Investors glimpse opportunity in Europe’s unloved mining shares

Investors are finally seeing potential in European mining shares, as China’s step-by-step economic stimulus is steadily laying the foundations for a recovery of the unloved sector.

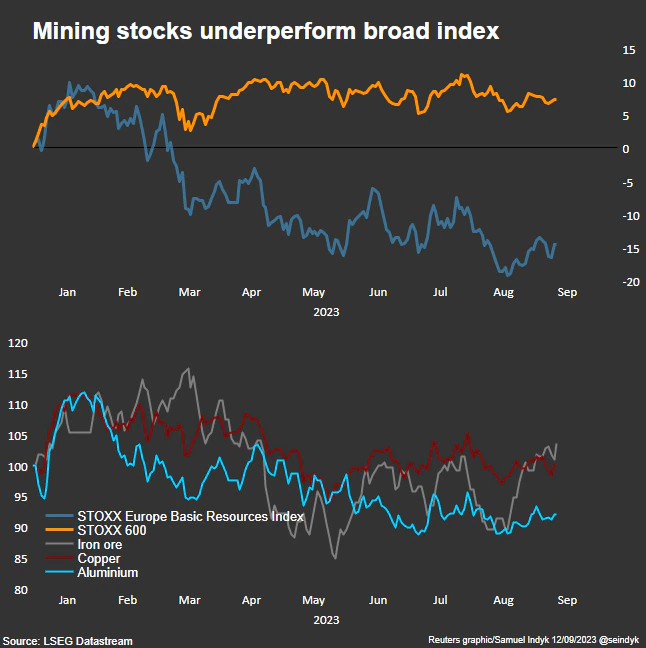

The STOXX Europe 600 mining index has fallen 15% this year, making it the worst performing sector in the region by some margin, with second-placed real estate down 4.5% and the top-performing retail index up 27%.

The metals and mining sector is typically used as a proxy for equity investors in Europe to gain exposure to China, given it is the world’s largest commodities consumer, and it has sunk along with China’s growth expectations.

The world’s second-largest economy has been struggling after a brief post-Covid surge, dragged down by huge debt due to decades of infrastructure investment and a property downturn. Analysts forecast the economy will grow by just 5% this year, the slowest rate, outside of Covid years, since 1990.

But Beijing in recent weeks has taken targeted steps towards supporting key pockets of its economy, lifting the mining sector off its 31-month lows. In the last month, the mining index has risen nearly 10% compared with a gain of just 2.5% for the wider STOXX 600.

“China is building a wall of stimulus, but they’re doing it brick by brick,” said Nathan Sweeney, chief investment officer of multi-asset at Marlborough Investment Management.

“At some point people will realize they have built the wall, but it just hasn’t come all at once.”

In the last three months, China has relaxed rules around home purchases and borrowing, and cut key interest rates. There are also new tax relief measures for small businesses and private investment in some infrastructure sectors, for example.

Sweeney says this wide range of measures could be a catalyst for an upturn in the metals and mining sector.

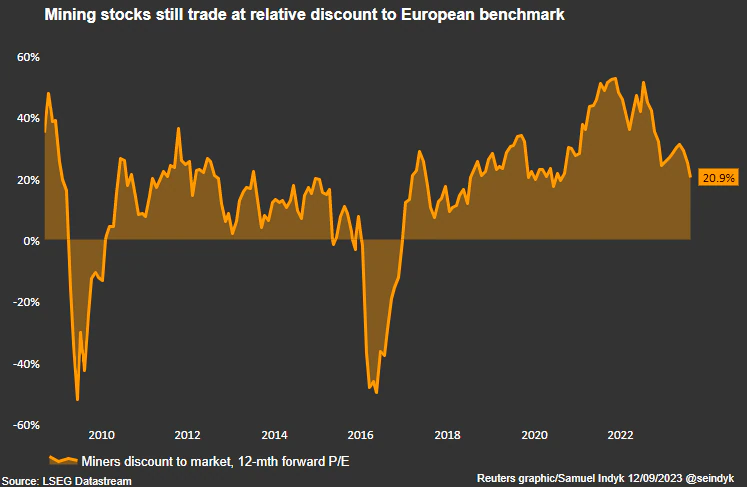

The STOXX basic resources index trades at over a 20% discount to the STOXX 600. Miners trade at a 12-month forward price-to-earnings ratio of 9.8, compared to 12.3 for the market, according to LSEG Datastream.

Shares in some of the industry heavyweights have taken a battering this year. Glencore and Boliden have dropped by more than 20%, while Anglo American has lost 30%. The pan-European STOXX 600 benchmark meanwhile, is up 7.5%.

Copper and iron ore have fared better. Three-month copper on the London Metal Exchange is flat for the year at $8,380 a tonne, while front-month Singapore iron ore futures are up nearly 9%.

Considering China’s heft in the commodities world – Morningstar estimates it accounts for over 50% of refined copper demand and about 70% of the seaborne iron ore trade – some of that resilience should eventually seep into mining stocks, analysts said.

“Obviously, the 800-pound gorilla from a primary metal demand perspective is China,” Peter Mallin-Jones, mining analyst at UK investment bank Peel Hunt, said.

“I’m quite positive because I can see, certainly for the base metals, fairly significant demand drivers into markets that feel relatively tight,” he said.

Sector is key to going electric

Specifically, Mallin-Jones points to the global energy transition, as economies begin to decarbonize, which could bring a huge increase in demand from fast-growing nations such as India, Indonesia, Malaysia and Nigeria.

Copper is the backbone of the electric and electronic industries and is essential in upgrading power grids, building solar farms, wind turbines and electric vehicles.

The United States and China are expected to add record amounts of solar production capacity this year, with a projected extra 32 gigawatts and between 95 and 120 gigawatts, respectively.

“That’s an enormous number and is a huge support for demand for copper and to an extent aluminium,” UBS metals and mining analyst Daniel Major said.

Major does not believe stimulus in China will lead to the kind of explosion in commodities demand seen after 2008, when the country bounced back from the global financial crisis.

We see measures limiting downside and creating stabilisation in aggregate commodities demand but not driving a very strong rebound,” he said, adding that he expects the demand outlook for iron ore to deteriorate alongside a slower global economy while the likes of copper and aluminium will likely benefit from the renewables boom.

Accordingly, UBS has ‘sell’ ratings on diversified miners Rio Tinto and BHP Group and Major prefers companies with more direct exposure to copper.

Antofagasta, Europe’s largest pure-play copper miner by market cap, Poland’s KGHM and copper recycler Aurubis are all down less than 12% this year, and have all relatively outperformed diversified miners Glencore, Rio Tinto and Anglo American, which have fallen between 14%-35%.

“The reality is the sector now looks attractive and a lot of bad news is in the price,” Marlborough Investment Management’s Sweeney said.

(By Samuel Indyk; Editing by Amanda Cooper and Elaine Hardcastle)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments