Column: Copper views Trump win through Chinese lens

Donald Trump’s US presidential election win has not sparked a repeat of the explosive copper rally which followed his unexpected victory in 2016.

That coincided with a market that was heavily short of both futures and options and triggered a mass realignment of fund positioning.

This time, copper was in risk-off mode ahead of what seemed a close-call result. Fund managers were net long of copper ahead of last week’s election, but only modestly so.

Moreover, the market focus was as much on China as it was on the US as the other big event last week was the meeting of China’s National Peoples Congress (NPC) Standing Committee.

The resulting $1.4 trillion package to ease local government’s “hidden debt” burden disappointed metal bulls looking for something much stronger from China’s cabinet.

As far as Doctor Copper is concerned, the main question around a second Trump presidency is whether the threat of tariffs will spur China to do more to fire up its sputtering growth engine.

Election week wobbles

Copper’s price reaction to the US elections was revealing in what it said about the market’s real focus, namely China.

London Metal Exchange three-month copper slid by 4.1% on Wednesday in what looked like a knee-jerk reaction to US dollar strength in the wake of the election results.

By the close of Thursday, copper had clawed back almost all its losses as traders bet the Trump tariff threat to Chinese exports would encourage the NPC Standing Committee to open up the stimulus taps.

Friday’s announcement of what is in essence a debt swap between central and local governments dashed bullish expectations and triggered a renewed sell-off.

Copper closed Friday at $9,443.50 per metric ton, representing a weekly loss of 1.3%. Although trading was volatile, the net weekly change was small and a far cry from the turbulence of 2016.

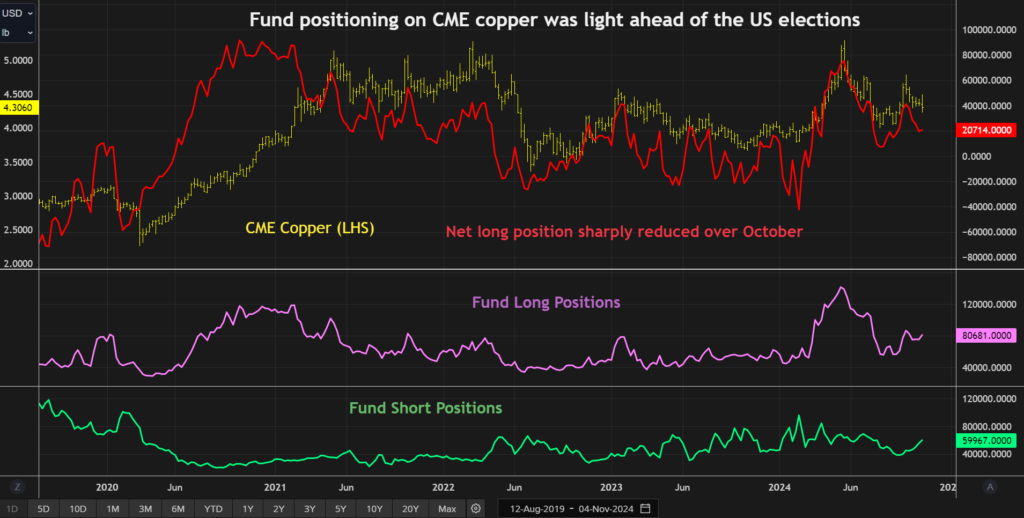

Fund positioning was much lighter this time ahead of an election that looked too close to call. Money mangers held a modest net long position of 20,714 contracts on the CME copper contract as of the close of Nov. 5. That had been sharply reduced from 41,127 contracts at the start of October.

Tariff turbulence

Copper is clearly unsure how to price in the bearish prospect of Trump’s promised 60% tariffs on Chinese goods and the potential bullish offset of more urgent stimulus from Beijing.

Tariffs, which are still several months away, are unlikely to make much difference to direct flows of metal from China to the United States.

The Biden administration has already tripled import duties to 25% on imports of Chinese aluminum and steel products in response to China’s growing exports.

Canada has done the same and imports from Mexico, which has been accused of being a transshipment point for Chinese metal, must now come with a certificate of analysis proving non-Chinese origin.

The bigger question is the potential impact on the broader Chinese economy, which looks a lot more vulnerable to a US trade war than was the case eight years ago.

Which is why copper’s immediate response to the US election result was to look for a reaction from Beijing.

What it got was a debt tidy-up, which although positive is unlikely to move the growth dial in the short term.

The US election may have provided some brief distraction but copper’s gaze has fully returned to the world’s largest metals user.

Metal bulls are hoping that a change of administration in Washington will provoke a change of stimulus policy in Beijing.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Alexander Smith)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments