Hong Kong ousts Dubai as biggest hub for Russian gold trade

Shut out of London following the invasion of Ukraine, Russian gold trading switched to Dubai. Now it’s shifting again, to the bullion hub of Hong Kong.

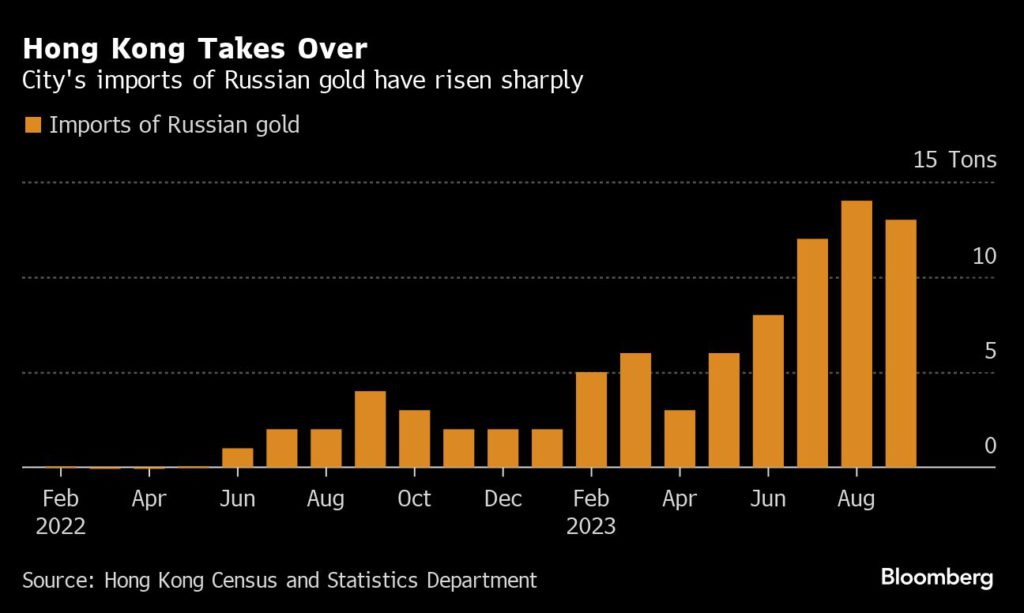

The city has long been a key conduit for bullion entering the Chinese mainland — the world’s biggest consumer market — but since April, Russian shipments surged. Hong Kong imported 68 tons of Russian gold this year, four times as much as the whole of 2022.

The shift to Hong Kong was driven by US sanctions on Russia’s top gold miners, as well as a crackdown by the United Arab Emirates on illicit activities in its bullion market, according to people familiar with the matter. The move east underlines the challenge faced by the West in curbing resource flows that fund the Kremlin’s war machine.

Before the invasion of Ukraine, almost all the gold exported from Russia — the world’s second-largest miner — was shipped to vaults in London, the center of the global bullion trade. But the Kremlin’s attack made Russian gold taboo in the mainstream industry, even before a formal ban blocked imports to the Group of Seven Nations and European Union.

When Russian gold was locked out of London, Dubai — a key transit hub for bullion being shipped to Middle East and Asian markets — was the initial beneficiary. The UAE maintained its neutral stance this year, refusing to take formal measures against Russian gold despite lobbying by the US and UK, people familiar with the discussions said.

Russia shipped 96.4 tons of bullion to the UAE in 2022, making it the country’s largest supplier. That was more than five times the volume exported through Hong Kong.

While there’s still no UAE ban on importing Russian gold, volumes have fallen significantly. That’s partly due to regulatory clean-up, after the Middle East nation was added to a watch-list by the Financial Action Task Force, a global money laundering watchdog.

Bank transfers in the UAE have been subjected to increased oversight, while cash payments are monitored through a mandatory government database, which has made paying Russian exporters more difficult, people familiar with the matter said. US sanctions in May on Russia’s biggest gold miners — Polyus JSC and the local unit of Polymetal International Plc — also had a chilling effect as UAE traders and banks are more reluctant to deal with designated entities, the people said.

Some Dubai-based gold buyers began rerouting shipments to Hong Kong, according to preliminary data from trade-tracking firm ImportGenius, based on Russian customs figures for the six months through August.

Other UAE firms pulled back altogether. State-owned logistics firm Transguard, which is part of airline Emirates Group, said in May it had stopped transporting Russian gold.

“The UAE operates with clear and robust processes against illicit goods, money laundering and sanctioned entities, and implements the highest international governance standards across the gold trade,” the government-chaired Gold Bullion Committee wrote in a statement to Bloomberg. The UAE will continue to trade “in compliance with all current international norms as set down by the United Nations.”

Last Wednesday, the UK issued a fresh round of sanctions on companies linked to the Russian gold trade, including Dubai-based Paloma Precious DMCC, which it said had imported $300 million from the country. The firm was formerly the shareholder of Emirates Gold DMCC, the refinery suspended from the UAE’s accredited list due to concerns about its ownership.

At the same time, China has made it clear that it wants to boost trade with Russia, underscoring the close ties between the nations’ leaders Xi Jinping and Vladimir Putin since the invasion of Ukraine. Beijing has provided diplomatic and economic support to Moscow that has helped blunt the effects of Western sanctions, while China is now the largest importer of fossil fuels from Russia.

VPower Finance Security (Hong Kong) Ltd., which moves cash and precious metals for some of China’s biggest financial institutions, is a key player in handling newly imported gold from Russia, data from ImportGenius shows. VPower did not respond to an email seeking comment.

The shift to Hong Kong was also helped by a surge in Chinese gold prices above international ones in September. That drew bullion into the country, creating profitable arbitrage opportunities for banks with import licenses.

(By Malaika Kanaaneh Tapper and Eddie Spence)

More News

Contract worker dies at Rio Tinto mine in Guinea

Last August, a contract worker died in an incident at the same mine.

February 15, 2026 | 09:20 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments