Column: Copper today, aluminum tomorrow? LME’s Russian dilemma

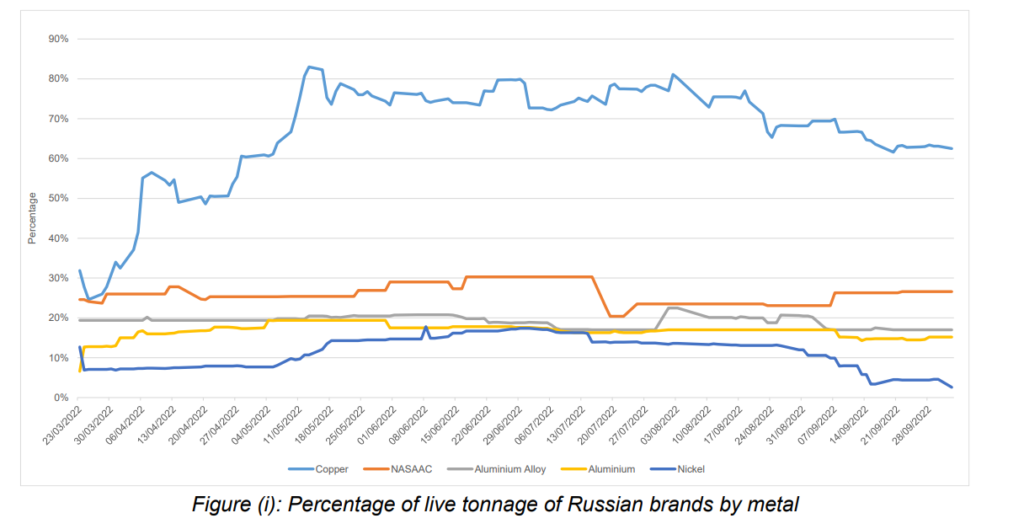

More than 60% of the copper stored in London Metal Exchange (LME) warehouses at the end of September was produced in Russia.

The proportion of Russian metal surged from below 30% in late March to above 80% in May and August in the wake of Moscow’s “special military operation” in Ukraine.

Such a high ratio is not unprecedented and continued stock cancellations and drawdowns suggest many buyers are accepting it against 2022 contracts in the absence of official sanctions.

But what if that changes? Annual supply contracts are in the process of being negotiated and at least some buyers are “self-sanctioning” by specifying no Russian metal in 2023.

Large amounts of unsold Russian metal, particularly aluminum, could hit the market of last resort and the LME is sufficiently concerned that it has issued a discussion paper on whether to suspend all deliveries.

Copper flows

The proportion of Russian copper in LME stocks was actually higher in the third quarter of 2021, when it reached 95% of live tonnage, LME data shows.

However, the sharp increase since March is striking, particularly since stocks of Russian aluminum and nickel have been low and little changed over the same period.

Two of the most active LME copper stock locations this year have been Hamburg and Rotterdam, handily located for Russian shipping lines. The two ports have received a combined 100,000 tonnes of copper since the start of March, almost a third of the total inflow.

What has come into LME sheds has largely turned around and departed. Hamburg copper stocks, for example, are up by only 6,800 tonnes at the start of January, despite almost 50,000 tonnes of inflow.

Until last month Russian copper had escaped the official sanctions net, meaning users could legally continue accepting it against contracts for “LME deliverable” metal.

However, the British government announced in September sanctions and an asset freeze on Iskander Makhmudov, the controlling shareholder of UMMC, one of Russia’s two dominant copper producers, according to the LME, which has severely restricted the ability to warrant either of UMMC’s two brands.

With just Nornickel still fully unsanctioned, the amount of potentially deliverable Russian copper is sharply reduced.

Moreover, there is an obvious destination for any unsold Russian copper next year. China remains a hungry commercial and strategic buyer and is likely to snap up what others do not want, particularly if it comes with a good price tag.

Aluminum threat

The same cannot be said for aluminum. China is by some margin the world’s largest producer and a big net exporter.

True, power rationing has constrained China’s output in the last couple of years and the country imported significant amounts of primary aluminum in 2020 and 2021.

But domestic market dynamics have shifted again this year and imports dropped by 71% to 298,000 tonnes in January-August from 1.03 million tonnes in the same period of 2021.

With Chinese banks wary of financing Russian material, the country is unlikely to be able to absorb Rusal’s four million tonnes of annual production for any sustained period of time.

It’s no coincidence that the issue of Russian deliverability has shot up the LME’s agenda since an aluminum industry meeting in Barcelona, where the talk was of who is, and more importantly is not, going to accept Russian metal in their 2023 contracts.

Rusal has just announced a sales management reshuffle and says its order book is “solid and the company has no need to deliver metal to LME warehouses.”

Pricing problem

Rusal, which has emerged as a major supplier of “green” aluminum, cautions that suspending its brands in the current low-stocks environment would create increased price and physical premium volatility.

It would also hard-wire a discount into the price of Russian metal relative to the LME price, creating an unpredictable ripple effect along a physical supply chain that prices basis exchange-deliverable brands.

The flip side is that if there were an influx of Russian aluminum, copper, or nickel into LME warehouses due to a lack of buyers, the LME contract would price the discount.

Such a scenario “could threaten the orderly nature of the LME’s markets, and in particular its key role in price discovery for the global physical industry,” the LME noted.

But then so too would suspending Russian metal ahead of official sanctions, which is the dilemma now facing the LME.

“A failure to take action now could mean that the LME’s hands are tied in the future when any move to address the situation could be undermined by the volume of Russian metal already on a warrant,” it said.

The plan is to ask the market for feedback in parallel with the annual negotiations for next year’s supply contracts.

The three options are to do nothing, set thresholds for Russian metal deliveries or suspend all warranting across all locations. Thresholds are probably too complex, the LME concedes, leaving a binary choice, albeit with another subset of questions as to how much notice should precede a suspension.

Dilemma

Asking the market is a good idea since it will be the degree of “self-sanctioning” that determines whether there will be a surplus of unsold Russian metal in the first place.

Getting a consensus could be much trickier, since there is evidently a lot of self-interest on both sides, particularly in aluminum, where Western producers and Rusal have clashed before over changes to LME warehouse load-out rules.

Rusal’s court challenge at the time is a reminder that any unilateral LME move may also be legally fraught.

Moreover, the metals debate could be changed at any time by the initiation of government sanctions such as just imposed by Britain on UMMC’s owner or the European Union’s April ban on Russian lead imports.

Unfortunately for the LME, the question mark over future sanctions on Russian metal simply underlines the dilemma of whether to go early or risk going too late.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Alexander Smith)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments