Gold price slips with rising yields as traders weigh data, Fed hiking

Gold slipped with rising Treasury yields as traders weighed mixed US economic data and the Federal Reserve’s interest-rate hiking path.

Data Tuesday showed a bigger-than-expected drop in US home construction, while production at US factories increased in July for the first time in three months.

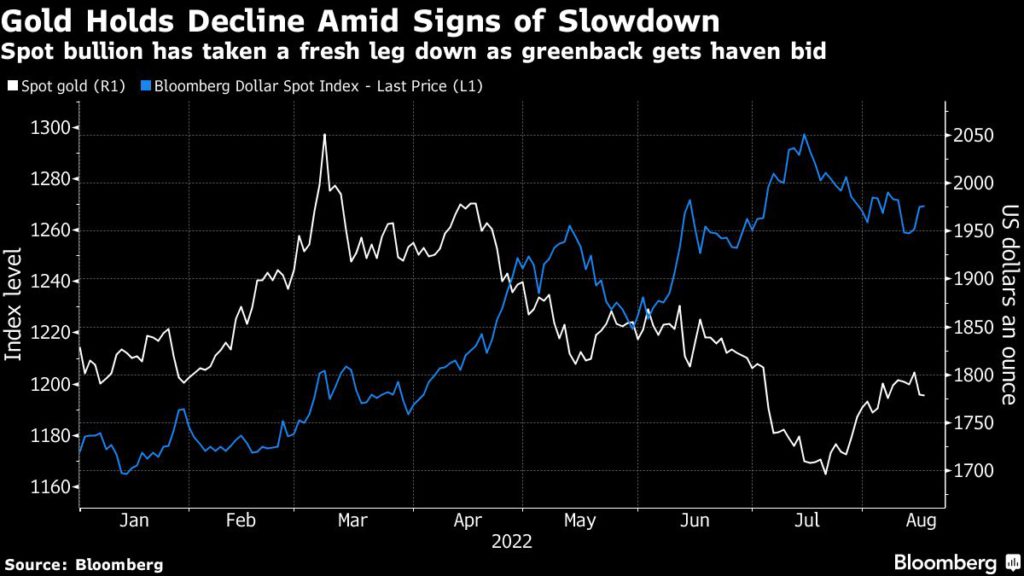

Bullion has taken a fresh leg down after rising for four weeks as the US currency renewed its ascent and bond yields remained elevated.

The price drop was “very contained” and the precious metal “arguably held up relatively well above $1,770 given the earlier renewed strength in the dollar which has since reversed,” said Nicky Shiels, head of metals strategy at MKS PAMP SA. “Overall, persistent US dollar strength and the climb up in US yields ensures rallies are capped.”

Worldwide holdings in bullion-backed exchange-traded funds have contracted for the past nine weeks, signaling reduced interest from the investor community.

Gold’s next move may hinge on the minutes from the Fed’s July meeting, which are scheduled for Wednesday and may offer clues on the size of the next rate hike. Ahead of their release, economist Nouriel Roubini warned that markets expecting a pivot and the Fed cutting rates in 2023 “sounds delusional.”

Spot gold declined 0.2% to $1,775.74 an ounce as of 5 p.m. in New York, after tumbling 1.3% on Monday. Bullion for December delivery slipped 0.5% to settle at $1,789.70 on the Comex. The Bloomberg Dollar Spot Index was little-changed after earlier rising as much as 0.3%. Spot silver declined, while platinum and palladium gained.

(By Yvonne Yue Li, with assistance from Eddie Spence and Ranjeetha Pakiam)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments