Column: Aluminum’s fortunes tied to Yunnan weather forecast

Global primary aluminum production grew by 2.0% year-on-year to 16.9 million tonnes in the first three months of 2023, according to the latest monthly assessment from the International Aluminium Institute (IAI).

The headline growth figure flatters to deceive.

Production outside of China is flat-lining, with restarts and curtailments largely cancelling each other out.

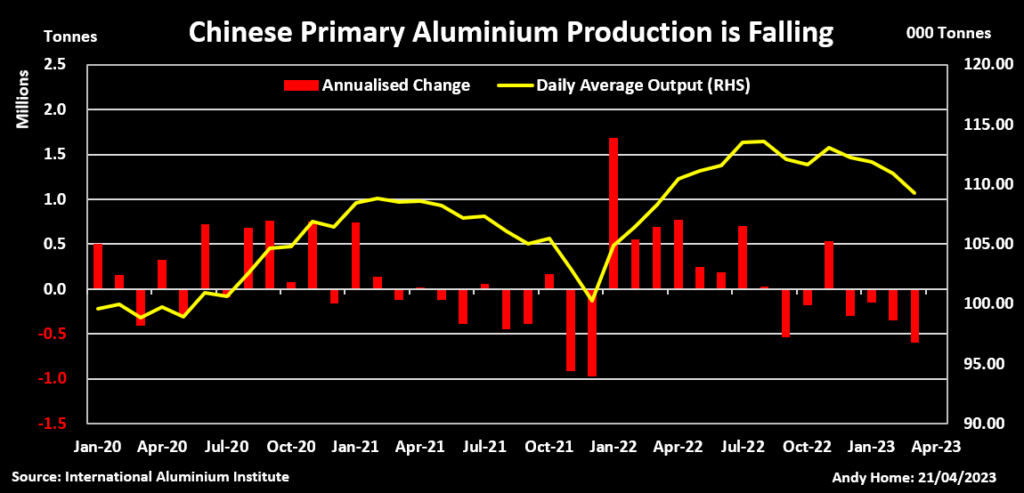

China, which accounts for just under 60% of the world’s primary metal production, lifted output by 3.9% relative to the first quarter of 2022, but the growth rate slowed sharply to just 0.9% in March.

Expressed in terms of annualized run-rates, China’s output of 39.9 million tonnes last month was the lowest in a year and down by 1.6 million tonnes from August’s record 41.5 million.

New and restarted capacity is failing to offset lower production in the hydro-rich province of Yunnan, where power-hungry smelters have been ordered to reduce operations to help cope with a severe drought.

China’s aluminum production is now highly dependent on weather patterns in the south of the country. So too is the global aluminum market.

Praying for rain

Yunnan province accounts for around 12% of China’s aluminium capacity and produced 4.2 million tonnes in 2022.

It has been a fast-growing production hub as Chinese operators have migrated from coal-powered provinces in a quest to produce low-carbon “green” aluminum using hydro energy.

Hydro power, however, requires rainfall and Yunnan is experiencing its worst drought in decades.

The provincial capital Kunming, which has received only 10% of its normal precipitation so far this year, earlier this week issued an orange drought alert, the second most severe warning in a four-tiered system. Many other towns have done the same, according to China Daily.

Industrial energy users, including aluminum smelters, have been instructed to reduce operations to balance the power system.

Around two million tonnes of the province’s production capacity is now off-line, according to Li Jiahui, an analyst at consultancy Shanghai Metals Market, speaking at a conference in Zhengzhou.

While other provinces have restarted capacity or even brought on new electrolysis lines, the impact has failed to offset the losses in Yunnan.

In theory things will turn around with the approaching rainy season, but in practice it will depend on just how much rain falls and whether there will be sufficient guaranteed power to allow smelters to commit to the costs of reactivating idled capacity.

Western production flat-lines

Primary aluminum production outside of China was flat year-on-year in the first quarter.

Only two regions registered significant changes relative to the first three months of 2022.

Latin American production surged by 24% thanks to the ramp-up of the Alumar smelter in Brazil, which is being restarted after six years of care and maintenance, and the return to full operations of the Aluar plant in Argentina.

However, the region is a relatively small producer and even with the stellar growth rate accounted for just 5% of non-Chinese production in the first quarter.

At the other end of the spectrum lies Western Europe, where first-quarter production was down by 10% on last year.

High energy prices have forced multiple smelters to idle capacity over the last year, and annualised run-rates in the region have fallen to multi-year lows of 2.7 million tonnes.

Output appears to be bottoming out, with no new announcements of curtailments and Norwegian producer Hydro negotiating a last-minute deal to avoid a potentially protracted strike at two of its smelters.

Next year will see the return of the San Ciprian smelter in Spain, which Alcoa will restart after two years of idling with new renewable power agreements.

Others may also reactivate curtailed capacity if power prices hold their lower levels after spiking in the wake of Russia’s invasion of Ukraine.

Weather watch

However, China’s dominant position in the global aluminum picture means that it holds the key to future production patterns.

And the key variable within China is Yunnan, which can churn out as much metal as all the smelters in North and Latin America combined.

Both the global supply chain and the aluminum price are becoming ever more dependent on rainfall patterns in southern China.

Seasonality is a new source of volatility for a metal that was previously defined by the predictable nature of the continuous aluminum smelter process.

Aluminum’s green energy-transition ambitions come with a big green production caveat.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Jan Harvey)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments