China’s low copper inventory data belie sufficient supply

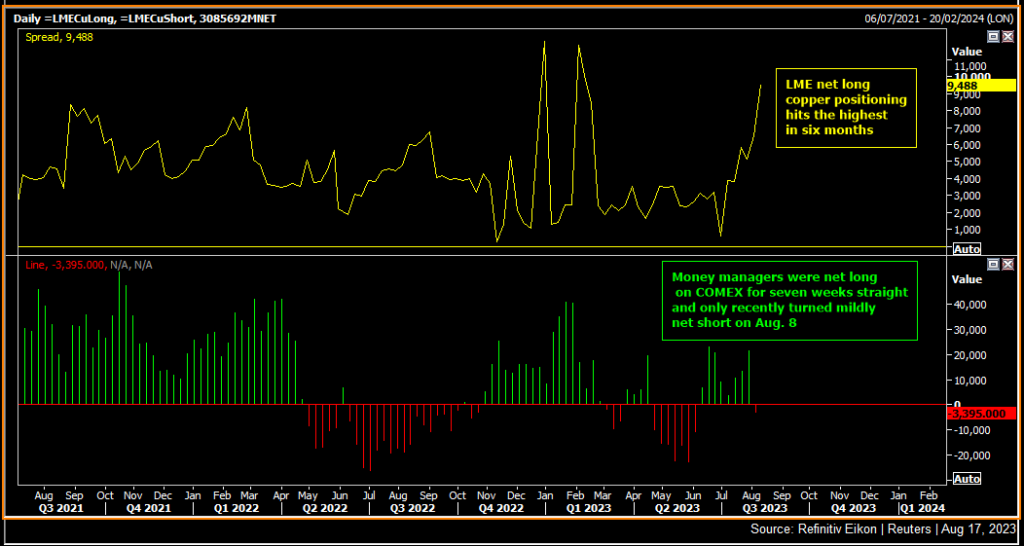

Net long positions of copper on the London Metals Exchange (LME) are at a six-month high, partly fuelled by low Chinese copper inventories data, but industry sources say this signal often as seen as bullish isn’t reflecting the reality on the ground.

China is the world’s top copper consumer, and combined inventory in the Shanghai Futures Exchange and Chinese bonded warehouses were 110,314 metric tonnes on Aug. 11, down 53% year-on-year and equivalent to just under three days of consumption.

While futures prices in London and Shanghai have fallen to multi-week lows, some investors have been building long positions, based on LME data, in anticipation that prices will turn higher in coming months because China’s inventories are so low, and on hopes the Chinese government will roll out more aggressive economic stimulus measures.

The total net long position in LME copper rose to 9,488 contracts on Aug. 11, the highest since Feb. 10, data provided in the Commitments of Traders Report showed.

“With such limited inventory cover in China and on Western exchanges, we see significant right-tail risk to the copper price if, for example, there was a material supply disruption or upside surprise in China policy support announcements,” Goldman Sachs said in a report dated Aug. 11.

“Indeed, our dialogue with the investment community so far in Q3 suggests interest in copper downside has now dissipated and buying copper dips is the predominant strategy.”

Traders and manufacturers, however, say there is enough readily available copper, and with demand hurt by a slowing economy, supply might not become tight anytime soon. In addition, the indicator may be particularly misleading now because more copper is now traded outside of the futures exchanges and directly between counterparties.

“Copper stock data is no longer important for us to assess market supply and demand,” said Zhang Kaimin, a purchasing manager at Hubei Shidai Refined Copper Technology, a copper rod maker that uses around 10,000 tonnes of refined copper a month.

“Spot supply is plentiful in the market and it is easy to source material as long as you pay a good price,” said Zhang, who booked some cargoes in early August.

Chinese copper stocks readily available in the spot market, which includes stocks in warehouses of the Shanghai Futures Exchange, totalled 82,600 tonnes on Aug. 14, up 17.5% year-on-year, according to information provider SMM.

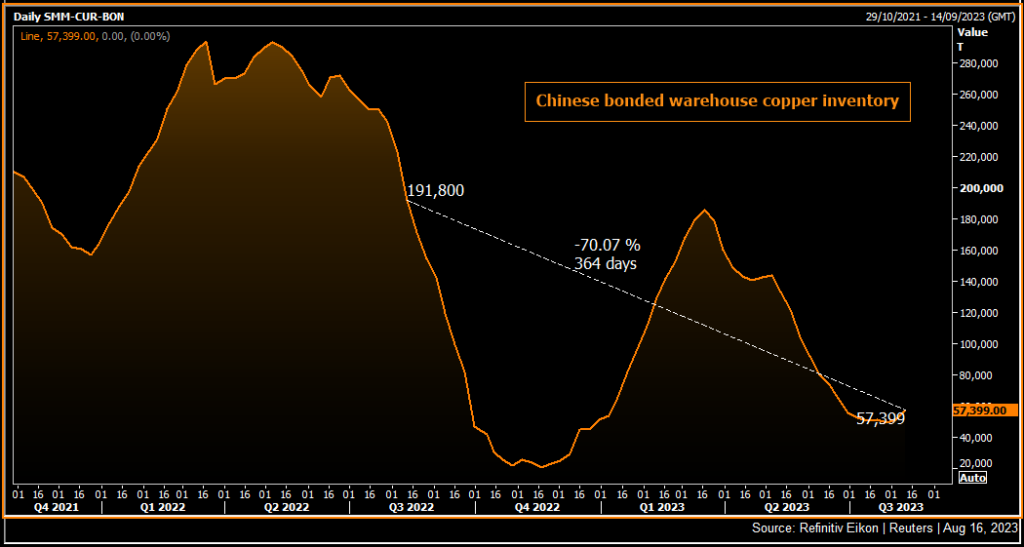

However, Chinese bonded warehouse inventory, at 57,399 tonnes on Aug. 11, was down 70% from the same time last year, SMM data showed.

Higher US dollar financing cost, the exit of once copper trading giant Maike Group, and the troubled Chinese property sector all contributed to lower bonded inventory, said CRU analyst He Tianyu.

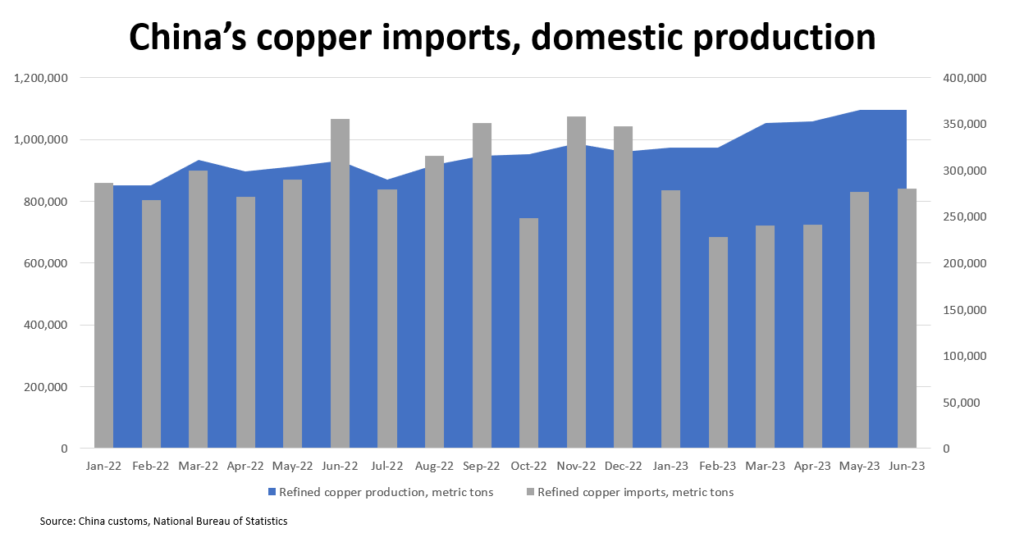

Record high production by Chinese smelters lifting operation rates and expanding capacity also made up for the 12.7% year-on-year fall in refined imports in January-June.

China consumes more than half of the world’s refined copper, and demand usually peaks during the September-October autumn months as the property and manufacturing sectors ramp up.

This year, the outlook for both sectors is subdued in the slowing economy, which means the traditional uptick in demand during these three months might not be as robust.

“Demand overall is subdued and copper exports are extremely sluggish,” said a Guangzhou-based copper product maker.

Inventories also fell because many Chinese smelters recently invested more into manufacturing value-added products using some of their own refined metal, reducing the need to send supplies into warehouses, said a copper tube maker.

There is also more direct delivery between smelters and consumers, said the person, who declined to be named as they were not authorized to speak to the media.

“Low inventory is basically a normal market… and the market liquidity is not as good as before,” said another source at a copper smelter.

Still, strong consumption from sectors including electric vehicles, solar and wind continue to support demand, analysts said, but the overall economic gloom must first lift for any significant pick up.

“The biggest risk will arise from China being unable to stimulate growth significantly in the country from current levels,” said StoneX analyst Natalie Scott-Gray, forecasting an average LME copper price in 2023 at $8,748 per tonnes.

(By Mai Nguyen and Siyi Liu; Editing by Miral Fahmy)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments