Column: LME aluminum stocks battle comes with a Russian twist

There was another raid on London Metal Exchange (LME) aluminum stocks last week.

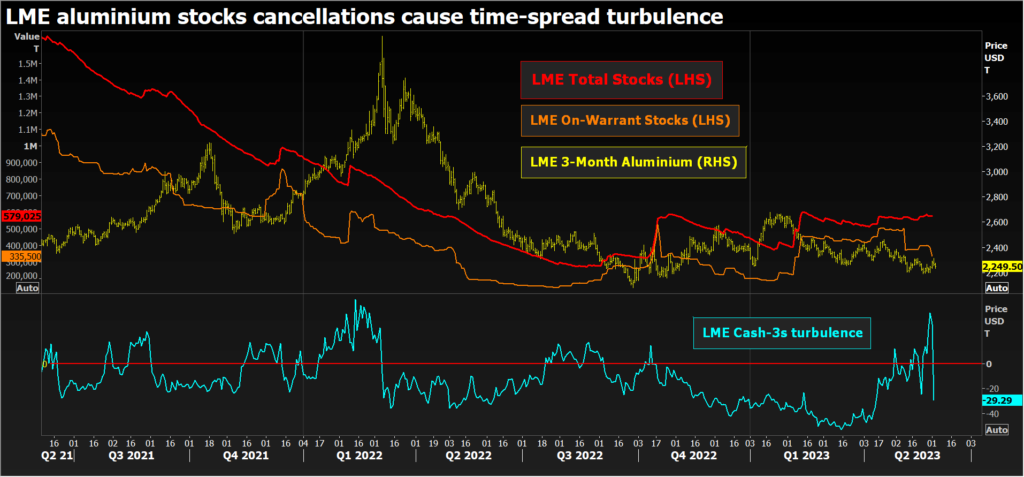

While headline inventory fell by a marginal 1,475 tonnes over the holiday-shortened week, available stocks slumped by 19% thanks to 83,875 tonnes of net cancellations.

It was the second swoop on exchange stocks of aluminum in the space of a month after the mass cancellation of 132,700 tonnes of metal on May 10. LME on-warrant stocks have fallen from over 500,000 tonnes in the middle of April to a four-month low of 324,650 tonnes.

LME time-spreads have been turbulent, the benchmark cash-to-three-months period flexing out to a backwardation of $42 per tonne on Thursday before snapping back to a contango of $29 at the Friday close.

Aluminum trading in London has long been characterized by such bouts of volatility as powerful traders battle it out across visible inventory and time-spreads.

But this time around the turbulence comes with a distinctly Russian twist.

Rising Russian stocks

The amount of Russian aluminum in the LME warehouse network has grown significantly over recent months as many Western users self-sanction by opting for other suppliers.

Russian-brand aluminum stocks totalled 256,125 tonnes at the end of April, accounting for just over half of the LME’s non-cancelled tonnage at the time.

The figure has grown from 93,750 tonnes at the end of January and 49,225 tonnes at the end of March 2022, when the LME figures covered all Eastern European brands.

It’s not the first time that Russian metal has washed through the LME warehousing system but the scale of the recent build relative to the more modest increase in overall LME inventory suggests less market surplus than specific problems marketing Russian metal.

The task became a lot harder after the United States imposed penal import duties of 200% on Russian aluminum in March.

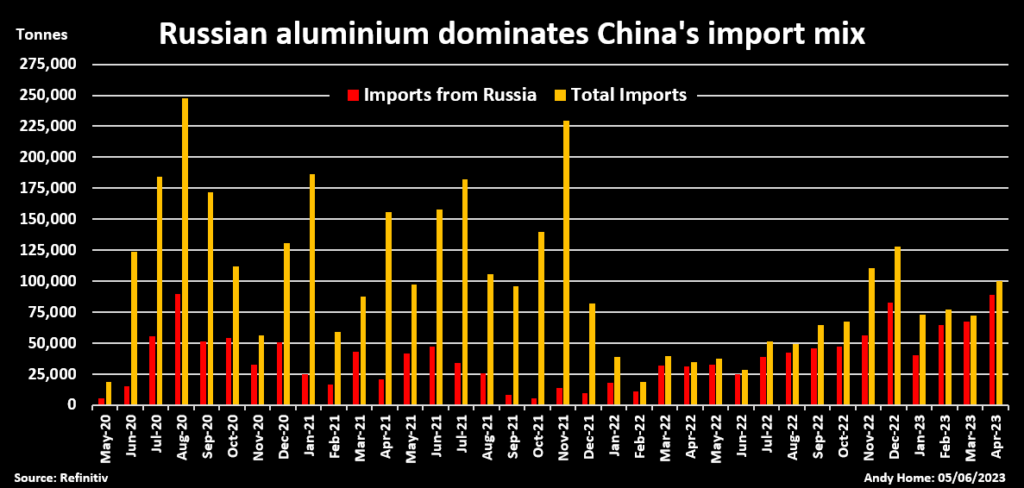

Some Russian metal has been displaced into China.

China imported 261,000 tonnes of Russian aluminum in the first four months of this year, accounting for a dominant 81% of total inbound shipments.

However, it is clear that some of Russia’s four million tonnes of annual production has made its way to the market of last resort.

Stocks battle

LME on-warrant stocks at the end of April largely comprised Russian and Indian brands, representing 52% and 47% of the total respectively.

Most of the LME stock was located at the South Korean port of Gwangyang and Malaysia’s Port Klang, a distribution which hasn’t changed much in the interim.

It’s been widely reported that the flow of metal into Gwangyang, a previously little-used storage point for aluminum, has been down to the warranting of Russian metal by Glencore, which has a long-term off-take agreement with Russia’s Rusal.

The Indian metal, by contrast, has largely flowed into Port Klang, a long-standing hub for surplus aluminum.

It’s noticeable that most of the recent cancellation activity has been at Port Klang, where on-warrant stocks have dwindled to 50,975 tonnes, the lowest level since 2015, and cancelled stocks have grown to 222,000 tonnes.

Gwangyang, by contrast, has seen only a modest 17,175 tonnes of net cancellations since the start of May and currently holds 229,825 tonnes of on-warrant stocks, accounting for 69% of the total live tonnage in the LME warehouse system.

The hits on Port Klang but not on Gwangyang suggest heightened competition for non-Russian brands of aluminum.

It’s by no means certain that the metal cancelled will be loaded out for physical delivery but it’s very clear that someone didn’t want someone else to have the remaining non-Russian metal.

Turbulence ahead?

The aluminum battle has abated judging by the collapse of time-spreads since Friday.

The outright aluminum price has been little affected by the gyrating front part of the curve. Three-month metal, currently trading at $2,250, is still ensconced in its recent $2,200-2,300 range.

However, the calm may not last for long.

Aluminum’s supply-demand picture has deteriorated this year, largely due to an underwhelming post-lockdown recovery in China’s manufacturing sector.

More surplus metal, both Russian and Indian, is likely to hit the LME in coming weeks, setting the stage for more clashes between trading houses over who gets which brands.

This is also a headache for the LME itself.

The exchange decided last year against stopping fresh inflows of Russian metal, arguing that the metal remains officially unsanctioned and many consumers, particularly Asian, intend to carry on using it.

The LME can take some heart from the fact that almost 60,000 tonnes of aluminum in Gwangyang have been cancelled and physically loaded out since the start of this year.

But LME-registered inventory at the Korean port has still mushroomed from just 24,025 tonnes at the start of 2023 to 235,850 tonnes and it now accounts for most of the live stocks.

The danger is that the LME aluminum contract becomes a de-facto Russian metal contract trading at a discount to the non-Russian market.

It’s not happened yet but the latest LME stocks tussle suggests an evolving differentiation between Russian and non-Russian components of the visible inventory picture.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Sharon Singleton)

More News

Manganese X poised to begin pre-feasibility study at Battery Hill

April 11, 2025 | 02:39 pm

Carbon removal technologies could create tens of thousands of US mining and quarry jobs – report

April 11, 2025 | 01:33 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments