Flash crash shows why it’s tough to be bullish on gold right now

Gold’s swift drop to the lowest since March has highlighted a tough truth for the precious metal — there’s a growing list of reasons to be gloomy.

While Monday’s flash crash was exaggerated by a combination of technical factors and poor liquidity, the initial trigger remains true — strong US jobs data showed the world’s largest economy is well on its way to recovery. That sets the stage for the tapering of stimulus by the Federal Reserve, potentially removing one of the key drivers that helped send gold to a record last year.

A strengthening dollar, plus growing expectations that inflation will prove manageable, are adding to the headwinds. Exchange-traded funds have also cut their holdings significantly this year. Gold traded 1.9% lower at $1,730.13 an ounce by 4:33 p.m. in New York, after earlier tumbling as much as 4.1%. Bullion futures for December delivery fell 2.1% to settle at $1,726.50 on the Comex.

Investors will now turn their attention first to the US inflation data scheduled for later this week, and then ahead to signals from Fed officials at the Jackson Hole conference later this month. The timing of tightening by the US central bank is key, and hawkish talk from Chair Jerome Powell could spell the start of a definitively bearish market for bullion.

No hype

Gold’s drop after payrolls beat expectations on Friday was triggered by a sharp rise in inflation-adjusted Treasury yields, which determine the opportunity cost of holding the non-interest bearing metal.

But when yields dropped deeper into negative territory in the past month, gold prices failed to benefit.

That shows just how negative sentiment has become for bullion after the metal’s relatively poor performance this year. Gold is an asset that thrives on momentum, and can be left vulnerable if the price fails to rally for a long time. Further rises in real rates driven by strong economic data could spark more precipitous drops.

Inflation fading

Whether rising prices associated with economies reopening will prove transitory or persistent has been a major theme for markets in 2021. Gold’s relationship with inflation is complicated — it’s often touted as a hedge against runaway price gains, but has historically tended to benefit mostly when they coincide with periods of high unemployment.

So far, the market is pricing in transitory inflation, as demonstrated by the falloff in US breakeven rates further down the curve. That would imply healthy and controlled price increases which wouldn’t benefit gold. The consumer price index due Wednesday will prove the latest gauge for investors, and is expected to be more muted compared to previous months.

“It’s hard for it to be bullish for gold at the moment,” said Marcus Garvey, head of metals strategy at Macquarie Group Ltd. “If it does soften and show that some of the recent price gains are easing, then there’s less upward impetus for inflation. But that doesn’t really reduce taper expectations because inflation is already sufficient to be ticking the box.”

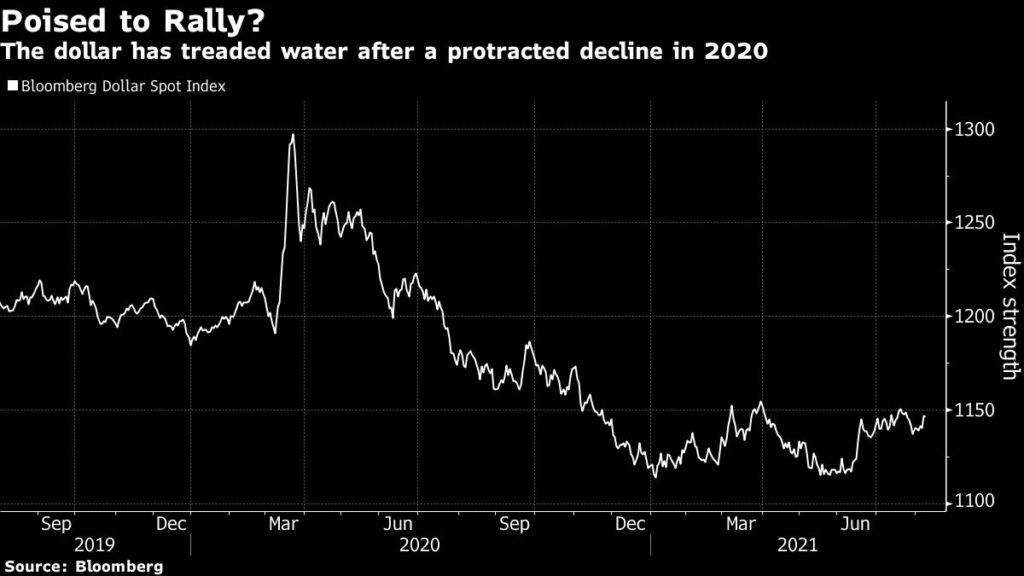

Dollar’s return

A major driver of gold’s strong performance last year was a protracted weakening of the dollar. Fast forward to 2021 and there’s signs we may see that trend reverse, putting pressure on bullion.

Strong US jobs data raised expectations for Fed rate hikes, giving the dollar its biggest gain in about a month on Friday. Meanwhile, money markets indicate the European Central Bank won’t tighten until at least mid-2024. That sets the stage for a stronger greenback, which would hurt gold.

Technicals

Gold’s plunge earlier Monday has broken below the neckline of a weekly head and shoulders pattern that may embolden bears in the medium term. Unless gold ends the week above the neckline, which currently lies at approximately $1,760, the outlook would remain weak based on the technical analysis.

Prices also tested and broke below the 100-week simple moving average, before pulling back. This average has offered support to prices most times since the Dec 2015 low. It lies at $1,738 for this week and will be watched closely by bulls and bears alike.

“Gold is now technically toasted and requires some resilience to stave off some key levels,” Nicky Shiels, head of metals strategy at MKS (Switzerland) SA, wrote in a note. “On the topside, a retaking of $1,750 would help install confidence (and hold off a move lower).”

ETFs exodus

Bullion-backed exchange-traded funds were a pillar in driving the metal to a record last year. But successful vaccine rollouts and stronger-than-expected recoveries in the western world prompted investors ranging from family offices to pension funds to cut their ETF holdings significantly this year, particularly in the first quarter.

To be sure, ETF holdings remain at historically high levels. And a rebound in gold imports in top consumer India could offer support to prices — while demand there was hammered earlier this year by the emergence of the delta variant of coronavirus, rising imports show an appetite for gold may be starting to pick up.

(By Eddie Spence, Akshay Chinchalkar and Yvonne Yue Li, with assistance from Swansy Afonso and Greg Ritchie)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments