Column: LME volumes still subdued a year after nickel crisis

A year on from the nickel crisis the London Metal Exchange (LME) is still struggling to regain trading momentum.

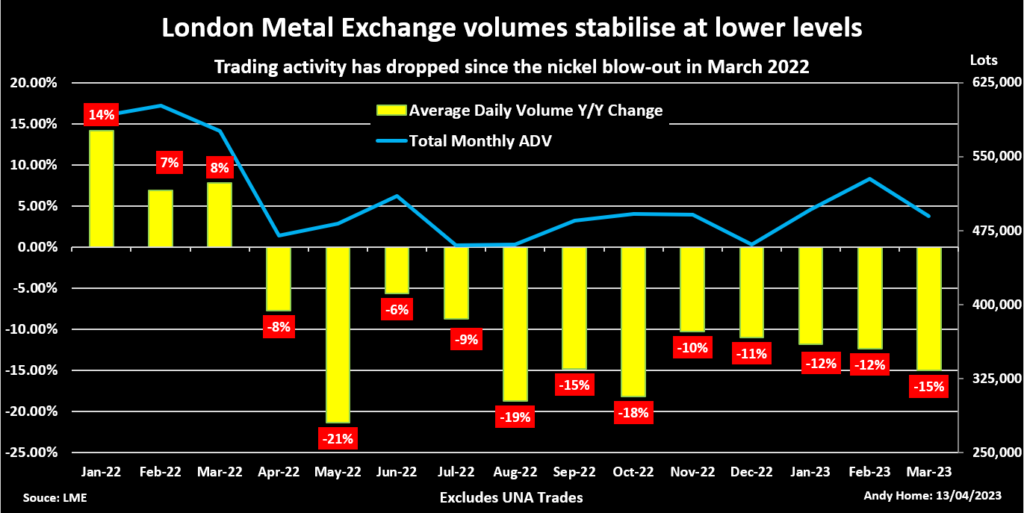

Volumes dropped sharply after the controversial decision to suspend nickel trading and cancel trades. They have stabilized over recent months but at a lower level than before the market meltdown in March 2022.

The LME is hoping that the resumption of nickel trading in Asian hours will help revitalize its floundering contract and is pressing on with a broader reform package to restore confidence in the 146-year-old industrial metals market.

The drop in activity has not been helped by a broader lack of investor enthusiasm for base metals in the current macroeconomic environment.

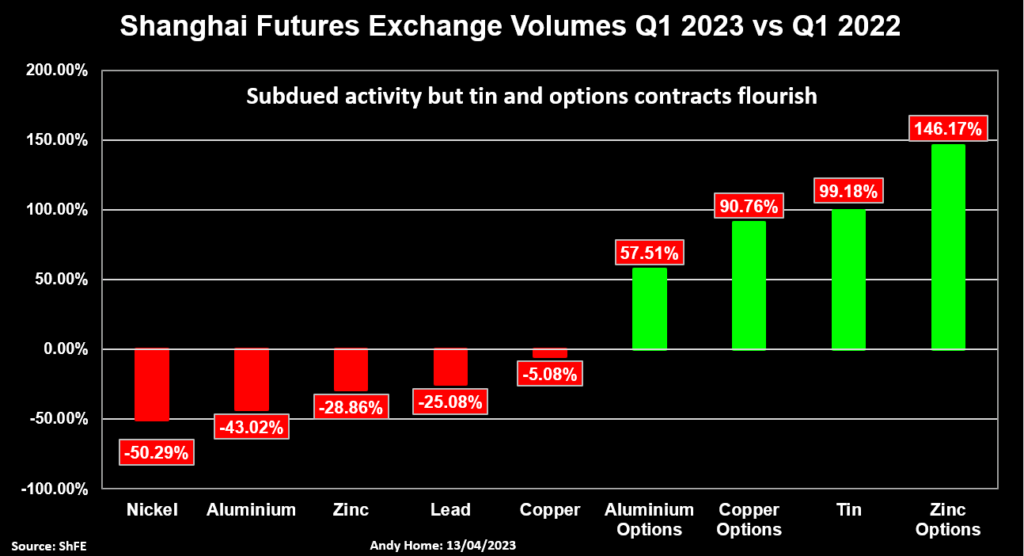

The Shanghai Futures Exchange (ShFE) also saw activity fall across most of its base metals suite in the first quarter, dampening the arbitrage opportunities with London.

In this subdued metals trading landscape there are currently two unlikely star performers: London lead and Shanghai tin.

Lost momentum

Average daily volumes on the LME, which is owned by Hong Kong Exchanges and Clearing, were down by 15% year-on-year in March and by 14% over the first three months of the year.

These comparisons are with the last months of trading before the nickel blow-up and the ensuing flight of many investment players from the market.

The headlines will look a lot kinder to the LME over the coming months since the baseline will be the lower trading activity environment that followed the six-day suspension of nickel trading.

However, average daily volumes in the year since have been running consistently around 13% lower than in the 12 months up to March 2022.

No surprise that nickel itself is still the under-performer of the LME’s core base metals portfolio.

Outright futures and options volumes were 53% lower in the first quarter than the same period last year, albeit with a slight uptick in March itself, which may reflect the restart at the end of the month of Asian-hours trading.

But LME zinc and aluminum also registered sharp volume declines of 19% and 17% respectively in the January-March quarter. Copper activity rose by 10% but was flat year-on-year in March itself.

Shanghai subdued, CME expands

The year started with great expectations of the demand boost from China’s full reopening after last year’s rolling lockdowns.

The reality has so far under-whelmed metals bulls, not least in China itself, where base metals seem to be out of favour with speculative players.

The Shanghai nickel contract took a big collateral hit from the LME’s crisis and volumes remain depressed, down by half year-on-year in the first quarter.

But as with the LME, Shanghai zinc and aluminum volumes also contracted sharply by 29% and 43% respectively, while copper fell by a more modest 5% on the first quarter of 2022.

The ShFE options contracts bucked the softer trend, those for aluminum, copper and zinc all registering strong year-on-year growth.

Options trading on the CME’s copper contract has also been booming, volumes on the vanilla contract surging by 156% in the first quarter and the newer weekly and event option contracts also gaining traction.

The CME’s aluminum contract has registered spectacular growth, volumes jumping to 198,000 contracts in the first quarter from 33,000 a year ago. Liquidity has been helped by rising stocks in CME-registered warehouses, registered inventory up by 50% on the start of the year at 28,842 tonnes.

That is still low by comparison with LME inventory of 530,350 tonnes and the CME contract is still a minnow relative to its London peer, which traded 12.8 million lots in the first quarter.

But the CME’s growth trajectory combined with its physical premium products suggest a structural shift in aluminum trading dynamics is underway.

Lead gets index booster

The two metallic stand-outs in terms of first-quarter trading activity were LME lead and ShFE tin.

London lead futures and options volumes grew by 21% year-on-year with activity exceeding the one-million-lot level in both January and March for the first time since early 2020.

The increased action coincides with lead’s inclusion from January in the Bloomberg Commodity Index (BCOM), putting the battery metal firmly on the broader investment radar.

The BCOM and its multiple look-alikes are passive investment instruments, requiring long positions in the underlying commodities in proportion to their index weighting.

That for lead is just 0.936%, lower than any other industrial metal, but still enough to boost activity in a contract that doesn’t normally attract much investor interest.

Shanghai tin boom

Tin is too small a metallic market to make it onto the Bloomberg or any other commodity index.

But it seems to be garnering a lot of attention from Chinese players. Volumes in the ShFE tin contract doubled in the first three months of the year in stark contrast to the subdued performance across the rest of the base metals pack.

March turnover totalled 5.34 million lots, the highest monthly volume since the contract was launched in 2015. With one Shanghai lot representing one tonne of metal, volumes last month were 14 times greater than last year’s global production of 380,000 tonnes.

True, ShFE tin stocks nearly doubled over the course of the first quarter but at 8,639 tonnes at the end of March any associated futures positions would still have been only a fraction of what has traded this year.

Indeed, the recent pattern of rising open interest into price declines suggests it is the bears who are in the ascendancy in the Shanghai tin market.

The LME’s tin contract has been a beneficiary, volumes rising 5% in the first quarter.

It may be a sign that the LME’s hopes of recovering lost momentum rest at least partly on a return of China’s army of speculators.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Emelia Sithole-Matarise)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments