Iron ore’s $100 price floor at risk of collapse from jump in supply

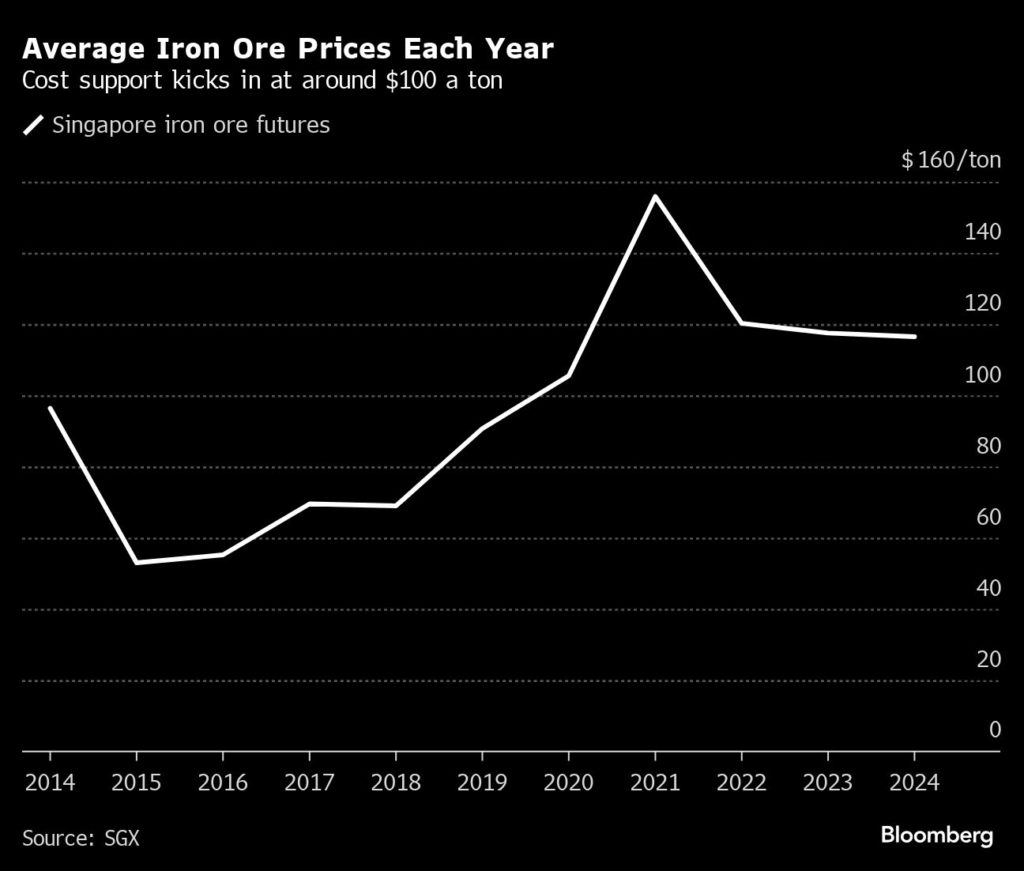

Iron ore prices are likely to stay in three digits for the rest of 2024, insulated to a large degree from China’s faltering economy by cost support that kicks in at around $100 a ton.

But that could change from next year as a wave of cheap supply starts to build in West Africa, lowering the industry’s average costs and forcing prices to better reflect the long-term decline of China’s steel industry, the biggest consumer of iron ore.

The world’s largest untapped ore reserve in Guinea’s Simandou is intensifying preparations for production. The project could deliver 5 million tons starting in 2025 before ramping up steadily to 90 million tons a year in 2028, according to Macquarie Group Ltd.

Nameplate capacity is 120 million tons, a level that could be reached in five to seven years, said Liz Gao, a senior analyst at consultancy CRU Group. By that time, “the market will rebalance, with high-cost producers leaving the market to make room for these new volumes from Simandou,” she said.

Digging up iron ore, the key ingredient to make steel, has been a fantastic business for some of the world’s biggest miners. China’s rapid growth, and a laserlike focus on lowering costs, has delivered bumper profits year-in, year-out for producers like Rio Tinto Plc and BHP Group Ltd. But a combination of fading demand in China and swelling supply now threatens to upset the outlook for their main profit driver.

Benchmark iron ore futures have slid 23% this year to about $109 a ton as Chinese consumption has slowed. Twice in recent months, the Singapore contract has breached $100 only to swiftly rebound due to the threat that higher-cost miners around the world would be forced to curtail production if prices stayed below that level. But that cost support is likely to become increasingly fragile.

Chinese conditions bode ill for iron ore’s long-term demand prospects. The economy isn’t growing as fast as it used to, and is becoming less steel intensive as it matures. The property sector, the biggest source of demand, is in the grip of a protracted crisis. The government is trying to cap steel production at or below the previous year’s level to reduce overcapacity and cut emissions. The industry is also adding more electric arc furnaces, which recycle existing steel and are less carbon intensive.

Sizable chunk

Simandou will deliver a sizable chunk of the 1.6 billion tons of iron ore sold each year on the global market. Australian miners currently account for well over half that volume. Rio Tinto, the world’s biggest supplier, BHP and Fortescue Ltd. also dominate the lower end of the cost curve, churning out ore at between $18 and $24 a ton, figures that don’t include processing and transportation. Brazil’s Vale SA, the world’s second-largest iron ore miner, produces at $21 a ton.

That has meant fat profits for the majors, despite the fall in prices. But costs at Simandou, which is divided into northern and southern blocks, would be comparable to the cheapest supply currently available. By the end of the decade, the southern part of the project is likely to be producing at $20 a ton, and the north at $35 a ton, according to Commonwealth Bank of Australia analyst Vivek Dhar, who pegs the long-term iron ore price at just $68 a ton.

And there are other supply issues to contend with. The Guinean project, which counts Chinese investors as well as Rio among its developers, is part of China’s efforts to raise its high-grade iron ore self-sufficiency to 45% by 2025. To make the jump from 17% in 2023, the country must at least double its supply by next year, according to Bloomberg Intelligence, which is likely to heap more pressure on prices.

Port inventories

And Simandou isn’t the only large mine scaling up operations. A Mineral Resources Ltd. project in Onslow, Australia, will reach capacity of 35 million tons a year by June 2025. It delivered its first iron ore shipment to China Baowu Steel Group ahead of schedule in May.

Even without Simandou’s ore coming to market, some higher cost mines are being shut. Mineral Resources has said it will close its Yilgarn project in Western Australia from the start of next year, citing costs.

Chinese buyers are already well supplied this year even as the buildup of overseas production gains momentum. Port inventories have expanded to their highest in over two years.

As the slowing economy continues to drag on prices, investors are focused on whether Beijing will offer more policy support to revive the housing market, said Soni Kumari, commodity strategist at ANZ Group Holdings Ltd. But even if next week’s Third Plenum does deliver another dose of stimulus, how commodities-intensive it will be remains to be seen.

As it stands, the situation is reminiscent of market dynamics a decade ago, when “terrible” domestic demand in China and abundant supply dragged prices below $40 a ton, said Atilla Widnell, managing director at Navigate Commodities Pte in Singapore.

“Hopefully, history doesn’t repeat itself,” he said.

(By Audrey Wan)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments