Bonds’ decades-long lead over gold vanishes as debt worries grow

For much of the past half century, US Treasuries have handily outpaced gold as a buy-and-hold investment. Now, bonds’ status as the ultimate haven is facing one of its biggest challenges yet.

Investors traditionally flocked to US debt as a super-safe investment paying steady income, and backed by the world’s economic powerhouse. For buyers ranging from individual savers to sovereign nations, these attributes made it a superior investment to gold, which doesn’t generate cash flows as bonds do, though it is still coveted as a scarce commodity and inflation hedge.

This relationship has been shifting lately, with recent trends moving in gold’s favor. The benchmark Bloomberg Treasury Total Return Index is on track for its third annual decline in four years, extending its loss from a peak in 2020 to 11%. In comparison, gold set a fresh record this week to clock in a 15% return so far this year alone.

To Kristina Hooper, chief global market strategist at Invesco, the divergence of the two traditional havens signals investors’ heightened angst about skyrocketing government debt and their preference for physical assets.

“The safe haven asset class of choice has become gold rather than Treasuries,” said Hooper. “The bigger theme is just the concern about a lot of debt and concern that the fiscal situation in the United States is unsustainable.”

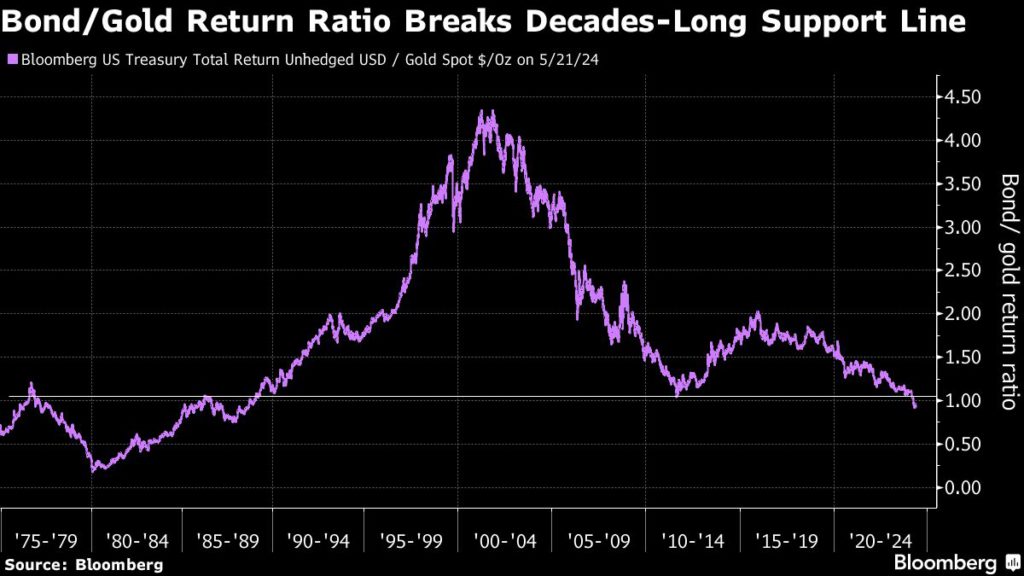

The diverging performance means gold has jumped ahead of US government debt as a long-term investment. A dollar invested in gold 51 years ago is now worth $2,314, $172 more than the return pegged to the Bloomberg Treasury index, which had its debut in 1973. (The comparison doesn’t factor in the storage costs for holding gold.)

In many ways, bonds’ recent struggles are easy to understand. They stem largely from the Federal Reserve’s aggressive monetary tightening campaign since 2022, which drove up yields from a record low and hammered bond prices.

It is the surge in gold that is harder to decipher. In theory, rising “real” interest rates — those adjusted for inflation — should dim the shine of the precious metal, making an asset that doesn’t yield anything less appealing. And yet gold has marched higher.

Analysts point to central banks’ purchases as a major force propelling gold’s surge. China, for instance, has topped up its gold holdings for 18 consecutive months, while scaling back its stockpile of US Treasuries.

At the same time, deep-seated concerns around mounting US debt and deficits have raised broader credit worries. The growth of US public debt has accelerated since the pandemic and almost doubled over the past decade to about $35 trillion.

Of course, bonds’ performance relative to gold has varied over the decades, lagging for certain points in time only to lead again. And gold’s outperformance typically comes with higher volatility. The yellow metal surged in the late 1970s, for instance, as investors sought inflation hedges.

Bonds started to catch up after Paul Volcker’s campaign to cool inflation in the 1980s jump-started a four-decade bull run for the fixed-income market. US 10-year yields tumbled to as low as 0.3% in 2020, from almost 16% in 1981, handing investors a windfall as bond prices appreciated. But the low yields helped sow the seeds for the losses since then, including an unprecedented decline of 12% in 2022, as the Fed jacked up interest rates to curb inflation.

To Julian Brigden, co-founder of Macro Intelligence 2 Partners, the bond’s current underperformance is more than transitory because an aging population and a shrinking pool of savings means there isn’t enough demand to meet the ever-increasing debt supply.

“We are in a structural bond bear market,” said Brigden, who advises clients, including hedge funds. “Bonds are not a good hedge. Gold is taking over.”

(By Ye Xie and Yvonne Yue Li)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments