Global commodity shock enters next phase with recession test

Commodities are hitting powerful headwinds after a first half dominated by the supply turmoil and inflationary shocks unleashed by Russia’s attack on Ukraine. Below, What to Watch looks at what the second half holds for raw materials from natural gas and crude to grains, gold, iron ore and lithium.

Across markets, there’s growing talk that high prices for raw materials will be cured only by recessions in the second half. Oil has sunk toward $100 a barrel, metals are poised for a deep quarterly slump, and there’s a cool-off in crops.

But the bearish view will tested. Goldman Sachs Group Inc. — among the more bullish commodity-watchers — just said prices haven’t yet topped out. That’s even with Bloomberg’s index of spot commodities down 13% from a record.

“We agree that when the economy is in a recession for long enough, commodity demand falls and hence prices, fall,” analysts including Jeffrey Currie wrote in a note. “Yet we are not yet at that state, with economic growth and end-user demand simply slowing, not falling outright.”

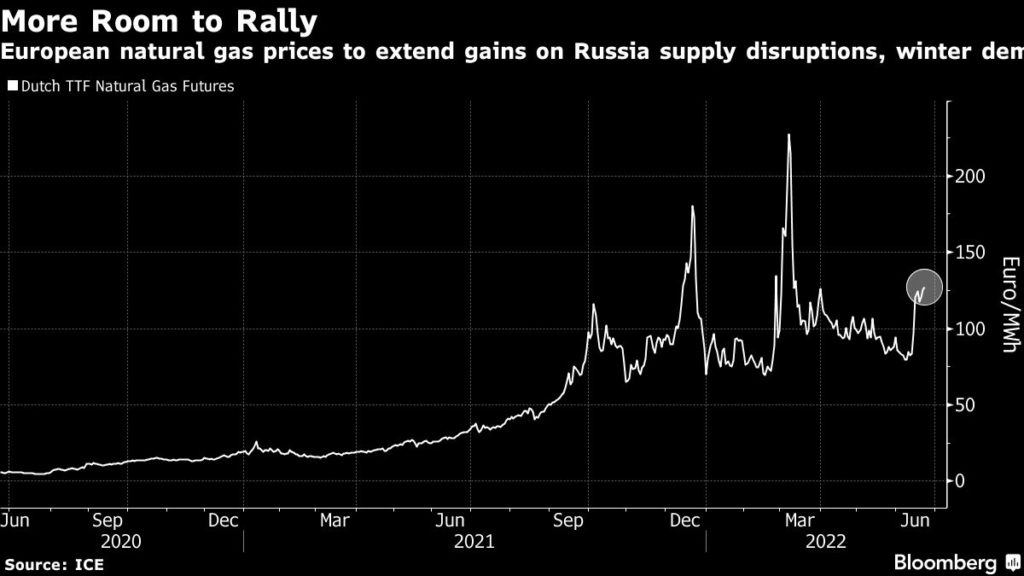

A hard winter

“Even if we don’t feel it yet, we are in a gas crisis,” Germany’s Economy Minister said last week. Russia’s squeeze on flows to Europe risks a historic global shortage — and higher prices still — with peak demand looming this winter. Consumer nations are preparing to run economies without the fuel, and competition for liquefied natural gas between Europe and Asia will intensify — all the more so if a key US export plant stays shut.

Expensive gas will increase power bills for households and businesses, and a full-blown crisis would shut industries from chemicals to fertilizers, fanning the flames of global inflation. Germany is preparing to trigger the next stage of its emergency plan, and gas rationing across Europe is a real prospect. In Japan, one of the world’s top LNG importers, the government is trying to curb consumption and is considering unprecedented moves to procure more fuel.

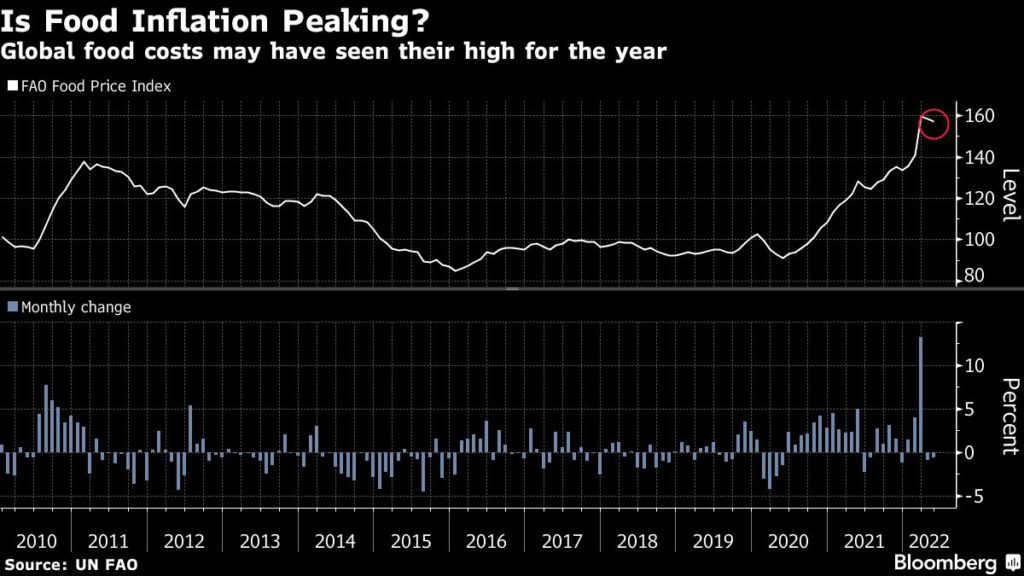

Feeding frenzy

Is the food crisis past its worst? There’s growing talk that grains and cooking oil prices have peaked — and maybe global food costs have too. More supply is on the way, with winter wheat harvests getting under way in the northern hemisphere, and spring wheat, corn and soybeans following later. The focus then turns to production in Australia, Brazil and Argentina. Barring weather woes, output could rise as farmers plant more in response to elevated prices.

Global stockpiles will remain crimped in the coming season — and millions of tons of grains are stuck in Ukraine — but they may not get substantially tighter. Some Ukrainian cargoes are reaching Europe, while Russia is heading for a bumper crop. Palm oil, the world’s most consumed edible oil, just slumped to its lowest level this year as top producer Indonesia ramps up exports, while wheat, corn and soybeans have tumbled from their highs. Global food costs have already fallen from their all-time peak in March, and more declines could follow.

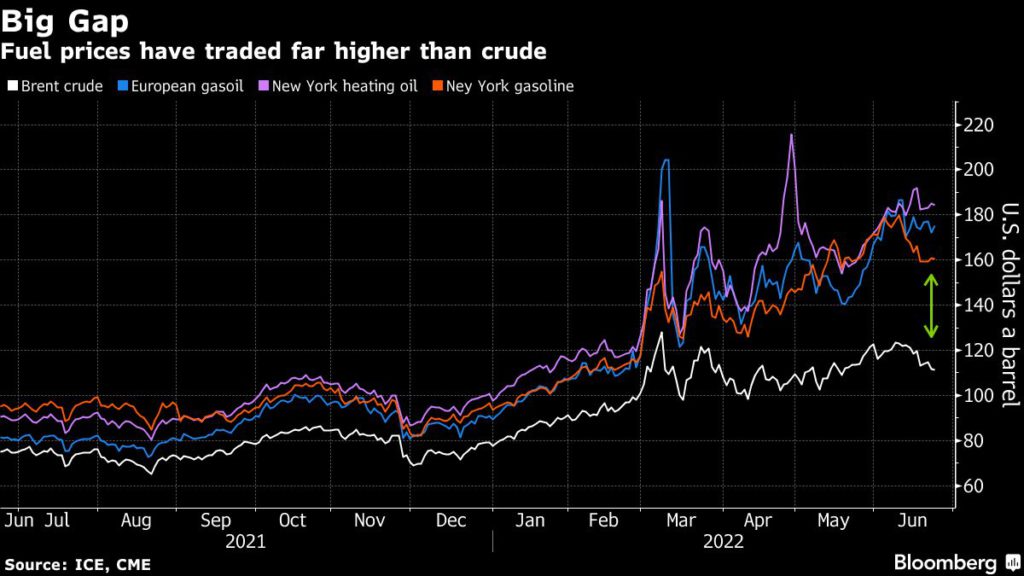

Oil dilemma

Refined products from gasoline to diesel are the oil market’s hot spots right now, and the big question for the second half is whether demand can be sustained amid rocketing prices. A cocktail of fuel subsidies keeping consumption afloat — together with limited refining capacity — has powered rallies that have outstripped crude prices. US gasoline at $5 a gallon has caught political attention, and could trigger policy action ahead of the November mid-term elections.

There’s little consensus on what’s happens next in crude, but we can expect louder discussions about how much OPEC and its allies can or will pump — especially if prices stick above $100 a barrel. While Citigroup Inc.’s veteran oil-watcher Ed Morse sees crude easing to the $80s by the fourth quarter on “strong headwinds to growth”, Goldman Sachs is among notable bulls, saying oil prices needing more gains to normalize “unsustainably low” inventories.

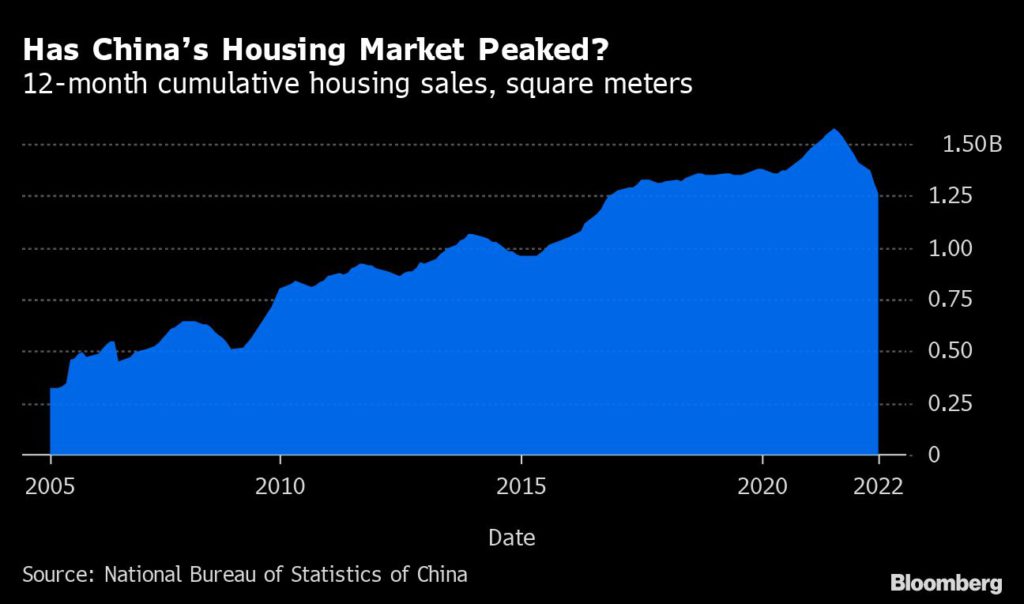

The China factor

Tumult in Europe and the Federal Reserve’s hawkish turn have left issues in China arguably less decisive than usual for commodities markets. But the top importer of energy, metals and crops will still be a key factor in coming months, especially if the economy ramps up to meet President Xi Jinping’s goal of 5.5% annual growth. That would lift demand, but metals markets in particular show why bets on any massive stimulus boost may prove risky.

The heart of the problem is China’s ailing property market, which has been in a long-term downturn since Xi warned that housing was “not for speculation.” There are few signs that the government is close to reversing its squeeze on a sector that was absolutely pivotal in rebooting iron ore and copper markets after previous downturns. Extra infrastructure spending just isn’t enough to offset the loss. That puts Xi’s growth goals at risk, which means iron ore and copper might struggle to match this year’s highs.

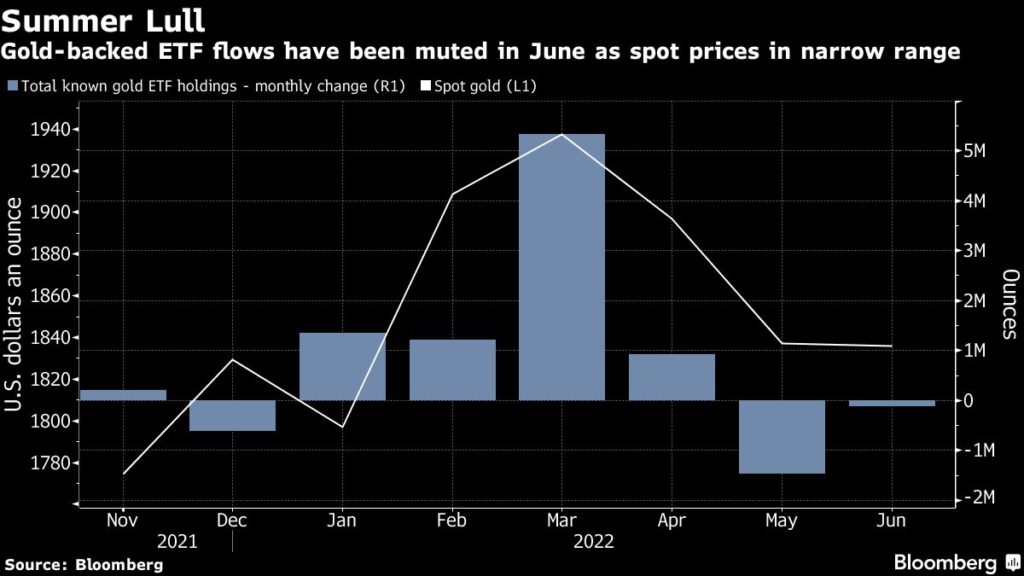

Golden mean

After spiking to a record after Russia’s invasion, gold is close to where it started the year, and consensus forecasts for the fourth quarter put prices just a smidgeon above where they are now. If that looks a bit boring, remember that the powerful forces keeping the precious metal in check speak directly to the dynamics shaping wider commodity markets. Certainly, gold faces some intimidating headwinds: outsized interest rate hikes from the Fed and other central banks; a strong dollar; and struggling physical demand in top consumer China.

But doubts over the Fed’s ability to fight inflation without a US recession are lending support, and a hard landing for the global economy could revive haven demand. In that sense, gold will be the measure of whether central banks can rein in price pressures without crushing growth. The tried-and-tested haven asset has been above $1,800 an ounce for most of the first half and might end the year there unless there’s another major shock.

Battery boom

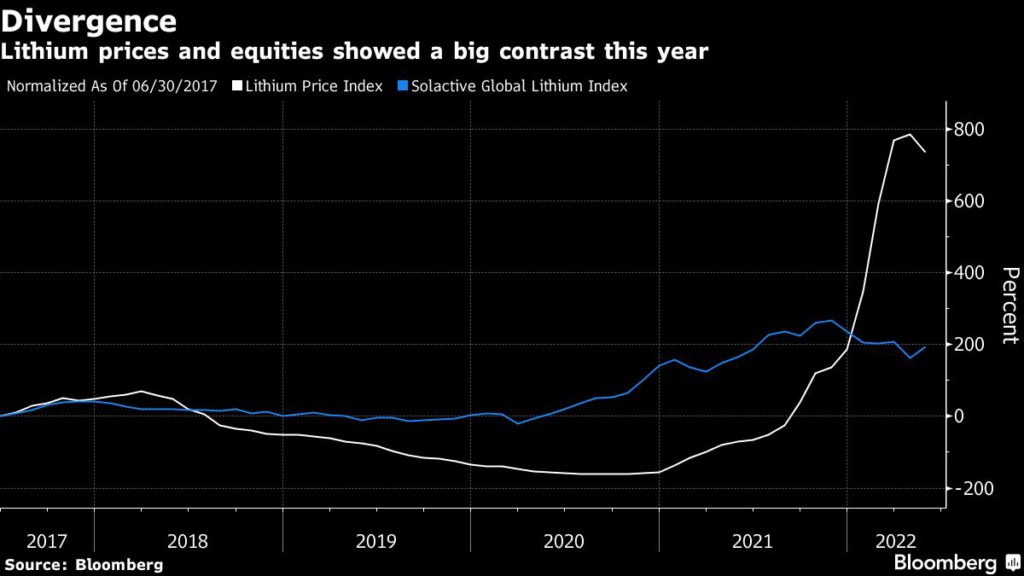

Lithium prices are revving up again after a brief pause in anotherwise sizzling rally over the past 18 months. The vital ingredient in electric-vehicle batteries could be in for further gains in the rest of 2022, with demand in the world’s largest EV market reviving after Covid-19 curbs that saw manufacturing slow and consumers halting car purchases.

Shares in lithium producers might finally catch up with the spike in lithium prices. Optimism around battery metals at one of world’s largest mining conferences recently in Toronto suggests that big money — especially from generalist investors — may soon flow into the lithium market. A solid demand recovery in China will help the market soak up additional supplies on the way, including from top produers Albemarle Corp. and SQM.

(With assistance from Doug Alexander)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments