Column: The bulls are back in charge of iron ore prices

Iron ore prices are gathering steam as confidence over the outlook for China’s steel demand increases, outweighing bearish factors such as potential winter production curbs and India lowering iron ore export taxes.

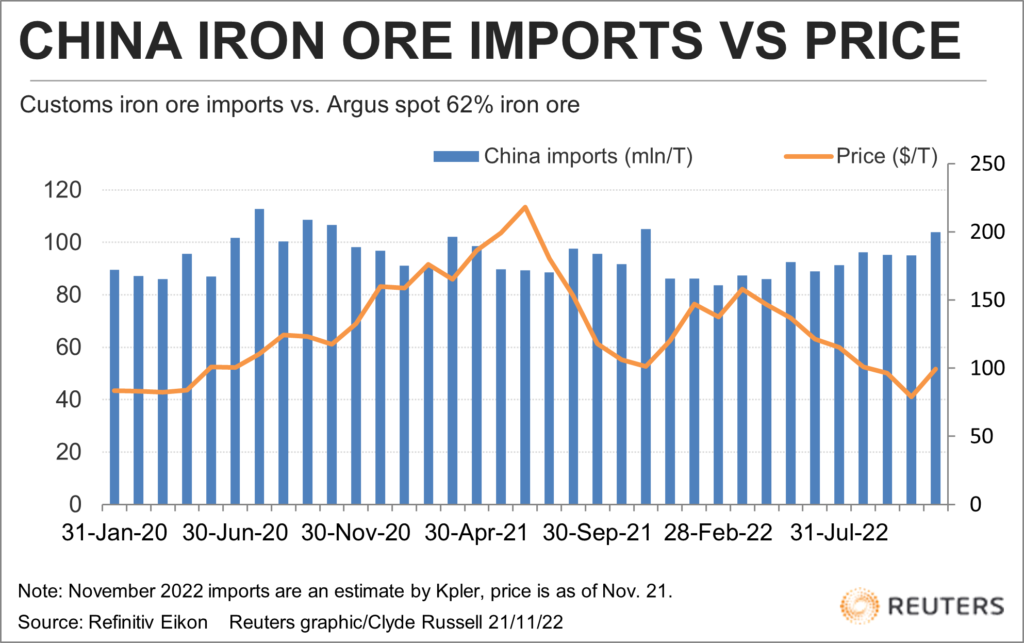

The price of spot 62% iron ore for delivery to north China, as assessed by commodity price reporting agency Argus, rose to $99.50 a tonne on Nov. 18, close to the $100 level last seen on Sept. 15.

The price has gained 26% since hitting a three-year low of $79 a tonne on Oct. 31, taking heart from China’s efforts to stimulate the world’s second-biggest economy and ease some of the strict covid-19 containment measures that have hamstrung growth this year.

In addition to optimism that steel-intensive sectors such as construction and infrastructure will accelerate next year, there are some other bullish factors for iron ore and steel.

Iron ore inventories at Chinese ports dropped to 135.45 million tonnes in the week to Nov. 18 from 136 million the previous week.

More importantly, inventories are almost 10% below the level that prevailed at this time last year.

It’s also worth noting that inventories usually build heading into the northern winter as steel mills accumulate stock to boost production in the new year, when construction activity picks up.

Steel rebar inventories are also declining, slipping to 3.74 million tonnes in the week to Nov. 18.

Rebar stockpiles typically drop heading into winter and build early in the new year to meet expected higher demand.

The current level of rebar inventories is also low for this time of year, being 23% below the 4.85 million tonnes in the same week last year, and the 4.88 million at this point in 2020.

The depleted inventory levels suggest that China, which buys about 70% of global seaborne iron ore, has scope to lift imports in the coming months.

Iron ore imports

November is shaping up to be a strong month for iron ore arrivals, with commodity analysts Kpler estimating seaborne imports of 103.9 million tonnes, while Refinitiv estimates a higher 106 million tonnes.

Both figures are substantially higher than the official customs figure of 94.98 million tonnes for October, and if imports do exceed 100 million this month, it would be the strongest outcome since November 2021.

There are some factors that may weigh on iron ore prices, the main one being the poor profitability of China’s steel mills, which may lead to lower output, especially during the early part of winter.

Steel production curbs may also be imposed by authorities as part of measures to control pollution, which could limit iron ore demand in the short term.

India may also start exporting more iron ore cargoes after the government scrapped some taxes, especially those on lower-grade material.

India is not a major player in the seaborne iron ore market, with its exports dwarfed by those from Australia and Brazil, but in 2020 it supplied an average of 4 million tonnes a month, according to Kpler data, with China the major buyer.

It is unlikely India will be able to export at its 2020 rate any time soon, given it takes time to re-establish trading relationships and restore supply chains.

Even if India does manage to resume exports, it’s likely to have only a limited impact on prices for lower grades of iron ore, such as 58% and below.

Overall, for now the bullish factors in China are driving the price of iron ore. The problem is that these factors are still largely sentiment-based and won’t become apparent in the real world until the beginning of 2023.

(The opinions expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

(Editing by Robert Birsel)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments