemicals in the U.S. in 2023.

Standard Lithium’s technology, which hasn’t been tested commercially before, allows for a 90% lithium recovery rate, according to Mintak. Companies operating in South America produce the metal at the world’s lowest cost by pumping briny mud from underneath Andean salt flats and letting it evaporate. But they have much lower recovery rates and use as much water as a standard copper operation, according to BlooombergNEF.

“There’s going to be a judgment day on where the materials for renewable energy storage and electric vehicles are coming from,” Mintak said. “It’s not only that you will need to produce high-purity material, but you will have to be able to address the environmental issues that everybody points fingers at.”

Standard Lithium’s shares in Canada were little changed Tuesday, after falling 5.1% in the previous session. Piedmont Lithium’s stock rose 1.1%.

Approval processes

Still, hurdles abound. Approval processes to sell lithium to battery-making companies typically last 18 months and miners need to prove they can supply a constant amount of high-quality product. In the past, that’s been a challenge even for established producers.

“Some of these projects could become lithium mines, but it’s not a given,” said Chris Berry, a consultant and founder of battery metals research firm House Mountain Partners. “It remains an open question whether they can raise $500 million or $1 billion for a strategic commodity when they have never done it in this country.”

Top lithium miner Albemarle, which produces about a quarter of the world’s output, together with its biggest rivals SQM, Tianqi and Ganfeng are the only producers with the size, volumes and cost position to serve large customers, according to Albemarle Chief Executive Officer Luke Kissam. The industry will experience a shakeout over the next decade, he said in an interview at the company’s headquarters in Charlotte, North Carolina.

“It’s going to be tough for newcomers,” he said. “A lot of these new entrants are going to get started in hopes that one of the big ones buy them out.”

(By Laura Millan Lombrana, with assistance from Joe Deaux and Justina Vasquez)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments