Column: Third European smelter closure compounds zinc conundrum

Europe’s energy crisis is taking a rising toll on the region’s industrial capacity with another zinc smelter going into care and maintenance.

Glencore is curtailing production at its Nordenham plant in Germany citing “various external factors affecting the business and wider European industry.”

It’s the third West European zinc smelter to close over the last year as operators struggle to cope with surging power prices.

Smelting has turned out to be the weakest link in the global zinc supply chain this year, creating pockets of extreme tightness in the physical market.

The rolling supply woes contrast with an increasingly negative demand picture and the bear-bull tension is manifest in continued price and time-spread volatility on the London Metal Exchange (LME) contract as traders try and work out whether supply or demand is falling faster.

The LME’s overnight move to limit the deliverability of Russian zinc won’t have much impact on physical supply but a near 5% jump in the zinc price to $3,193 per tonne is a sign of the collective uncertainty.

European shutdowns

The Nordenham smelter, which produces around 165,000 tonnes per year of refined zinc and alloy, will be shuttered from the start of next month.

Glencore mothballed its Portovesme smelter in Italy at the end of last year and Nyrstar closed its Budel plant in the Netherlands last month.

Other plants are adjusting run rates to avoid peak power pricing periods as the entire European smelter sector fights a ferocious margin squeeze.

Europe was already on track to lose 234,000 tonnes of refined zinc production this year before the latest closure, according to analysts at Macquarie Bank. (“Commodities Compendium”, Sept. 29, 2022)

The smelter crisis is unlikely to abate until Europe gets on top of its energy problems and manages the flow-through consequences on its metals producers.

The growing number of hits to Europe’s industrial ecosystem has propelled the metals sector up the list of policy-maker priorities but it’s a long list.

Global woes, Russian sanctions

Macquarie estimates another 240,000 tonnes of zinc production has been lost outside of Europe this year due to a combination of technical problems at some Western plants and power constraints on Chinese smelters.

The International Lead and Zinc Study Group calculates a 2.4% slide in global refined zinc output over the first seven months of the year.

The market is super-sensitive to supply-side headlines right now, hence the knee-jerk reaction to the LME’s announcement it is limiting the deliverability of Russian zinc.

This comes in response to an extension of British sanctions on Iskander Makhmudov, thought to be the ultimate owner of Russian zinc and copper producer UMMC, albeit one obscured by a series of holding companies.

The exchange won’t accept any deliveries of UMMC’s “CZP SHG” zinc brand unless it was sold before Sept. 26, when the British government announced sanctions, or unless the owner can prove that UMMC has “no right of ownership and/or other economic interests in respect of the metal”.

There is no Russian zinc in the LME’s warehouse system at the moment and exports have almost dried up since a fire at the Chelyabinsk smelter in 2018. The plant was permanently closed with UMMC planning to shift production to other smelters in the Urals.

However, Russian exports of unwrought zinc have slid from over 40,000 tonnes in 2017 and 2018 to just 622 tonnes in 2021, according to the International Trade Center.

That suggests much-reduced export capacity and the latest sanctions will likely have far more resonance in the copper market than in zinc.

Pricing tension

But zinc is still caught in the conundrum of pricing a global downturn in metals usage simultaneously and accumulating refined metal losses.

Most analysts think the combined demand hit from China’s faltering property sector and a looming, energy-driven recession in Europe will outweigh the growing toll of European smelter closures.

Macquarie is forecasting the LME cash price to fall from an average $3,647 per tonne in 2022 to an average $2,725 next year as macro gloom overwhelms micro dynamics.

Citi agrees, saying it expects zinc to fall to $2,500 per tonne by early next year as the manufacturing slowdown crushes demand. (“Global Commodities Quarterly”, Oct. 4, 2022)

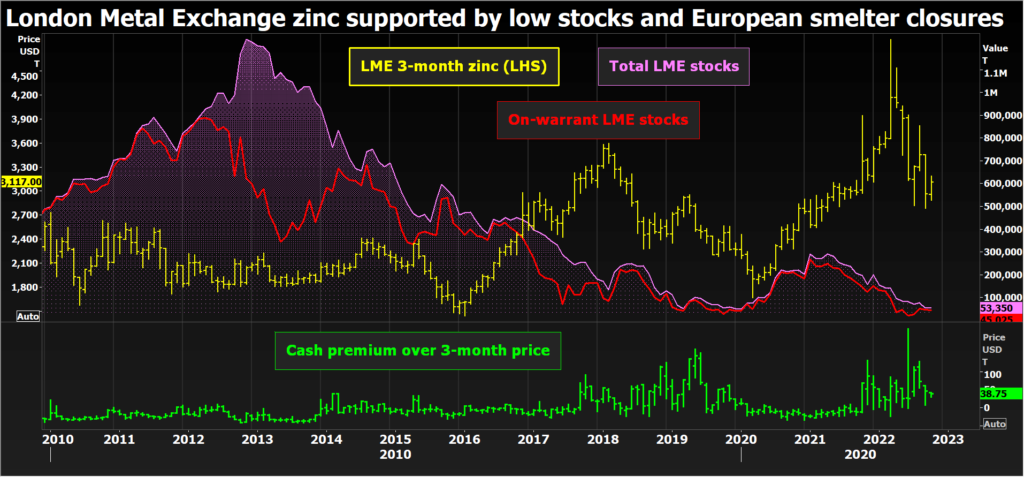

The nagging problem with the bear narrative is the depleted state of exchange inventories which is generating time-spread tightness on both the LME and Shanghai exchanges.

LME registered stocks are at a multi-year low of 53,325 tonnes, now down by 146,000 tonnes on the start of January. Shanghai Futures Exchange (ShFE) inventory stands at 37,694 tonnes, the lowest it’s been since July 2021.

The LME’s benchmark cash-to-three-months spread has been in backwardation since the start of June, the cash premium valued at $29.50 per tonne at the Wednesday close.

Although there is certainly more zinc sitting in the off-market statistical shadows, owners can achieve a premium of over $500 per tonne by selling it to a European physical buyer rather than delivering it to an LME warehouse.

Fastmarkets has just lifted its mid-point assessment of North European premiums to a new all-time high of $525 per tonne over LME cash in the wake of the Nordenham news.

Premiums should be falling as high energy prices chill European demand but the mounting loss of production from smelter closures is clearly still working against physical buyers.

Until physical premiums loosen, it’s hard to see how there’s going to be a significant rebuild in exchange inventory that would complement the broader bear narrative.

The latest European smelter closure simply adds to the tension between a decidedly bearish macro picture and zinc’s supply problems that are preventing a rebuild in stocks.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by David Evans)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments