In race to net zero, being small or diverse foils metal makers

A look at the underachievers in a new decarbonization ranking of metal producers shows size, location and metal type all matter, while diversification has its downside.

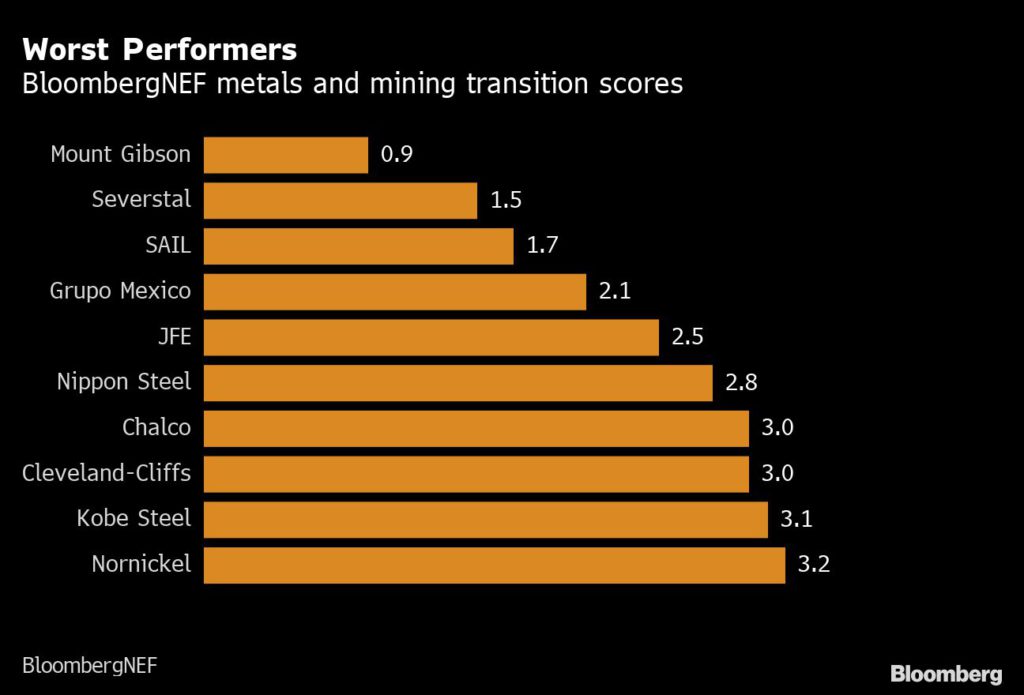

The worst performers among 53 major metal companies ranked for risks and readiness in a net-zero emissions scenario were an Australian iron ore miner and steelmakers from Russia and India, according to a BloombergNEF rating. Top scorers — such as Norsk Hydro ASA and ArcelorMittal SA — were large companies focused on one product and one segment.

As environmental, social and governance investments hurtle toward $50 trillion, grading enterprises on their transition efforts is becoming as important as conventional earnings metrics. That’s especially so in the dirty business of making metals, which creates about a quarter of the reported emissions of the world’s 12,000 largest companies. Companies’ exposure to fast-changing demand trends and efforts to clean up their operations and supply chains will play an ever more important role in determining trading valuations.

Related Article: Miners look to carbon capture to move beyond net zero

At the bottom of BloombergNEF’s first transition score for the metals industry is Mount Gibson Iron Ltd. While the Western Australian company produces high-grade ore that helps reduce steel-making emissions, its volume is a tiny fraction of global heavyweights like Rio Tinto Group. Smaller firms faired worse because they are less able to fund decarbonization activities and hold less sway with customers and suppliers to do the same.

But size isn’t everything. Severstal PAO, a top Russian steelmaker with a market value of almost $20 billion, came in second to last, according to BNEF. Among other factors, Severstal paid the price of diversification, with the company not only producing a slew of steel products but also a decent amount of iron ore and coal. Vertical integration has plenty of benefits, but can undermine a company’s ability to focus on particular technologies and products for decarbonization.

Location was another factor weighing on companies. Steel Authority of India Ltd., or SAIL, came in third to last, scoring zero in the category on government policy, BNEF reported. Most of the top companies in the ranking are based in Europe, where policy encourages or requires moves to significantly reduce emissions.

It’s also no coincidence that the three last-placed three companies are from the same broad sector. Steel is one of the dirtiest materials to produce, with the industry blamed for about 7% of global carbon emissions. Ferrous alloys also fall outside the group of metals such as copper and cobalt considered key for electrifying economies.

Still, Freeport-McMoRan Inc.’s status as the world’s biggest publicly traded copper producer, wasn’t enough to save it from the bottom half of BNEF’s rankings. The Phoenix-based company scored poorly in customer net-zero pressure and registered a lower electrification rate than larger state-owned rival, Codelco, for example. Codelco also did more to manage portfolio demand risk by selling a stake in an oil and gas project, while Freeport exited a cobalt cathode project, Bloomberg’s energy data and analysis firm said.

Mount Gibson Iron said in an emailed response that its high grades and direct-shipping method give it a cleaner profile than some other producers. In addition, a mine life of just five years means its future remains open, while its small size and strong finances mean it will be a “nimble follower” of technologies that become available, the company said.

Severstal responded to the low BNEF ranking by reiterating its commitment to helping the steel industry cut emissions. In July, the company set a goal of reducing the carbon intensity of its emissions by 10% by the end of 2030, placing it among the top 15 steelmakers, it said.

Neither SNAIL nor Freeport immediately responded to requests for comment.

(By James Attwood, with assistance from Yvonne Yue Li)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments