China EV, battery makers grapple with graphite squeeze

As they scour the globe for the lithium, nickel and cobalt resources needed to keep China on top in the electric vehicle (EV) stakes, Chinese battery and EV makers are fretting about supply of another mineral closer to home – graphite.

Graphite, in both natural and synthetic forms, is used for the negative end of a lithium-ion battery, known as the anode. Around 70% of all graphite comes from China, and there are few viable alternatives for batteries.

Chinese producers have their work cut out keeping up with global demand for graphite, which has surged along with rapid growth in the battery market in recent years.

Consultancy Benchmark Mineral Intelligence (BMI) sees a roughly 20,000 tonne graphite deficit in 2022, versus a similar-sized surplus last year. About 20,000 tonnes of graphite is enough to make batteries for roughly 250,000 EVs, an industrial source said.

Top global EV battery maker Contemporary Amperex Technology Co Ltd (CATL) is “desperate” to secure supply of key ingredients such as graphite to keep up with rising orders, said a person with knowledge of the matter.

“There’s not enough graphite in the market for domestic players to grab,” said the source, who asked not to be identified because the person was not authorised to speak to the media.

“Demand from clients such as Tesla (TSLA.O) is growing rapidly while supply of raw materials has been extremely tight,” the source said, adding that the recent power rationing on industry had exacerbated the situation.

CATL did not respond to Reuters’ request for comment.

Severe shortage

The upcoming Winter Olympics in Beijing is set to make supply of the dark grey form of carbon even tighter as authorities look to ensure a blue-sky backdrop to the showpiece event by ordering energy-intensive and high emitting industries like graphite to slash output, said a source with Chinese EV maker NIO Inc (NIO.N), with knowledge of the graphite market.

“Graphite is in severe shortage and all companies are snapping up purchases,” said the source, who also declined to be named as he is not authorised to speak to the media.

George Miller, an analyst with BMI said Northeast China’s graphite mines tend to close during the winter months due to extreme cold temperatures, leaving graphite processors no option but to try and fulfil orders from inventory.

“Graphite consumers, whether within China or outside, are fighting over a limited stock of material,” he said.

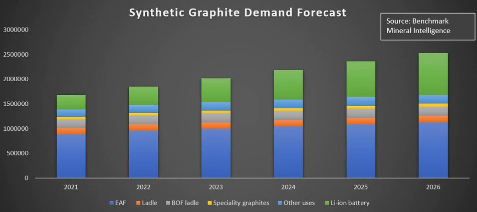

BMI forecasts that global demand for battery anodes will grow by an average of around 27% per year over the next decade, driven by the lithium-ion sector.

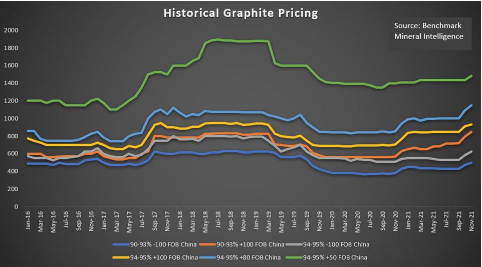

Anode-grade graphite flake prices on the Chinese domestic market are up almost 40% year-to-date at 4,500 yuan ($707) per tonne, testing the record highs seen in 2018, according to BMI.

Reflecting the rapid growth in the EV market, China’s auto sector sold 2.99 million EVs and plug-in hybrids in the first 11 months of 2021, a 170% rise on the same period in 2020.

Tesla, the world’s most valuable EV maker, registered its support for U.S. Section 301 tariff waivers on imports of both artificial and natural graphite from China to be reinstated as many tariff exclusions expired.

“Tesla has concluded that no company in the United States is currently capable of producing … graphite to the required specifications and capacity needed for Tesla’s production,” the company said in a public comment lodged with the U.S. Trade Representative recently.

CATL is studying using the natural form of graphite in battery anodes as an alternative to artificial graphite because of greater availability, said the first source, even though it may not give the same level of performance.

“We have heard indications that Chinese anode producers are shifting their anode blends towards a higher percentage of natural feedstock,” Miller said.

($1 = 6.3630 Chinese yuan)

(By Zhang Yan and Tom Daly; Editing by Gavin Maguire and Ana Nicolaci da Costa)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments