Iron ore’s unexpected rally shows pockets of China strength

The one commodity that should be getting hammered by China’s worsening property crisis is actually doing rather well.

Iron ore climbed to its highest in a month last week after a rally that has defied deepening gloom over China’s debt-laden economy. Prices have largely kept above the key $100-a-ton threshold this year despite waves of worrying news from the real estate sector, which in more normal years makes up about 40% of demand.

The absence of a price crash or devastating slump in steel demand illustrates how pockets of China’s economy are holding up despite the negative headlines. There are still plenty of risks ahead for iron ore, not least the prospect of a prolonged slump in the property sector. But relatively robust prices offer a counterpoint to the prevailing bearish mood across Chinese markets.

“Iron ore is still very resilient for an environment like this, and I think Chinese demand is playing a role in that,” said Hao Hong, chief economist at Grow Investment Group. It shows parts of the economy, outside the property sector, are relatively healthy, he said.

While the Shanghai Composite Index of stocks fell to its lowest this year last week — prompting government steps to steady the market — iron ore futures rose to as high as $114 a ton. In the last major slump of 2015-16, prices sank below $40 a ton, and China’s steel surplus flooded onto the world market, fueling trade tensions.

This doesn’t mean China’s economy will escape a marked slowdown in growth, or that iron ore prices will continue at these levels. Property construction is falling, especially in less-developed inland cities. And President Xi Jinping’s government is holding off on the large-scale stimulus, including infrastructure spending, that has typically lifted steel consumption during previous episodes of economic stress.

BHP Group, the world’s second-biggest iron ore producer, said it’s seeing “solid demand from infrastructure, power machinery, autos and shipping, offsetting weakness in new housing starts and construction machinery.” Consultancy Kallanish Commodities Ltd. adds “white goods” to that list, a category that includes products like fridges and washing machines.

Railway boom

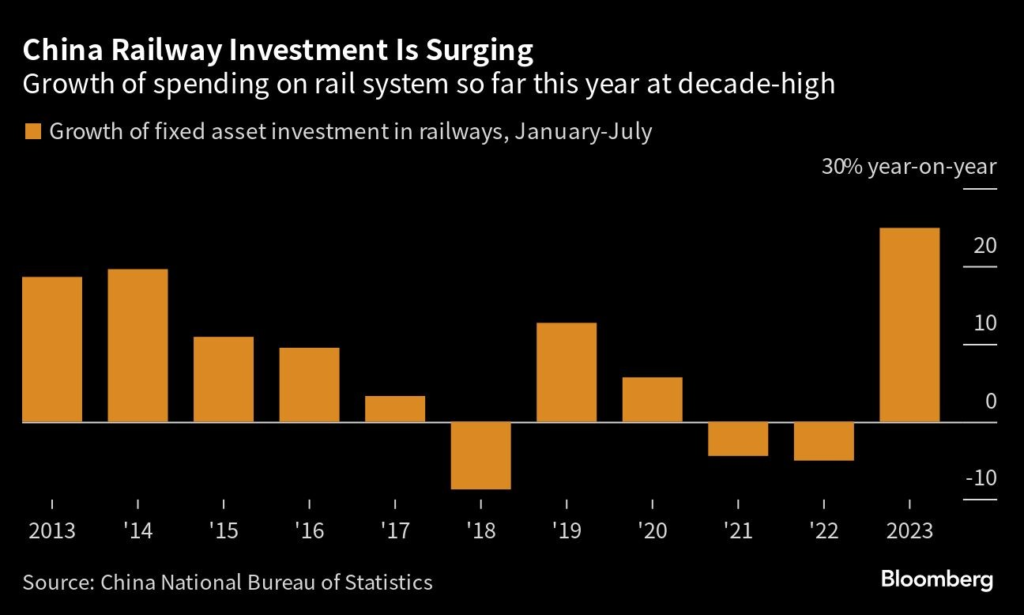

While many local governments are slowing spending due to financial strains, central government investment on infrastructure like railways is growing more rapidly.

Spending growth on railways is running at 25% year-on-year in the first seven months of 2023. Machinery manufacturing has risen 15% and auto output has grown 12%. There’s also a boom in the new energy sector, which isn’t negligible for steel demand. Property investment, meanwhile, contracted 7.1% in the first seven months of the year.

Steel industry forecasts from researcher CRU Group illustrate the divergence between construction and the rest, with demand for so-called “long products” used in building set to fall 1.7% this year. Flat products, the other major category, will see a 3% increase, it said.

Research firm Mysteel said demand for heavy plate used in ships, bridges and wind turbines rose 8.1% in the first five months of the year. The product accounts for about 10% of Chinese steel demand. Other categories covering construction, machinery, appliances and cars were flat or slightly lower.

And even in the property sector, there are some small signs of optimism even as debt risks continue to swirl around the sector, with some state-backed developers reporting a recovery in sales volumes.

The overall result is a market that’s “lying flat,” according to Jiang Hang, head of trading and research at Yonggang Resources Co. — a reference to the much-discussed social phenomenon where citizens do the minimum to get by. Mills aren’t building up much inventory, but they’re still buying when necessary to meet immediate demand, he said.

Production curbs

The resilience in steel demand and iron ore prices is also being driven by some industry-specific factors.

Steel exports have soaked up some extra material, and shipments from China are on track to reach their highest since 2016, although volumes are still well short of the quantities that irked trade partners at that time.

Iron ore has been helped by cuts at electric arc furnaces that use scrap — an alternative production method for steel. That’s helped keep output derived from iron ore relatively robust. Average daily production of molten iron from blast furnaces has reached its highest since 2020, according to Mysteel.

Steelmakers and traders are also buying up iron ore in anticipation of the seasonal lift to construction activity that occurs after the summer. And mills could be raising their output now to guard against the possibility of government-ordered production curbs later in the year.

“Iron ore prices have deviated a bit from economic fundamentals, largely due to a lack of self-discipline at mills,” said Xu Xiangchun, an analyst with Mysteel. “China’s economy isn’t that promising.”

For the rest of this year, whether China avoids more turmoil in the property sector is likely to be the decisive factor for prices. The lack of confidence in the private sector, and the dangers of local-government debt stress spreading to other parts of the economy, are also strong headwinds.

“China can’t reignite the fire under real estate and it looks like it doesn’t want to,” said Tomas Gutierrez, an analyst at Kallanish Commodities. “It does look like there’s a pretty solid floor for iron ore at $100 in the short term, but longer-term the outlook is weaker.”

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments