Column: Funds sell copper as technical picture deteriorates

Fund managers are taking an increasingly bearish view of copper’s short-term prospects as the price tests the lower band of its year-to-date trading range.

London Metal Exchange (LME) three-month copper has this week broken down through the $8,000-per metric ton level for the first time in five months in tandem with a collapsing time-spread structure.

Last trading at $7,990 per metric ton, London copper is now within sight of the year-to-date lows of $7,867-7,871 recorded in late May.

Investors on both sides of the Atlantic have been shifting positions in response to a potential downside break of a range that has defined the price action this year.

Bears flex muscles on CME

Fund positioning on the CME copper contract has oscillated between long and short for several months as the price chopped around in a sideways range.

But the collective stance has turned more bearish since the start of September with money managers lifting outright short positions to 77,276 contracts in the week to Sept. 26.

It’s the largest accumulation of bear bets since March 2020, when copper and the rest of the base metals complex were reeling from the first impact of Covid-19 restrictions.

Fresh fund selling has shifted net positioning to the short side to the tune of 21,220 contracts, the most bearish reading since June when the collective net short flexed out to 23,012 contracts.

Bulls are still hanging on in there. Indeed outright long positioning actually rose by 1,339 contracts on the week, attesting to the continued wide spectrum of views on copper’s short-term dynamics.

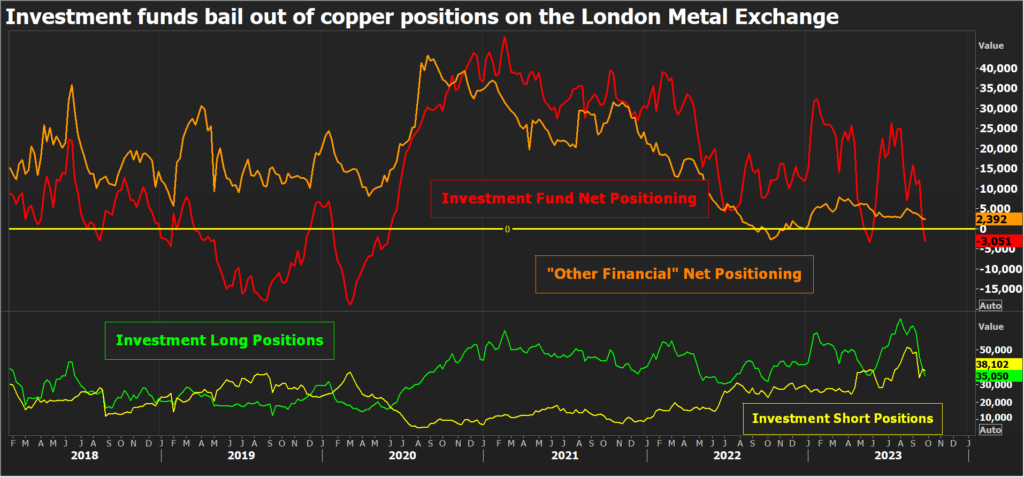

Bulls throw in the towel in London

Investment fund positioning has also shifted to the short side on the London copper market for the first time since early June.

Here it’s a case of investors sharply reducing their long exposure. Outright long copper positions have been slashed from 63,665 contracts at the start of September to 35,050 as of the Sept. 26 close.

Funds have also reduced their short exposure, albeit less dramatically. The last two weeks have seen a margin net rebuild but nowhere near to the extent seen in the US market.

Net positioning has shifted to a collective short of 3,051 contracts, just shy of the 3,228-contract peak 2023 short in June.

It’s worth noting that the “other financial” reporting category, which includes index funds, is still in modest net long territory.

Technicals rule OK?

There are good reasons for investors to be wary of a potential bear break-out from this year’s previously price-defining trading range.

China’s piece-meal stimulus remains underwhelming, even as Europe’s manufacturing sector contracts and concern grows about economic momentum in the United States. A strong dollar and a weak yuan are also piling pressure on the copper price.

Copper’s micro dynamics are compounding the sense of impending gloom. LME time-spreads have collapsed, the cash discount to three-month metal widening to $77.50 per metric ton at Tuesday’s close, the largest discount since the early 1990s.

Low liquidity may have accentuated the move but heavy cash selling in recent days is a warning signal that more copper could be about to hit the LME warehouse system.

LME copper stocks rose by 65,025 metric tons over the course of September, the largest monthly increase since April 2022, and spreads are saying there may be a lot more metal sitting in the warehouse shadows.

But copper’s deteriorating chart picture holds the clue to the market’s immediate prospects, particularly given the number of black-box funds that are configured to react to momentum and technical triggers.

Focus is now on those May lows and whether they will provide sufficient support to hold back the building bear pressure.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Alexandra Hudson)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments