Copper short squeeze in New York is rocking metals markets

A massive dislocation between the prices for copper traded in New York and other commodity exchanges has rocked the global market for the metal and prompted a frantic dash for supplies to ship to the US.

The source of the disruption is a short squeeze that has driven up prices on the Comex exchange in recent days. The premium fetched by New York copper futures above the London Metal Exchange price has rocketed to an unprecedented level of over $1,200 per ton, compared with a typical differential of just a few dollars.

The blowout in that price spread wrong-footed major players from Chinese traders to quantitative hedge funds, some of whom are now scrambling for metal that they can deliver against expiring futures contracts.

The wild swings highlight how commodity markets can spiral rapidly out of control when market participants are no longer able to finance their positions — a situation that becomes more likely amid the low inventory environment and logistical snarls that commodity traders have faced in everything from nickel to cocoa in the past few years.

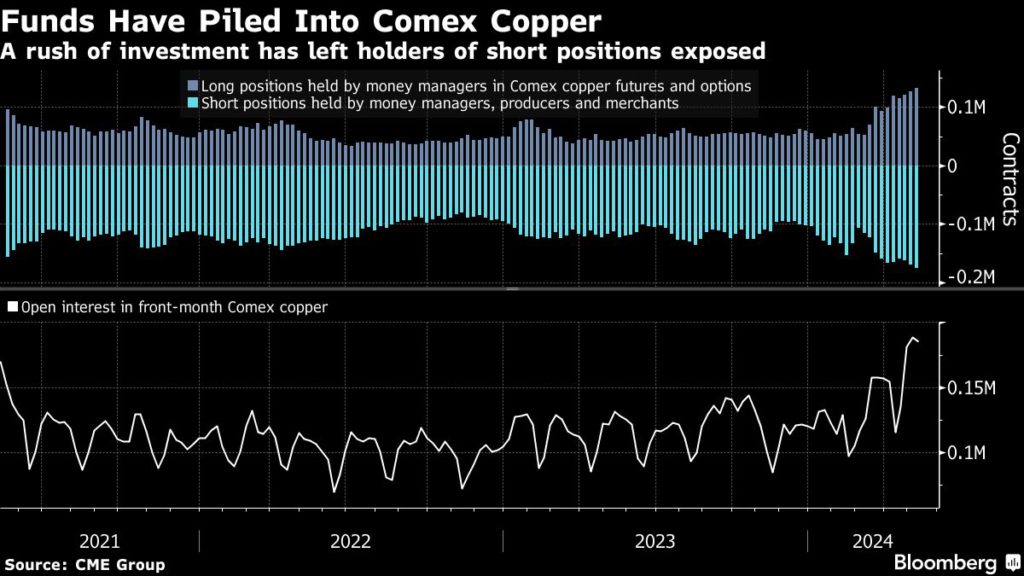

The volatility on Comex also reflects a surge of interest from speculators after forecasts that long-term copper mine production will struggle to keep pace with demand. While less important than the LME, Comex, which is part of CME Group Inc., is a key playground for investors, some of whom have used the exchange to build up large bullish bets on copper in recent months.

“The broader story is that there are new investment funds that are boosting their exposure to copper for a multitude of reasons, and while that’s a global trend, a huge amount of that investment has been heading to Comex,” said Matthew Heap, a portfolio manager at Orion Resource Partners, the largest metals-focused fund manager.

While copper prices have been rising for months, this week’s spike was specific to the Comex and the most-active futures contract for July delivery. By Wednesday, the July price had soared as much as 10%, touching a record high for that contract, even as the global benchmark contract on the LME traded broadly flat.

The move, according to numerous traders and brokers, was a classic short squeeze. Market participants who had placed bets on the Comex contract moving back into line with prices on the LME and in Shanghai, the other global copper benchmark, were forced to buy those positions back as prices rose, creating a vicious cycle.

The spread of more than $1,000 a ton between Comex and London was “something never seen previously,” said Colin Hamilton, managing director for commodities research at BMO Capital Markets. “There has been a squeeze on short positions into contract expiry, exacerbating the move.”

Hedge funds and other traders had taken the other side of the bullish trades on Comex, betting on narrowing differentials between the contracts in New York, London and Shanghai, or between New York contracts for different delivery dates, often using substantial leverage. With prices on the Shanghai Futures Exchange relatively depressed, some Chinese physical market participants had also sold on the LME and Comex, with plans to export.

The July Comex copper contract soared to a record $5.128 a pound ($11,305 a ton) on Wednesday morning. It also traded at a record premium above the September Comex contract — a situation known in commodities markets as a backwardation, a hallmark of a short squeeze.

The price spike was driven by short covering rather than any overall physical shortage, traders and brokers say, but it has shined a light on relatively tight supplies in the US copper market.

Inventories tracked by the Comex currently total 21,066 short tons, while LME inventories in the US are just 9,250 tons. For comparison, annual US copper demand is almost 2 million tons. Traders say solid demand, and shipping issues at the Panama and Suez canals, have left the market tight. US copper imports year-to-date are down 15%, according to consultancy CRU Group.

“We continuously monitor our markets, which are operating as designed as market participants manage copper risk and uncertainty,” the CME said in a statement.

Short squeezes are nothing new in commodity markets, and they often prompt a mad scramble to find supplies of raw materials that underpin paper contracts.

In 2020, as Covid locked down much of the world, gold traders raced to ship metal to address a similar dislocation between New York and London bullion prices. And in 1988, a short squeeze in aluminum led some traders to load the metal into jumbo jets — a highly unusual and costly mode of transport for industrial raw materials — in order to get it on to the LME as soon as possible.

The current Comex copper squeeze has triggered a similar dash to send copper to the US. Chinese traders have spent the past 24 hours calling around shipping companies to try to secure transit to the US, according to people familiar with the matter.

Traders and miners in South America have also raced to boost their US shipments. Chilean copper-mining giant Codelco is directing all of its available volumes to the market and also negotiating with customers to postpone some sales so that it can maximize deliveries, people close to the situation said. Codelco didn’t immediately respond to a request for comment.

There have been some signs that the squeeze is easing: the July copper contract edged lower on Thursday morning after coming off its highs from Wednesday, while the premium over cash copper on the LME narrowed to $573 a ton — although still a historically elevated level.

There may be further relief ahead, as investors with bullish positions via commodity indexes are set to start rolling their copper positions in early June, providing an opportunity for traders with short positions to defer delivery, potentially easing the backwardation.

Still, it’s not clear if that will be enough to resolve the squeeze ahead of the expiry of the July contract, which goes into delivery at the start of that month. Chinese traders seeking to transport metal to the US have found that shipping schedules are fully booked, with the earliest available shipping slots from Shanghai to New Orleans at the beginning of July, said Gong Ming, analyst with Jinrui Futures Co.

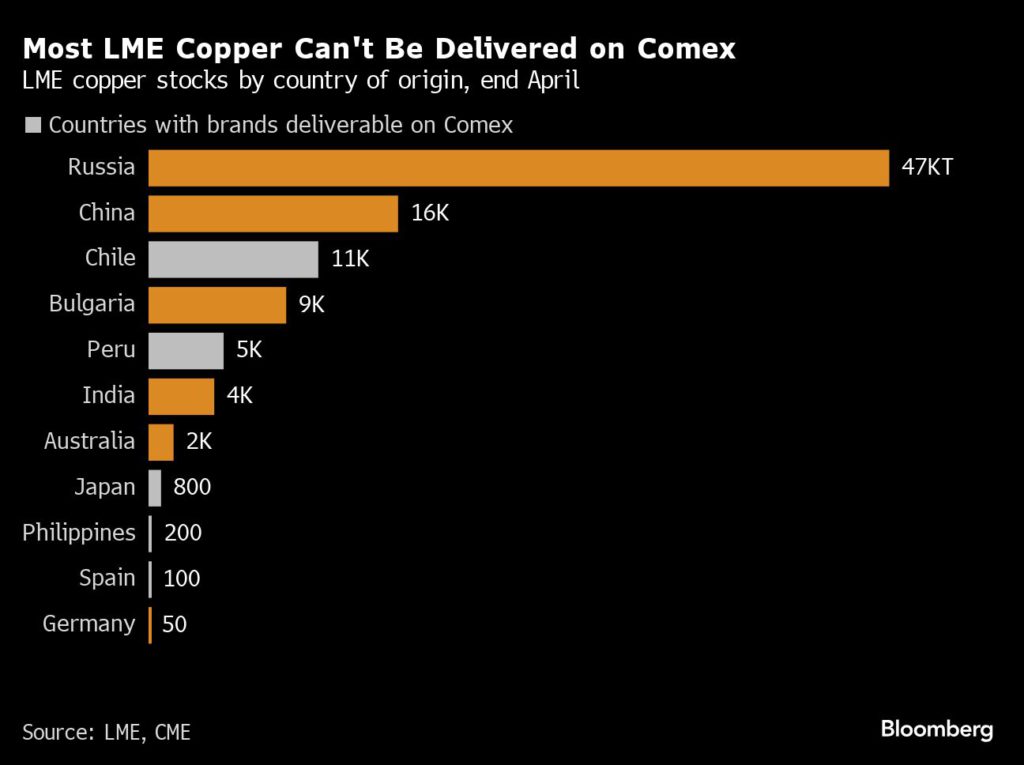

Adding to the predicament of those caught out by the squeeze is the fact that much of the copper inventories outside the US is from brands that aren’t deliverable against Comex futures. For example, more than 80% of the 94,700 tons of copper on the LME at the end of April was produced in Russia, China, Bulgaria or India — countries whose copper isn’t deliverable on Comex.

While substantial inventories have built up in China in recent months, traders estimate that only about 15,000 to 20,000 tons of that could be delivered against Comex futures.

“We do not think the physical arbitrage activity will be sufficient by the July expiry to close the arb on the near month. There is not enough material and not enough time,” said Anant Jatia, chief investment officer at Greenland Investment Management, a hedge fund specializing in commodity arbitrage trading.

“However, physical traders are currently heavily incentivized to move copper into the US and over time the arb market will stabilize.”

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments