Hedge funds’ bullish copper bets run into China’s slowdown

As copper surged to record highs last month, several senior Chinese traders started trying to contact western hedge fund managers whose names they’d only read in the press. For years, the veteran traders’ privileged insight into their own economy had given them an edge in the copper market, where China accounts for more than half of global demand.

But now they were bewildered. Everything in China pointed to a market that should be slumping, and yet prices were soaring on a wave of speculative money. What were they missing?

The approaches – direct and through intermediaries, to fund managers like Pierre Andurand and Luke Sadrian who had made a splash as some of the market’s biggest bulls – highlight the tug of war that has gripped the copper market in the past few months.

On one side are bullish fund managers in London and New York, who have plowed tens of billions of dollars into copper with an eye to future shortages. On the other are Chinese purchasers, more focused on the here and now, who have rarely if ever been so gloomy.

For the Chinese traders, it has been a humbling experience. The downbeat mood at home had persuaded them to bet against international copper prices. Then a wave of investor buying pushed prices to a record, and traders who fancied themselves the smartest players in the market were wiped out.

“This year has been tough for Chinese traders,” Tiger Shi, managing director at broker Bands Financial Ltd., said in an interview last week. “Their vaunted information advantage over the Chinese physical market didn’t bring them the rewards they imagined.”

But now, as the dust settles on last month’s frenzy, the importance of the Chinese market has reasserted itself. Prices have dropped about 13% from the peak above $11,100 a ton, as speculators sharply reduced their bullish bets in the wake of the surge — with much of that reduction driven by trend-following funds, according to traders.

Without western investors buying, all eyes are back on China, and a copper market that several industry insiders say is still the weakest they’ve ever seen it.

The tug of war between the two is likely to determine where copper prices go next: If tentative signs of a recovery in Chinese buying are sustained, some copper bulls believe the market could be gearing up for fresh record highs in the second half of the year.

But if weak Chinese orders persist, it would suggest that the soft patch is not just a result of delayed buying, but an indicator of poor underlying demand. Prices could fall even further — back to $9,000 or even $8,000 a ton, according to the most bearish traders.

It’s a dynamic that’s likely to dominate conversations as more than 1,000 smelter executives, traders, bankers and analysts are set to gather in Hong Kong this week for the London Metal Exchange’s annual Asia party. It’s traditionally an occasion for western investors to glean insight into Chinese fundamentals, but this year Chinese traders are likely to be just as interested in better understanding their counterparts.

It’s also a sign that, after more than two decades in which China’s industrialization and urbanization has been the major driver of the copper market, the situation is evolving as the electrification of everything gobbles up greater volumes of copper the world over.

Among Chinese copper traders and the fabricators who shape raw metal into pipes, wires and other parts used in everything from air conditioners to power transmission cables, the mood remains overwhelmingly gloomy.

“Business is shrinking significantly. The physical sales business is very bleak”

Even though some of the people Bloomberg spoke to in the past two weeks said they had seen a recent uptick in demand, they were reluctant to suggest that the market is turning around.

“This could be the most difficult year during my over-a-decade industry history,” said Ni Hongyan, vice general manager at trading firm Eagle Metal International Pte. “Business is shrinking significantly. The physical sales business is very bleak,” she said.

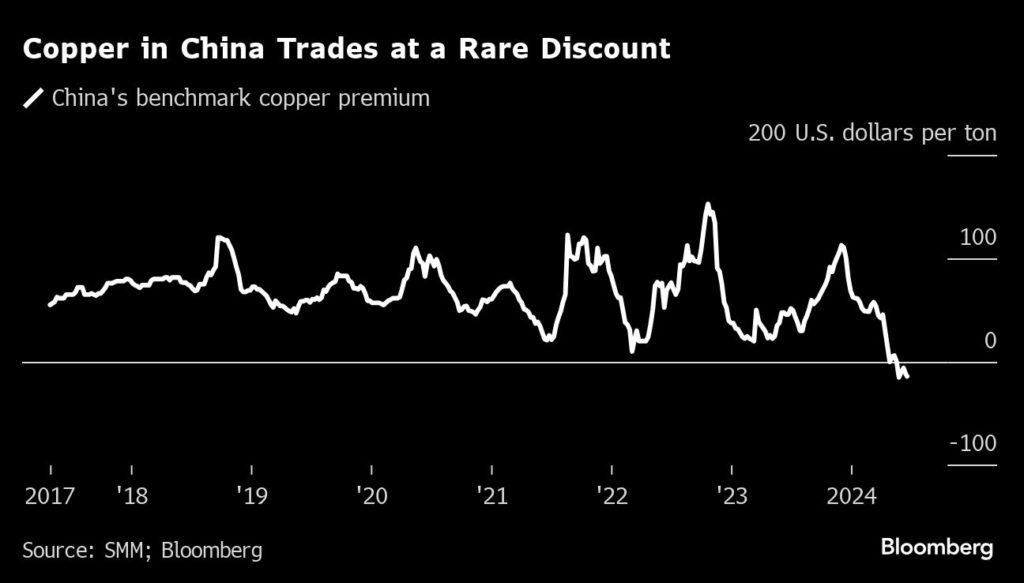

The data paints a similar picture. Copper in Shanghai’s tax-free bonded zone has been selling at a highly-unusual discount to London Metal Exchange prices for more than a month. That was painful for many Chinese merchants, who consider the second quarter the peak season for fabricators to purchase and prepare raw material stocks after the annual political meetings of the country. Instead, copper inventories on the Shanghai Futures Exchange have risen by 78% since the end of Chinese New Year to a record high for this time of the year.

A senior executive at one of the world’s top metals traders said the market for refined copper in China was weaker than he had ever seen it – “by a distance.”

Short squeeze

The disconnect between the Chinese market and western investors had been building for several months. Investors and analysts fell over one another to make the most bullish prediction for copper prices amid forecasts of soaring demand from the energy transition, and challenges boosting mine production. A series of reports estimating massive amounts of copper needed for artificial-intelligence data centers added to the frenzy.

Goldman Sachs Group Inc. said copper was in “the foothills of what will be its Everest,” predicting prices would average $15,000 a ton next year, while Andurand called for copper to hit $40,000.

The situation came to a head in May. As copper prices in China lagged international prices, many domestic traders had been placing bets that the gap would narrow, going short the international copper contracts and long the Shanghai market. After their brokers refused to put on new short positions in London to avoid being exposed to volatility during a week-long Chinese holiday, some traders placed bearish bets on the Comex in New York instead.

But as investor money kept piling in to the market, particularly US copper futures in New York, the Chinese traders were caught in a short squeeze. Faced with rising copper prices, their cash flow was running out and they had no choice but to give up, causing an unprecedented blowout in New York futures that saw them trade far above other price benchmarks.

Since then, however the Chinese market has reasserted itself.

Chinese copper exports hit a record 149,000 tons in May. LME stocks in South Korea and Taiwan — the locations closest to China — have been rising. And traders have been rushing to ship copper to the US to arbitrage the difference in prices – though none of it has yet appeared in Comex-registered inventories.

‘Not there yet’

In compiling this account, Bloomberg spoke to more than a dozen senior figures in China’s copper trading industry, most of whom who asked not to be identified discussing private information.

Many of the traders gathering in Hong Kong this week will still be nursing their wounds. The past six months could be among the worst performing period in their copper trading careers, several said.

For the wider market, the key question is what happens next.

In China, some traders say there have been tentative signs of a pick-up in buying in the past couple of weeks, a move which, if sustained, could put a floor on prices. Inventories of copper on SHFE have fallen for the past two weeks, albeit by a modest 14,000 tons. Beijing is also set to announce more long-term policy support for the economy at a key Communist Party meeting next month, which is seen boosting demand for raw materials like copper.

Wang Wei, general manager at major copper trader Shanghai Wooray Metals Group Co., which sells refined copper to hundreds of Chinese fabricators, said that demand was “rebounding a bit,” although only to return to similar levels as a year ago.

But there are still reasons to worry about China’s underlying copper consumption. Property is a key driver of copper demand, and the weakness in the Chinese sector is likely to continue as a drag, according to Eugene Chan, trading manager at Zhejiang Hailiang Co. There are also some indications that high prices are spurring a greater push for substitution of copper for aluminum.

“The financial market flood of net new length has become a trickle. Without that incremental macro-driven buyer, it comes down to whether the underlying physical market can support the current price,” said Colin Hamilton, managing director for commodities research at BMO Capital Markets. “We have to reset to a level to bring these buyers back, and we’re not there yet.”

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

OBITO

thank you, great article !