Gold price may get China, India physical demand boost as ETF spike fades

(The opinions expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

With all the excitement in silver in recent days as retail investors rushed to buy, the status of the gold market may have been overlooked, though it could be argued that the yellow metal faces a more interesting 2021.

There are several ways of looking at spot gold’s recent performance, ranging from the view that it had a stellar 2020 to disappointment that it hasn’t maintained its rally and the price has stagnated in recent months.

First, the facts.

Spot gold rallied 25% in 2020, having ended the year at $1,896.49 an ounce, up from the $1,507.01 at the end of 2019.

The pandemic also ensured that interest rates across the world will remain extremely low for an extended period

The price also reached a record high of $2,072.49 an ounce on Aug. 7, but has since dropped 11.5% to end at $1,833.55 on Wednesday.

A 25% return certainly looks positive on the surface, but may actually be considered soft by some market participants, who had forecast stronger gains and harboured the expectation that the rally would extend well beyond the psychological $2,000 an ounce barrier.

Since reaching the all-time high, gold has gradually shifted into a lower trading band, with a brief rally at the start of the year as former U.S. President Donald Trump caused some concerns with his failed efforts to overturn the November election that saw him lose convincingly to now President Joe Biden.

What is worth doing is looking at what were the main drivers of gold’s performance in 2020, and how are they shaping up in 2021.

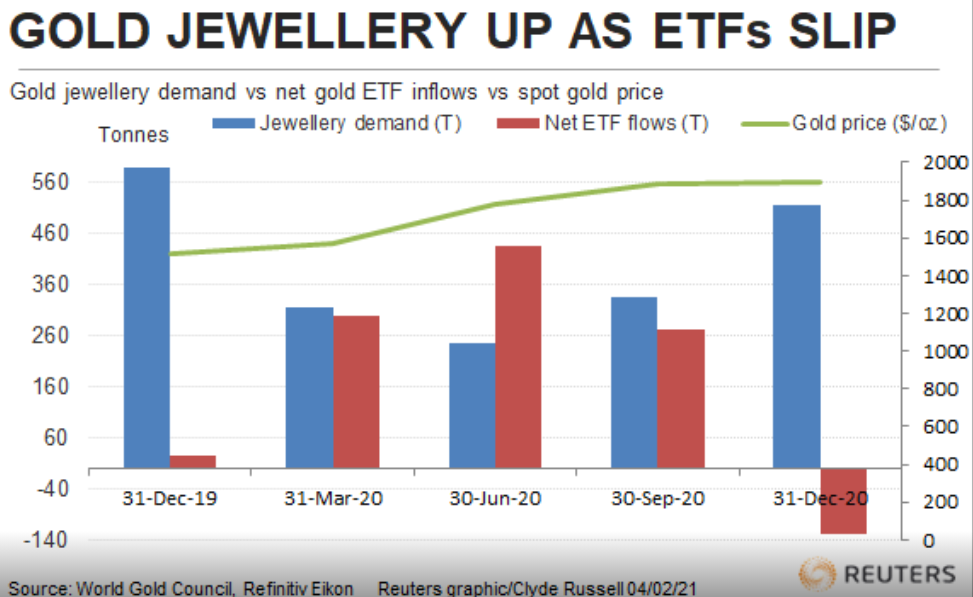

There is little doubt that buying into exchange-traded funds (ETFs) were the major factor in gold’s strong 2020, with World Gold Council (WGC) data showing a massive 120% surge in inflows to 877.1 tonnes in 2020, up from 398.3 tonnes in 2019.

This isn’t too surprising given how gold’s position as a safe haven saw investors flock into ETFs as the coronavirus pandemic spread across the globe, upending economies and leading to concerns about other asset classes such as stock markets.

The pandemic also ensured that interest rates across the world will remain extremely low for an extended period, a factor that traditionally supports gold.

However, it’s also worth noting that the inflows into ETFs, which were strong in the first three quarters, reversed in the fourth, with the WGC numbers showing an outflow of 130 tonnes after a cumulative inflow of 1,007.1 tonnes in the first nine months of the year.

Recently, ETF inflows appear to have steadied, with the largest fund, the SPDR Gold Trust, holding 37.21 million ounces as of Wednesday, down slightly from 37.64 million at the end of 2020.

However, the fund’s holdings have dropped by 9.5% since the 41.12 million ounces recorded on Sept. 21, which was the highest in nearly eight years.

Positive physicals

While many analysts focus on interest rates, monetary policy expectations and the level of the U.S. dollar in formulating views on gold, it does seem that the physical market plays a substantial, if somewhat underappreciated role.

There is no way to sugar-coat it, 2020 was a dreadful year for physical gold demand, with jewellery demand plunging 34% to 1,411.6 tonnes from 2,122.7 tonnes in 2019, according to WGC figures.

Other physical applications weren’t as dire, with technology use dropping 7% to 301.9 tonnes, and bar and coin purchases rising 3% to 896.1 tonnes.

Another bearish factor was central bank demand, the third pillar of gold along with physical buying and investment products, which fell by 59% in 2020 to 272.9 tonnes from 668.5 tonnes the prior year.

While predicting central bank buying is challenging, it’s likely that physical demand could rebound in 2021, especially in the two largest consumers, China and India.

Jewellery demand in China was smacked down 35% to 415.6 tonnes in 2020, while in India it slumped 42% to 315.9 tonnes.

This wasn’t surprising given the lockdowns to combat the coronavirus and the accompanying economic hit, but there are already signs of a turnaround as the recovery from the pandemic starts to gather momentum.

China’s fourth-quarter jewellery demand was 145.1 tonnes, the most since the fourth quarter of 2019 and up 22.4% from the prior quarter.

India’s jewellery demand was 137.3 tonnes in the fourth quarter, also the most since the fourth quarter of 2019 and 125.8% up from the prior quarter.

If physical demand returns as the global economy improves, and ETF flows and central bank buying remain more or less constant, it’s possible gold will resume a bullish trend in 2021.

(Editing by Christian Schmollinger)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments