Bulls run wild: Chinese funds throw more fuel on copper’s flames

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

Copper punched through the $9,000-per tonne level last week for the first time since 2011, with a red-hot rally showing no signs of abating.

The London Metal Exchange (LME) three-month copper price reached $9,617 per tonne on Thursday, within sight of the all-time high of $10,190 recorded almost exactly 10 years ago.

While the copper market has risen for 11 consecutive months fuelled by China’s physical buying and the narrative of a metals-heavy global green recovery, Chinese funds stepped into the driving seat last week with one player placing a mega $1-billion bet on higher prices.

Investors outside of China appear more equivocal, with fresh money entering the market even as other funds start taking profits. Few, though, seem prepared to risk going short even as wariness grows that copper’s one-way bull run is overdue a correction.

A major deterrent to doing so is an emerging squeeze on the London market, where official stocks are low and time-spreads are tightening.

China bull

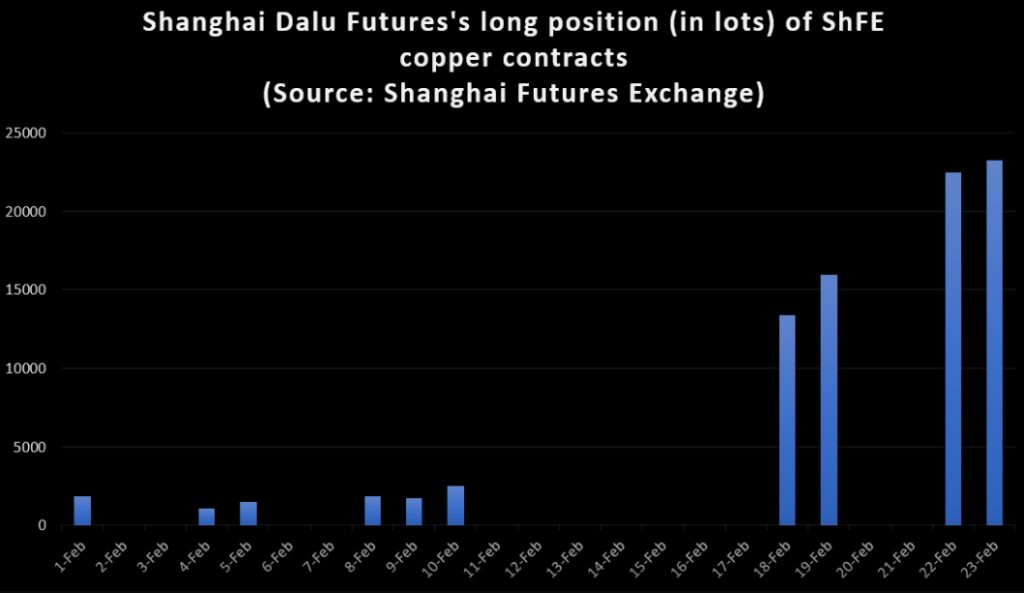

It’s clear that someone in China decided to celebrate the Year of the Ox by going long copper.

Broker Shanghai Dalu Futures jumped to the top of the bull rankings on the Shanghai Futures Exchange (ShFE) copper contract when the market reopened after the lunar new year holiday.

As of last Friday the firm, controlled by Zhongshan Securities Co Ltd, held a long position equivalent to almost 120,000 tonnes across the April-July contracts, according to Refinitiv data.

It also held another 20,000 tonnes of long positions on the Shanghai International Energy Exchange’s (INE) international copper contract.

The Shanghai Futures Exchange only details long and short positions on contracts above a certain level of open interest, meaning the position could be bigger still if it’s spread across less liquid months.

The ultimate identity of the big Shanghai copper long is a source of much speculation in the market with many drawing comparisons with another mega bull play channelled through Gelin Dahua Futures in 2018.

Dalu has also rapidly built up positions on the ShFE’s aluminium contract, suggesting a broader play on the industrial metals narrative.

The mystery buyer, however, is only the most prominent part of a bigger speculative crowd surge into the Shanghai copper market.

Market open interest on the ShFE contract mushroomed from 277,000 contracts to a one-year high of 378,401 over the course of February, coinciding with the latest leg of the price rally. Volumes soared to levels last seen in 2015, suggesting a retail investor stampede to get a piece of the copper action.

Funds build LME, cut CME positions

While bulls run wild in Shanghai, the investment picture outside China is more nuanced.

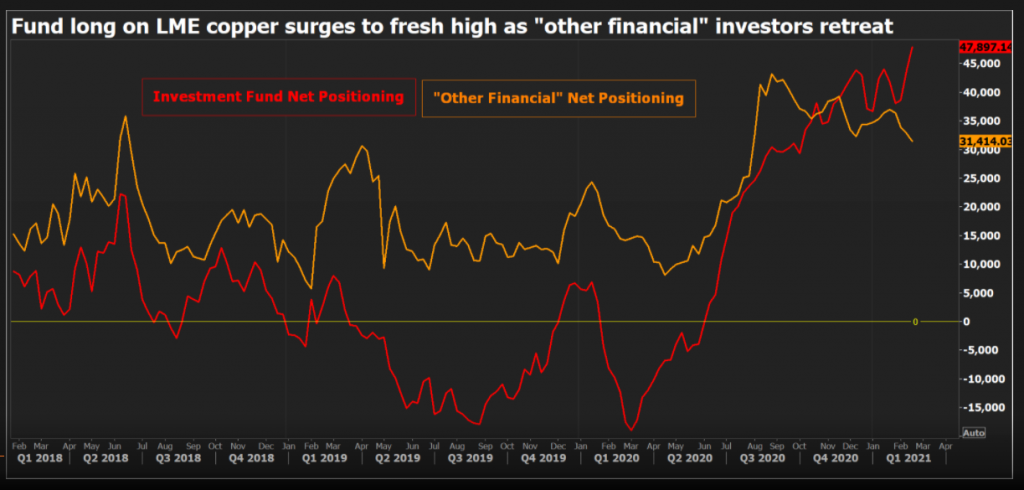

The investment fund net long position on the LME has risen to 47,897 contracts, the highest level since the exchange started publishing the Commitments of Traders Report in its current format at the start of 2018, while LME broker Marex Spectron estimates the speculative net long in the London market reached 62% of open interest last Thursday, a level not seen since 2004, when it peaked at 75%.

However, it’s not all one-way traffic.

Chinese investors may have propelled the latest leg of this rally but market optics in Shanghai are changing

The long position held by the LME’s “other financial” category, which captures insurance and pension flows, has been in steady retreat since its October 2020 peak of 43,212 contracts, falling further to 31,414 contracts last week.

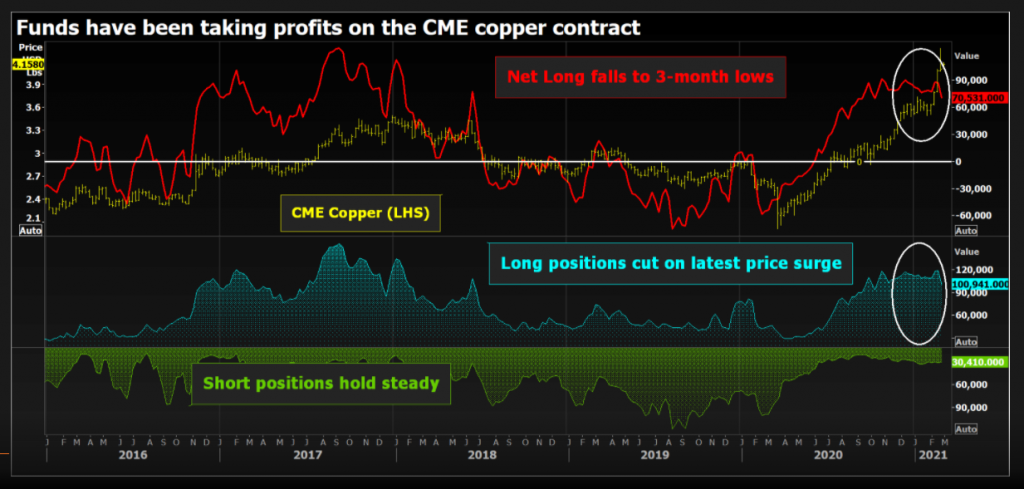

Also in retreat are fund bulls on the CME copper contract.

The money manager net long slipped from 87,312 to 70,531 contracts in the week to last Tuesday (Feb. 23) even as the price moved higher.

The reduction appeared to be classic profit-taking with outright long positions falling and outright short positions holding steady at their recent low levels.

Caution about the potential for a price correction after copper’s relentless upward march is currently being expressed via the purchase of put options with few prepared to risk an outright short position.

London squeeze

The collective reluctance to stand in the way of a fast-moving bull train is being reinforced by an emerging squeeze in the LME copper market.

Being short in a volatile and tightening market is a scary prospect for even the most adventurous funds.

The benchmark LME cash-to-three-months time-spread closed last week valued at a backwardation of $62.25 per tonne, which is the tightest the period has traded since early 2019.

LME inventory is stubbornly low despite a widening cash price incentive to deliver metal onto LME warrant. LME stocks currently stand at 74,200 tonnes, down by 31,600 tonnes on the start of January. A steady trickle of arrivals has been more than offset by departures.

LME stocks, however, can often flatter to deceive and any further tightening will test the true level of availability.

As of last December there were another 134,000 tonnes of copper sitting in the LME’s off-warrant shadow zone. Most of it – 99,000 tonnes – was located at Rotterdam, where visible onto-warrant inflows have totalled just 3,325 tonnes so far in 2021.

Made in China

Chinese investors may have propelled the latest leg of this rally but market optics in Shanghai are changing.

ShFE registered inventory more than doubled over February to 147,958 tonnes, the highest tally since October last year.

Inventory always builds over the Chinese new year holidays but the effect this year is going to be accentuated by the new physically-deliverable INE copper contract.

Bonded stocks registered with the INE jumped from just 199 tonnes to 57,346 tonnes last week, although it’s unclear whether this was the result of new arrivals or existing inventory being registered with the exchange.

Either way, this new component of the global stocks picture reinforces the sense that China’s supply chain is starting to refill after last year’s stellar imports.

Rising Chinese stocks will be a test of the big long operating through Dalu Futures. Everyone remembers the last time a Chinese fund took this size a position. The Gelin Dahua bet didn’t end well for the fund or the copper price.

(Editing by Kirsten Donovan)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments