Column: Iron ore’s price bounce may be based on more than just China hopes

The price of spot iron ore for delivery to north China has rallied from a two-year low as some optimism creeps back into the market that the worst may be over for the steel raw material.

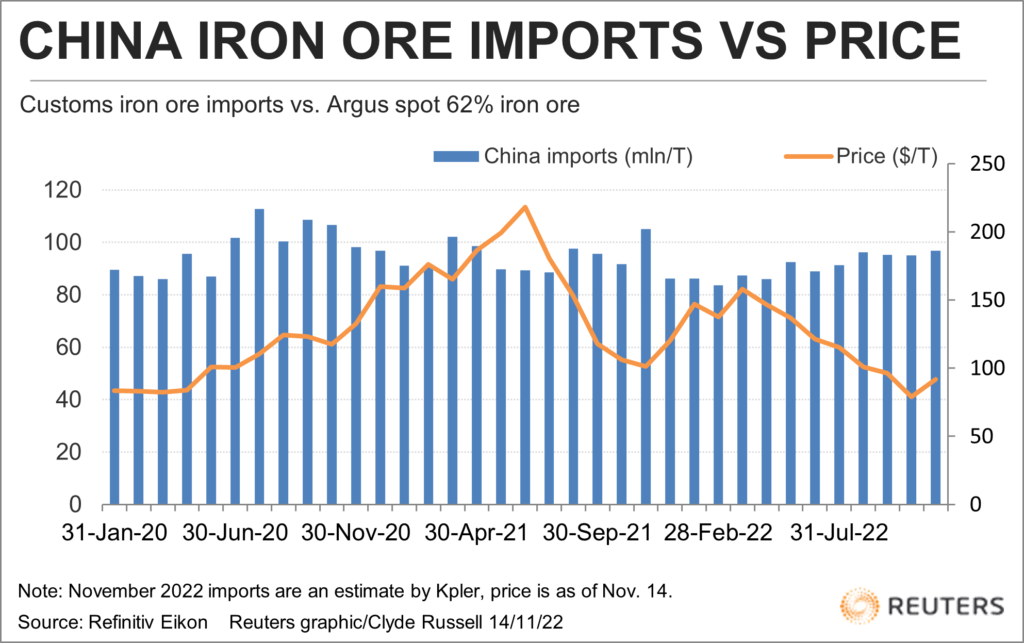

The spot price of benchmark 62% iron ore, as assessed by commodity price reporting agency Argus, ended at $91.75 a tonne on Nov. 11, up 16% from a three-year low of $79 on Oct. 31.

However, iron ore is still down 43% from its peak in 2022 of $160.30 a tonne, reached on March 8 in the aftermath of Russia’s Feb. 24 invasion of Ukraine, which raised fears of a loss of supply from Ukraine, which had been the world’s fifth-largest exporter.

While supply concerns have eased, the main dynamic behind the price retreat has been weakness in the residential construction sector in China, which takes about 70% of iron ore that is exported by sea.

China’s real estate investment was 8.0% lower in the first nine months of the year than a year earlier, while property sales by floor area declined by 22.2% in the same period, according to official data released on Oct. 24.

Given that construction accounts for more than a third of China’s total steel demand, the ongoing weakness in residential property has been a cloud over iron ore’s outlook.

But there are some signs that Beijing’s stimulus efforts are starting to bear fruit, with policy changes making it easier and cheaper for first-time home buyers to access loans.

Some changes to China’s strict zero-covid policies may also boost market sentiment and confidence among potential home buyers, event though the country is battling several new outbreaks of the coronavirus.

But it’s also likely that iron ore’s recent rally is still largely built around changes in market sentiment, rather than actual changes in steel demand.

China’s total iron ore imports, including very small volumes arriving by rail from neighbouring countries, fell 4.7% in October from the previous month, dropping to 94.98 million tonnes, with arrivals for the first 10 months of the year down 1.7% from the same period in 2021.

A recovery may be on the cards in November, with commodity analysts Kpler estimating that seaborne iron ore imports will be around 96.87 million tonnes.

But the overall message from iron ore imports this year is that they will likely be slightly lower in 2022 than last year.

Stimulus, covid

The hope is that the stimulus measures and a more relaxed covid-19 stance result in a strong start to 2023, and certainly steel mills appear to be increasing production in anticipation of improving demand.

China’s steel output rose to a three-month high in September of 86.95 million tonnes, which was up 3.7% from August’s 83.87 million, according to official data released on Oct. 24.

However, for the first nine months of the year, steel production was down 3.4% from the same period in 2021, pointing to a likely small contraction for the year as a whole.

The question for the market is whether there are any actual bright spots for steel demand, and thus iron ore imports in China, or whether it is all just hope that stimulus measures finally start to work in the new year.

While the market tends to focus on weakness in residential property construction, total construction has been holding up far better.

A recent presentation by Will Millsteed, Rio Tinto’s head of market analysis, showed that China’s total new starts by floor space was only just in negative territory for the first nine months of the year.

This is because floor starts by non-developers had been up more than 30% in the first nine months, almost offsetting the decline in starts by property developers.

“Buildings that are not constructed by developers consists of social housing, factory, warehouse, hospitals, schools, social wellbeing facilities, hotels, etc. Non-developers account for about 60% of overall building construction,” the presentation said.

Strong electric vehicle sales have also helped keep auto sales in positive territory for the year to date, which in turn boosts steel demand, while infrastructure spending is also holding up.

Overall, the picture for steel demand outside of residential property is resilient, and if the outlook for the housing sector is improving, it could be a bullish signal for China’s iron ore imports in coming months.

(The opinions expressed here are those of the author, Clyde Russell, a columnist for Reuters.)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments