Copper price on the way up, but with many ‘ifs’

Copper bulls betting on a strong recovery of physical demand after the Chinese New Year should be wary of getting carried away, market participants say.

A rally fuelled by sentiment and expectations, without an actual increase in consumption, could trap investors in an eventual sharp downturn, such as the one in mid-2022 triggered by the Ukraine-Russia war and an energy crisis.

“The first two weeks of January is always a bit dangerous. People come back after the break feeling refreshed. Things can get a little carried away,” said Guy Wolf, Global Head of Market Analytics at broker Marex.

Benchmark London prices hit a seven-month high of $9,550.50 on Wednesday, while the Shanghai contract leaped to its highest since April 25 on Thursday, on hopes that a U-turn in Chinese covid-19 policy would boost metal demand.

“I am a little skeptical. They were locking people up in apartments but there’s quite a lot of evidence that smelters continue to operate. It’s not like the 2020 lockdowns where China stopped and reopened,” Wolf said.

Helping the copper price rally were also hopes of slowing US interest rate hikes and low copper inventories.

[Click here for an interactive chart of copper prices]

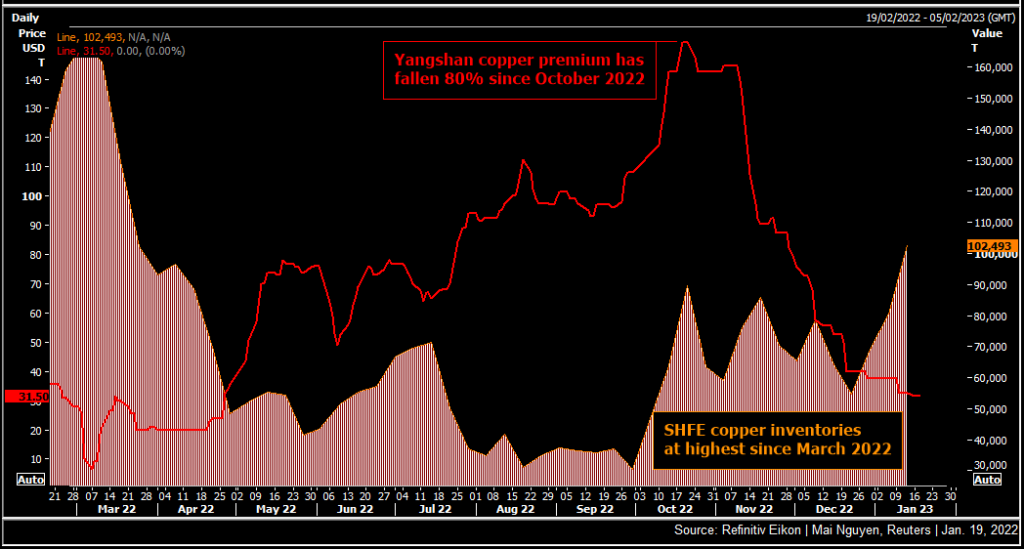

But SHFE copper stocks have been slowly building up, while the premium to import copper into China has plunged 80% since October.

Coronavirus infection in China is rising, and a second wave could come after hundreds of million people travel home for the Jan. 23-27 Lunar New Year holiday.

“I am bearish. The end users haven’t been biting. Their order books are not filled. But then everything could change very quickly after the Chinese New Year is over when the government spending taps turn on,” said a metals trader.

More stimulus and infrastructure spending could be unveiled at the Chinese National People’s Congress in March, ING analyst Ewa Manthey said in a note.

China’s expected recovery is seen solely driven by the services and consumer sectors, which are less metals-intensive than industry, while the Federal Reserve is likely to stay hawkish, Citi analysts said in a note.

However, they still see LME copper hitting $10,000 a tonne in three months.

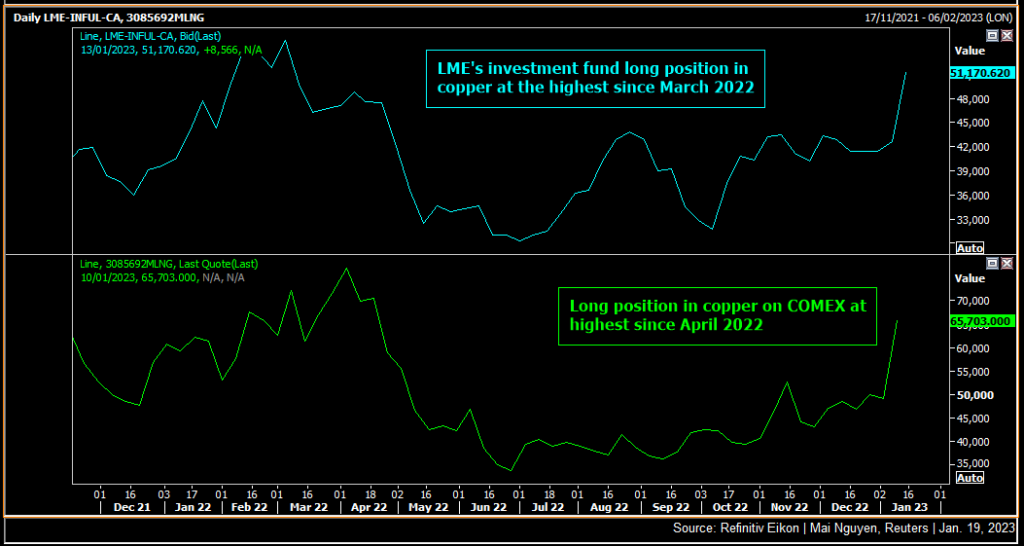

“The vast bulk of last weeks’ copper price rally was associated with fresh long positions, as opposed to substantive short covering. This leaves further room for copper to run considering there remains an outstanding copper short position,” they said.

Long copper positions are building on both the LME and the COMEX.

Copper’s long-term prospects still look bright due to its use in green energy transition sectors such as solar, wind and electric vehicles – which see a strong rise in copper usage.

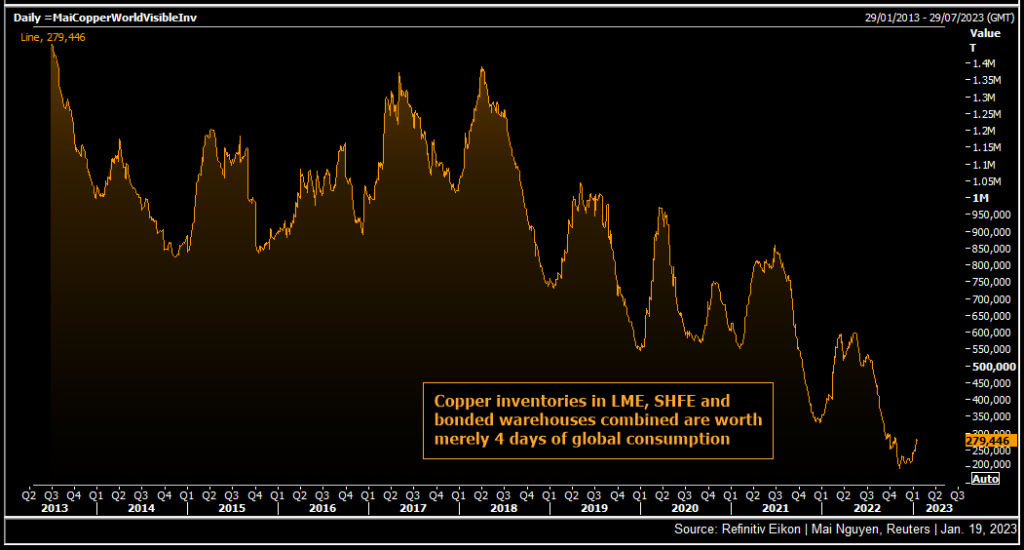

Combined refined copper stocks in LME, SHFE and bonded Chinese warehouses are only four days worth of global copper consumption. The indicator is normally measured in weeks.

“China reopening could easily drive demand up by 100,000-200,000 tonnes, enough to flip the supply-demand forecasts into a deficit,” Jefferies analysts said in a note.

“Supply side concerns remain in place for 2023 in Chile and Peru, which account for around 30% and 10% of global mining supply respectively, posing significant upside risk,” they added.

Most companies expect the Chinese economic recovery to start around March, with some large ones seeing a rebound as early as from late February, said CRU analyst He Tianyu.

($1 = 6.7810 yuan)

(By Mai Nguyen; Editing by Mark Potter)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments