Iron ore price falls over 15% in 2024 on faltering China demand, high portside stocks

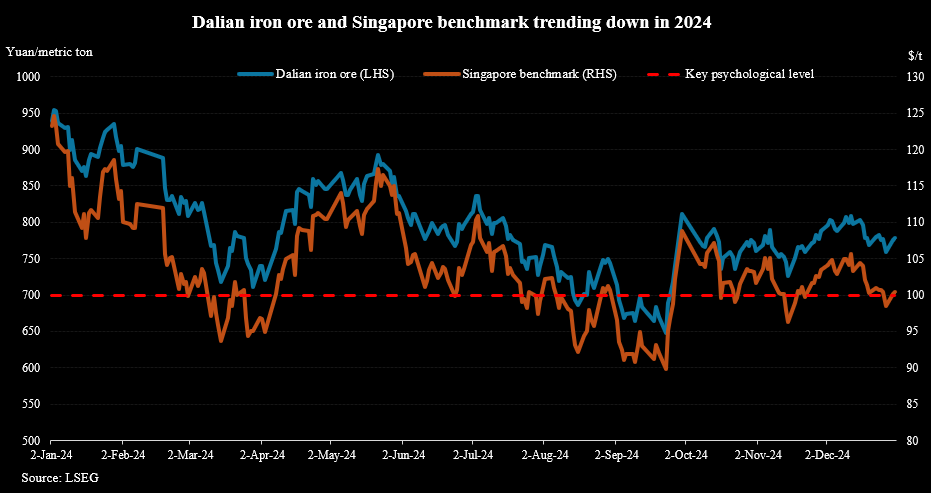

Iron ore futures ended 2024 with a drastic decline of more than 15% as faltering demand, thin steel margins and high portside stocks in top consumer China dragged prices of the key steelmaking ingredient lower.

Prices rose on the day as sentiment was boosted by Chinese President Xi Jinping’s remark that this year’s gross domestic product (GDP) is expected to grow by around 5%, although mounting caution following China’s slowing factory activity expansion in December pressured prices earlier the session.

The World Bank sees China’s gross domestic product growth at 4.9% this year, up from its June forecast of 4.8%.

The most-traded May iron ore contract on China’s Dalian Commodity Exchange (DCE) ended daytime trade 1.17% higher at 779 yuan ($106.73) a metric ton.

The benchmark February iron ore on the Singapore Exchange was 0.23% higher at $100.4 a ton as of 0703 GMT after falling to $99.6 earlier in the session.

Year-to-date, the Dalian contract has fallen 16%, while the Singapore benchmark has slid 18.5% as demand wilted with China’s crude steel output falling by 2.7% year-on-year in the first 11 months of this year.

A raft of stimulus measures unveiled by Beijing since late September to spur its sputtering economy helped the ferrous market recoup some losses caused by protracted property sector woes hitting steel consumption despite robust steel exports.

The new year should see more oversupply in sea-borne iron ore markets, said Tomas Gutierrez, head of data at consultancy Kallanish Commodities.

“There are higher Australian exports coming and some important projects ramping up… So prices will be under pressure.”

Other steelmaking ingredients on the DCE advanced. Coking coal and coke gained 0.91% and 1.43%, respectively, although they posted annual falls of 44% and 32.5%.

Steel benchmarks on the Shanghai Futures Exchange were mixed, but ended the year with falls between 11% and 25%.

Rebar added 0.39%, wire rod rose 0.08% while hot-rolled coil eased 0.09% and stainless steel dipped 0.35%.

($1 = 7.2991 Chinese yuan)

(By Amy Lv and Colleen Howe; Editing by Mrigank Dhaniwala and Sumana Nandy)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments