Hong Kong is the real loser from new China copper contract

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

China’s long-awaited international copper contract made its debut last week.

The timing will be a bitter blow for Charles Li, whose tenure as chief executive of Hong Kong Exchanges and Clearing (HKEx) ends in December.

Li upended the commodities world by snapping up the venerable old London Metal Exchange (LME) in 2012 with a vision of Hong Kong connecting China’s huge mainland metals market with the rest of the world.

However, what worked for HKEx in the stocks and bonds sectors never took flight in metals with the obvious partner, the Shanghai Futures Exchange (ShFE), rejecting all advances.

The ShFE copper contract is characterised by a low ratio of open interest to trading activity as locals avoid overnight margining

After refusing to let the LME and its owner in, ShFE is now stepping out with its new international copper contract.

Suggestions that this marks the beginning of the end of the LME as a global pricing benchmark are probably a little premature.

More likely is that Shanghai will, over time, become a pricing point for the Asia-Pacific area, both reflecting and reinforcing the underlying deglobalisation of metal supply chains.

The battle to get in

At the heart of the LME’s long-running attempt to muscle into the Chinese market was the opening of exchange warehouses in Shanghai’s bonded zone, where international and domestic markets physically meet.

The previous LME leadership had given up on the possibility after a ruling from China’s Securities Regulatory Commission (CSRC) explicitly prohibiting any overseas exchange from setting up warehouses.

With ShFE effectively ring-fenced, the LME reacted by strengthening its Asian presence by opening warehouses in Taiwan and setting up a representative office in Singapore.

Li bet he could force open the Chinese locks and it’s possible he came close, with Reuters reporting in July 2013 that the all-powerful National Development and Reform Commission was reviewing the case.

But it evidently decided against and by October of that year LME Chief Executive Barry Jones conceded that: “I think we are dreaming if we think we will have warehousing there any time soon.”

With ShFE seemingly spurning all offers of partnership on new products, Li’s last throw of the dice was setting up a physical market in Qianhai. It has failed to gain any real traction and has now been blown away by the new copper contract, based on the copper sitting in Shanghai’s bonded zone.

Initial physical delivery storage capacity is set at 175,000 tonnes, compared with total bonded copper stocks of around 370,000 tonnes.

Coming out

The new contract, traded on ShFE subsidiary the International Energy Exchange, is Shanghai’s fourth yuan-denominated international contract offering after crude oil, rubber and low-sulfur fuel.

They are international in the sense that, unlike domestic exchanges, the contracts exclude China’s 13% value-added tax and are open to overseas players to trade without setting up a mainland subsidiary.

All are aimed at increasing the internationalisation of the yuan and boosting Chinese pricing power.

Copper is the “biggie”.

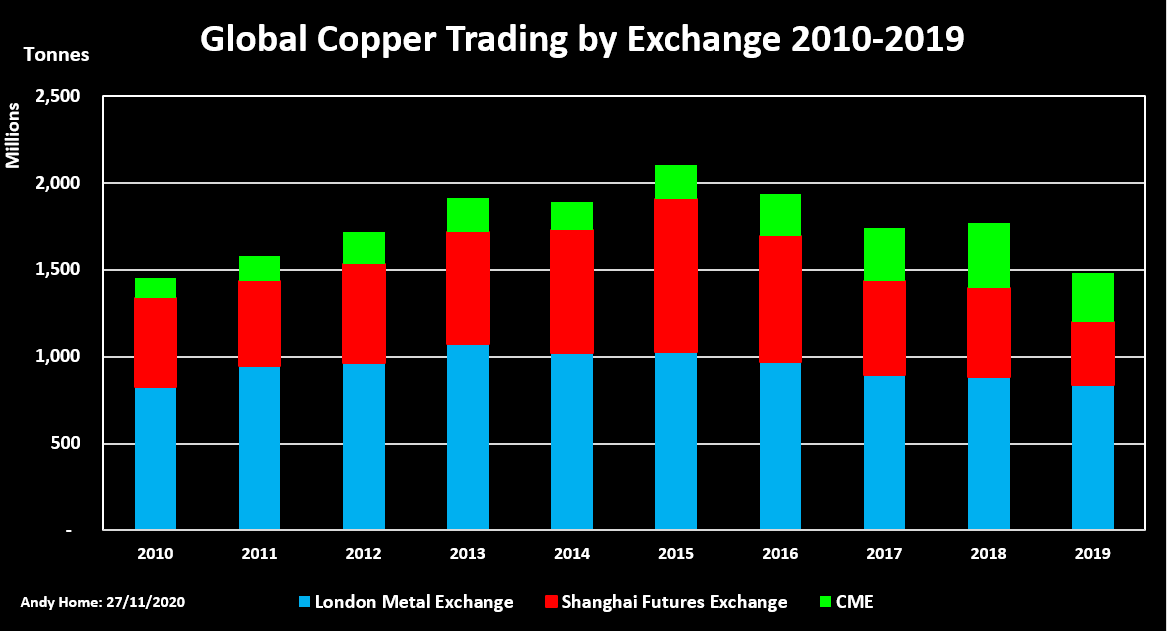

China is the world’s largest physical buyer of the metal by some margin and already exerts a huge influence on pricing via existing arbitrage between the LME and the ShFE’s domestic contract.

The LME’s own pricing supremacy dates back to the 19th century, when Great Britain was the world’s largest importer of copper.

China is the world’s new industrial powerhouse, which is why the LME spent so many years trying to open up warehouses there.

It and HKEx will now have to watch from the sidelines as Shanghai, not Hong Kong, becomes the copper connector between mainland and international markets.

Building liquidity

The new contract has made a respectable start, notching up over 60,000 lots of trading since launch on Nov. 19.

That’s a fraction of the two million lots traded on the domestic Shanghai copper contract in the last week but those super-charged volumes reflect high levels of retail investor participation in China’s commodities exchanges.

The ShFE copper contract is characterised by a low ratio of open interest to trading activity as locals avoid overnight margining, typically under 10% on a month-end basis.

The ratio on the new contract has exceeded 50% over the last four days, attesting to the presence of heavier-weight players.

There is little doubt that it will continue building liquidity, albeit with China’s capital controls acting as a significant brake.

Regional not global

It is also almost certain that in time the contract will emerge as a natural pricing reference point for copper flowing to China.

But the LME can probably breathe easily for a while yet.

Fang Xinghai, vice-chairman of the CSRC, the same body that locked the LME and HKEx out, told the China Daily he expected the contract “to become one of the pricing benchmarks in the Asia-Pacific region”. Emphasis on the word “one” there.

The scope of the contract’s pricing power will be determined by the geographical scope of China’s physical supply chains, and these are shifting.

Rare earths, magnets and telecoms make the deglobalisation headlines as first the United States and now the European Union stress the need for greater self-sufficiency and less dependence on China for critical components.

But trade tensions have been playing out in the copper market too.

The United States used to be the biggest supplier of copper scrap to China. However, tighter purity rules and a brief tit-for-tat tariff exchange last year have changed this trade flow.

The largest destination for U.S. copper scrap is now Malaysia, where the material is upgraded to meet Chinese purity thresholds. Malaysia is now China’s top supplier, the United States falling to a distant third.

This reformulation of scrap flows redirects the potential scope of a Shanghai price reference point from international to Asian markets.

A similar reorientation may be pending in the concentrates market, where Australian producers are facing a boycott from Chinese buyers as Beijing expresses its displeasure over a range of political and economic tensions.

The world has passed peak globalisation and the restructuring of global supply lines into more regional ones is playing out across the metallic spectrum.

A deglobalised world may not need a global copper reference point but rather three regional ones, currently offered in theory by the LME, CME and now Shanghai bonded.

This does not need to be a zero-sum game. History suggests that more pricing venues means more trade for everyone.

That, however, still leaves HKEx out in the cold and it is Hong Kong, rather than London, that may be the real loser in this great copper game.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments