Glencore-backed zinc miner is getting crushed in the debt market

A Peruvian zinc miner has seen its bonds tumble to an all-time low as investors grow increasingly concerned about its ability to refinance maturing debt and Swiss commodities giant Glencore Plc looks to sell its controlling stake.

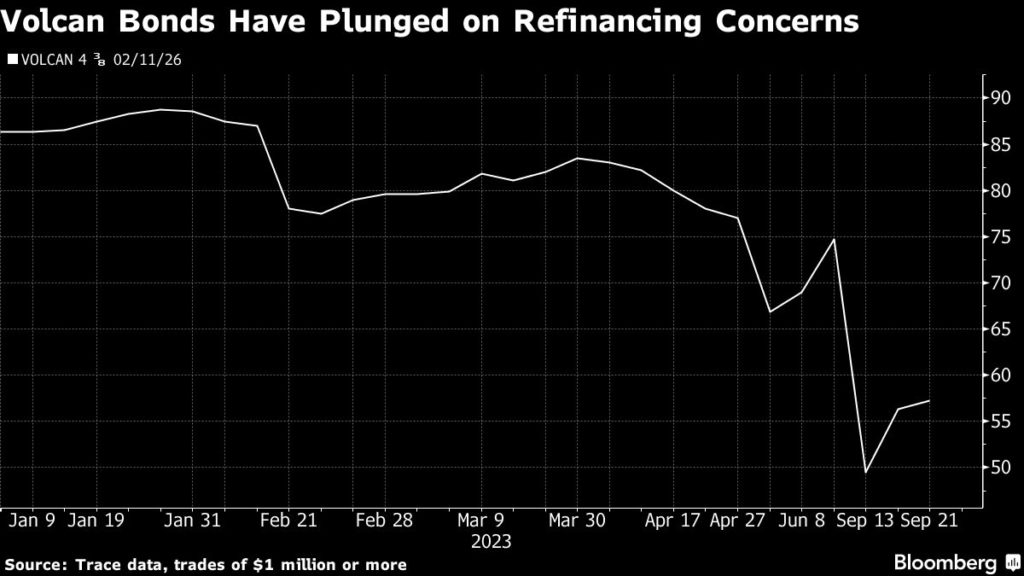

Volcan Cia Minera SAA’s dollar-denominated notes closed as low as 49.5 cents on the dollar last week, then edged higher to around 57 cents this week, after trading closer to 90 cents in early February. The miner has posted losses in four of the last five quarters and seen cash levels drop as zinc prices have slumped in a global economy where growth is slowing.

The company has hired Bank of America and Apoyo as advisors as it seeks to address its liquidity concerns, Diego Garrido-Lecca, Volcan’s interim chief executive officer, wrote in an email to Bloomberg. It has options including selling assets, he said.

But it faces pressure now, including friction with Glencore and a debt downgrade this month. Late Monday, Volcan announced the appointment of a new chief executive and a new chairman. The outgoing management said those changes were made by Glencore-aligned directors, and may have been enacted illegally. The miner said the board decisions were carried out legally and in line with company rules.

Glencore last year started looking into selling its 23% stake in Volcan, amounting to 55% of its class A voting shares, as the Swiss firm looks to simplify its business. That potential for a change in a key owner adds uncertainty to the outlook for Volcan’s debt.

Garrido-Lecca declined to comment on the process of Glencore selling its stake in Volcan, while a representative for the Swiss firm declined to comment.

Zinc falls

Moody’s Investors Service on Sept. 8 downgraded Volcan two notches to Caa1, one of the lowest ratings tiers, citing the company’s refinancing risk. Volcan has about $105 million of obligations coming due through the end of 2024, according to Moody’s, which estimates the company’s operations will burn through about $203 million during that period after making necessary capital expenditures.

The Lima-based miner ended the second quarter with about $50 million of cash and has a revolving credit facility of $50 million available until November. Its liquidity is coming under pressure from lower prices for zinc, which is often used to galvanize steel for automaking or construction.

Futures have risen in the last few weeks but have still fallen by about 30% from a January peak because of China’s uneven recovery and the prospect of more supply coming on line. Volcan in July said it was suspending its Islay mine in central Peru, joining a string of producers to curtail production amid weaker prices.

Some analysts see an opportunity in the company’s debt. Bonds of Volcan trimmed losses after hitting a record low.

Lucror Analytics upgraded its recommendation for the bonds to “speculative buy” from “hold” earlier this week on the back of depressed valuations. The notes “are at a historic low, and have become more attractive in our view, given the company’s proven ability to refinance its debt,” analyst Josseline Jenssen wrote in a note.

Liquidity options

Volcan’s management and board are capable of dealing with the company’s current financial situation, with options including the renewal of the revolving credit facility and the sale of hydroelectric and cement assets, interim CEO Garrido-Lecca said in a written response to questions.

But it’s unclear how much money can be raised from selling these assets, said Omar Zeolla, a research analyst at Oppenheimer & Co. The company has a loan due in 2026, plus around $360 million of dollar-denominated bonds due in February 2026.

“Volcan has watched its cash being drained, creating a brewing liquidity crisis,” said Bevan Rosenbloom, a senior credit analyst at Seaport Global Holdings LLC.

(By Vinícius Andrade and James Attwood, with assistance from Marcelo Rochabrun)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments