Column: Analysts wary of base metals after China recovery rally

Base metals have enjoyed a strong start to the year, the London Metal Exchange (LME) index rising by 9.4% over the course of January on high hopes for China’s post-covid reopening.

However, analysts are cautious that China’s recovery may not live up to bullish expectations and that prices have got ahead of themselves, judging by the latest Reuters base metals poll.

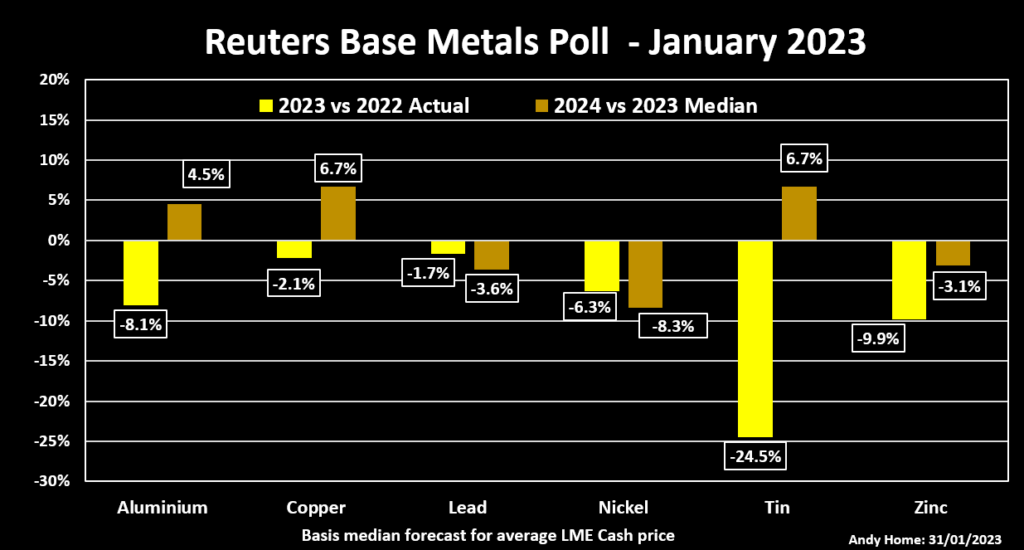

Median 2023 price forecasts for all the core LME base metals are lower than both last year’s price and current trading levels.

Depleted exchange inventories are seen limiting the immediate price downside but analysts are also expecting supply to recover from the combination of pandemic disruption and high power prices.

Supply will be a key differentiator next year, with copper, aluminum and tin outperforming nickel, lead and zinc.

Doctor Copper bets on China

Copper is back in favour with investors, who have been building long positions in the metal as one component of the broader China recovery trade.

The LME copper cash settlement price was $9,075 per tonne on Tuesday, up 10% on the start of January.

Many think it’s already over-priced. The median forecast of 31 analysts is for cash copper to fall back to an average of $8,250 per tonne in the second quarter before recovering to $8,750 in the fourth quarter.

A median forecast of $8,625 for the full year is 2.1% lower than last year’s average of $8,814 per tonne.

[Click here for an interactive chart of copper prices]

While everyone agrees that China’s reopening is “unequivocally positive for copper”, to quote Capital Economics, many appear to share the research house’s caution around the likely strength of the demand rebound.

The world’s biggest metals consumer still faces problems reinvigorating a moribund property sector and the impact on exports of slower growth in the rest of the world.

“We believe that the early January direction is correct but that the timing is slightly off,” said Saxo Bank, which is expecting improving Chinese demand to kick in only from the second quarter.

China’s recovery momentum and growing “green” demand from solar panels, wind farms and electric vehicles are seen helping copper rise further to $9,200 per tonne in 2024.

Mitigating against higher prices is an expected lift in mine production which will keep the global market in a 379,000-tonne supply surplus over 2023 and 2024.

Supply recovery

Indeed, recovering supply is likely to be just as significant to metals pricing as recovering Chinese demand this year.

Only zinc is expected to be in supply deficit this year and that to the modest tune of 19,500 tonnes, according to the median forecast of 12 analysts.

Analysts are expecting the market to swing back to a 123,000-tonne supply surplus in 2024, with the LME average cash price expected to decline to $3,042 per tonne from $3,484 in 2022.

Lead is similarly out of favour with analysts, the average LME cash price forecast to slide from $2,153 per tonne in 2022 to $2,040 in 2024 under the weight of a cumulative 183,000-tonne surplus this year and next.

Nickel is expected to see an even bigger cumulative surplus of 216,000 tonnes over the same period, reflecting the massive build-out of production capacity in Indonesia.

It’s therefore no surprise that analysts are looking for significantly lower nickel prices, with a median forecast of $24,000 per tonne this year and $22,000 in 2024, compared with Tuesday’s cash settlement of $29,400.

Aluminum is viewed as more finely balanced, with a median forecast supply surplus of 80,535 tonnes this year and 92,100 tonnes in 2024.

These are small numbers in a 60-million-tonne global market-place, and seem to reflect wariness about the continued impact on smelter production of high power pricing in Europe and sporadic rounds of power rationing in Chinese provinces such as Yunnan.

Although the median forecast is for aluminum to fall to an average $2,488 per tonne this year, continued production-side constraints will underpin a recovery to $2,600 next year.

Perils of forecasting

Tin is a good reminder of the challenges of commodities forecasting, the LME tin price having registered both an all-time high of $51,000 per tonne and a two-year low of $17,350 over the course of 2022.

The median forecast is for tin to average $23,670 per tonne in 2023, a sharp fall from last year’s average price of $31,362 per tonne. But expectations among the 17 analysts contributing a tin forecast span a wide price spectrum between a high of $30,959 and a low of $19,014.

That said, last January’s median forecast proved surprisingly close to the mark at $34,880 in what was a year of extraordinary volatility.

Also close were the median calls on copper ($9,370 per tonne versus an actual $8,814) and zinc ($3,225 vs $3,484). A median lead forecast of $2,155.50 per tonne was almost spot on relative to last year’s actual average of $2,153.00.

The biggest collective miss last year was nickel, where a median price forecast of $19,921 per tonne fell far short of last year’s average price of $25,627.

But few could foresee the scale of market disruption that broke out in March, when a melt-up in the nickel price forced the LME to suspend trading for six days.

This time last year analysts were also in a wary mood after a blistering run-up in price over the back end of 2021. Their collective caution proved well founded as the base metals unwound most of those gains over the second half of 2022.

There’s a sense of deja vu about this year’s early price strength and the equal sense of caution in the latest analysts’ poll.

Whether they will be right for the second year running remains to be seen.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Jan Harvey)

More News

Contract worker dies at Rio Tinto mine in Guinea

Last August, a contract worker died in an incident at the same mine.

February 15, 2026 | 09:20 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments