China cobalt buyers use global glut to challenge pricing

China’s battery industry has seized on a glut in the global cobalt market to push through a change in the way the commodity is priced.

A rapid expansion of cobalt mining in Democratic Republic of Congo and Indonesia has output racing ahead of demand, dragging down global prices. It’s also prompted a push by squeezed Chinese refineries to win changes in how cobalt is bought and sold.

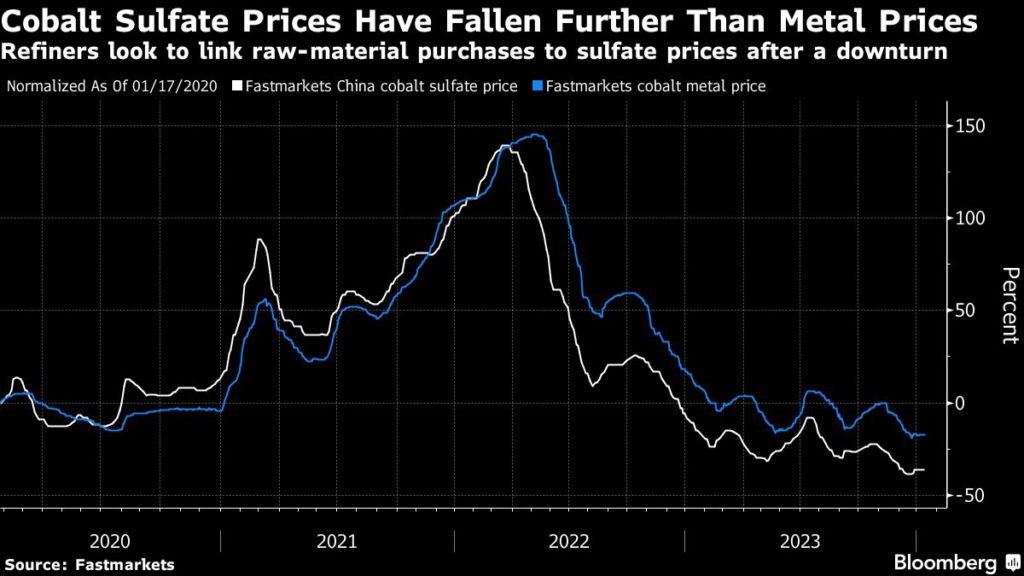

Top producers CMOC Group Ltd. and Eurasian Resources Group have agreed to sell more of their material against the local Chinese price of cobalt sulphate, the chemical form used in batteries, according to people familiar with the matter. That’s a shift from pricing against refined cobalt metal that has been typical for decades.

The switch is only partial so far, and has been resisted by one major supplier, Glencore Plc, said the people, asking not to be identified discussing a private matter. But the pricing change is one among many upheavals triggered by the boom-to-bust slump across the battery materials sector in the past year.

“Refiners would prefer sulphate pricing, and the glut of material reaching the market means that they are in the driving seat,” said Thomas Matthews, battery metals analyst at CRU Group in London said. Pricing against the chemical will be the norm at least for the coming five years, he said.

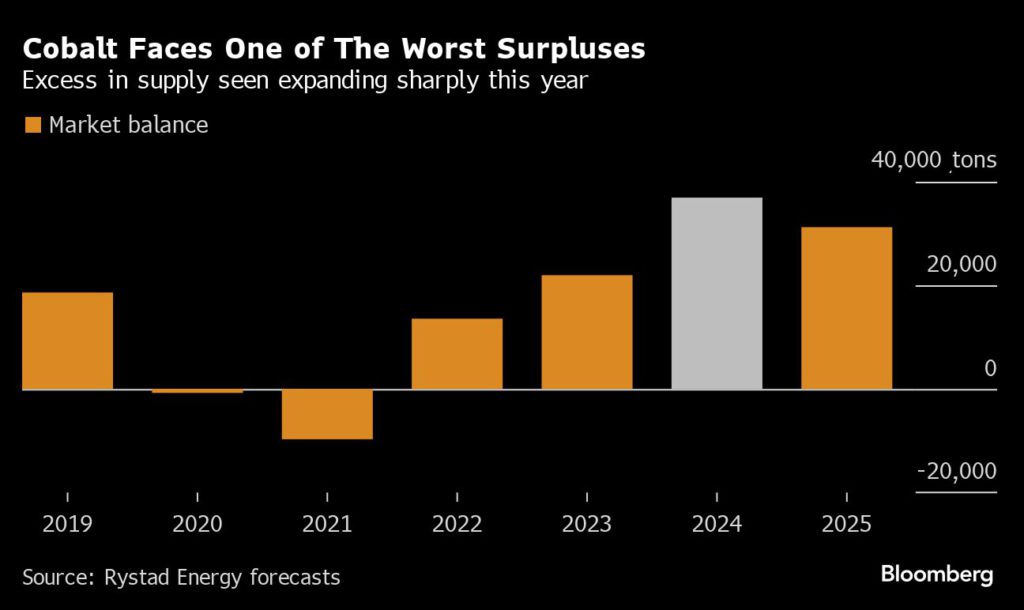

Cobalt prices slumped about 30% last year, and the price of cobalt sulphate in China sank to its lowest since at least 2010 in December, according to Shanghai Metals Market. Consultancy Rystad Energy forecasts one of the biggest-ever worldwide surpluses in 2024.

Off exchange

Like many niche commodities, cobalt supply contracts are often fixed against spot prices assessed by third-party agencies. Miners typically sell hydroxide for sulphate production at a percentage of the global metal price published by Fastmarkets, a UK company.

But the Chinese refineries are now referencing cobalt sulphate prices from domestic agency Shanghai Metals Markets, taking advantage of a period of plentiful supply to seek prices which, they say, better reflect an expanding and China-centric battery supply chain.

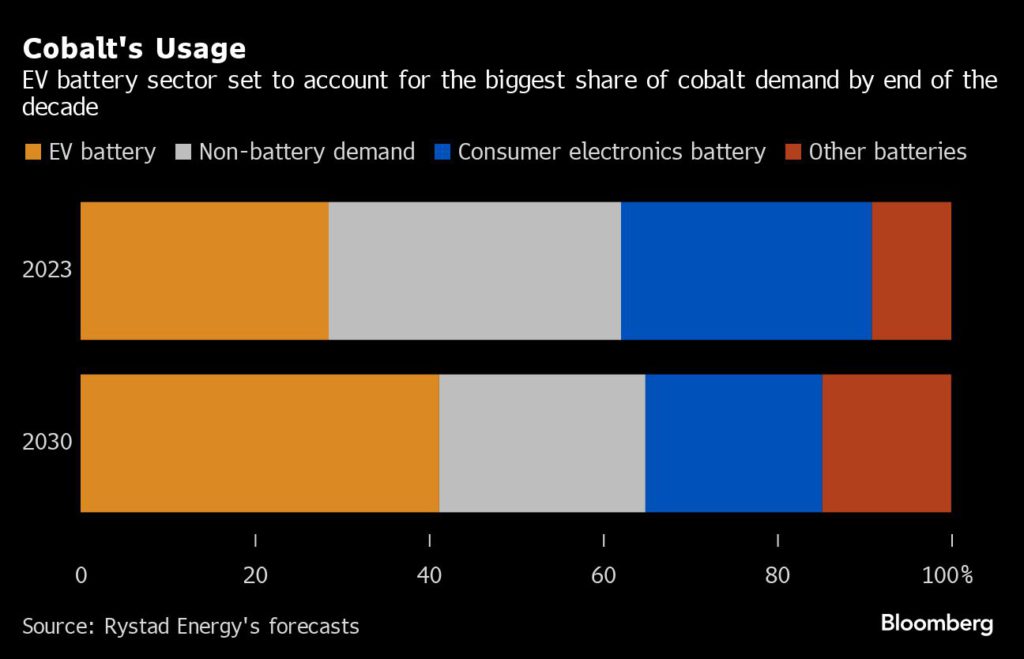

Rystad says EV batteries will account for 41% of cobalt demand by 2030, up from 28% last year. That comes despite a shift to battery chemistries that don’t require cobalt.

Chinese industries have long pushed for greater pricing power across a range of commodities from iron ore to crude oil and now battery materials. A lithium futures contract was launched last year, while Russia’s largest nickel miner was said to sell some of its metal in yuan at prices set in Shanghai.

CMOC, which is Chinese, plus Glencore and ERG are the world’s top three cobalt miners, and together account for more than half of global production, according to Rystad.

Glencore is resisting sulphate pricing in negotiations because it has less control over the end-product market in China, and a link to the chemical pricing could amplify its exposure to a downturn in prices or demand, the people familiar with the matter said.

In response to Bloomberg’s query, a CMOC representative said the company is referencing various formulas in its sales contracts, including cobalt metal and payables, hydroxide quotes and cobalt salt products. ERG didn’t respond to requests for comment, while Glencore declined to comment.

Collapse

Lithium and nickel also plunged along with cobalt in 2023 as supply expanded, China’s booming EV industry dialed down its breakneck pace of growth. The price slump has wreaked havoc, with new projects stalling, inventories ballooning and investor interest on the wane.

Oversupply is a particular problem for cobalt because it emerges almost entirely as a by-product of making copper or nickel. Indonesia’s booming nickel mines have already transformed the Southeast Asian nation into the world’s second-biggest cobalt producer after DRC. In the African nation, a major new source of cobalt is CMOC’s Kisanfu copper project.

So despite price volatility and a growing surplus, there’s unlikely to be any major mine shutdowns or targeted efforts to rein in cobalt production, according to Rystad Energy’s analyst Susan Zou.

“As long as the price of copper stays at decent levels, there will still be appetite for mining activity,” Zou added. “Gains in copper are still likely to offset some losses in cobalt.”

(By Annie Lee, William Clowes and Jack Farchy)

Read More: Most cobalt producers loss-making after 2023 price slump, says ERG

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Godlove Godfrey saitoti

I have a mined cobalt,am looking for a buyer