Billionaire Anil Agarwal’s Anglo American trade a gold mine

Indian billionaire Anil Agarwal may be calling off his charge at Anglo American Plc – but he, his adviser JPMorgan Chase & Co., and the hedge funds that financed him can at least console themselves with the profits they made. The only people who were exposed to any real risk in the adventure look to have been Anglo’s shareholders.

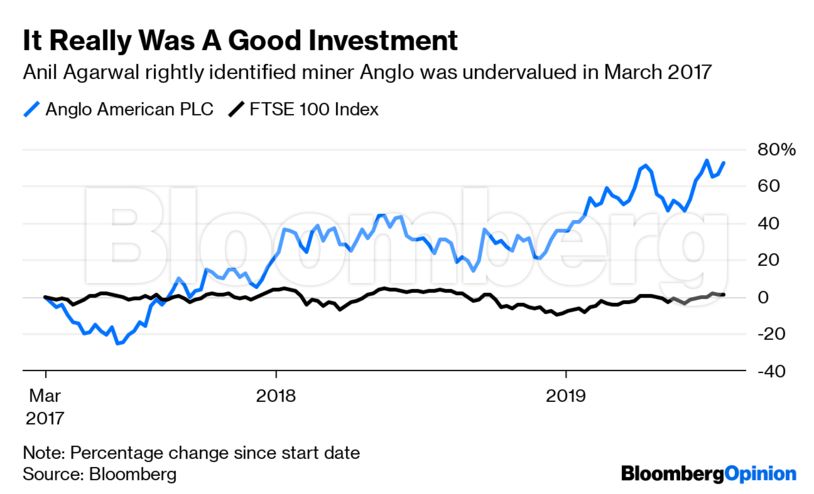

Agarwal acquired a roughly 20% stake in 2017, shelling out barely any cash himself

Agarwal acquired a roughly 20% stake in 2017, shelling out barely any cash himself. The shares were acquired almost entirely from hedge funds who had borrowed them from other investors, with JPMorgan acting as broker. In return, the funds received an unusual bond issued by the billionaire’s investment vehicle, which would be repaid in the Anglo shares he had acquired. Notably, the structure limited the tycoon’s exposure to the ups and downs of Anglo’s share price.

Both sides have done well out of this. First, Agarwal. He has had to pay roughly 420 million pounds ($521 million) of coupons on the bonds. If his Anglo shares went up a lot – as they did – the terms allowed him to keep nearly 10% of his holding on redemption, which was announced on Thursday. On Friday, he sold that residual holding for almost 520 million pounds.

His 100 million-pound profit looks to be a 24% gain. But the internal rate of return will be much higher because he didn’t have to shell out of those coupons on day one.

The hedge funds weren’t taking much risk either. Having borrowed Anglo shares and sold them to Agarwal, their profit came from the coupon. The Anglo shares received on redemption would – broadly – cover their short position in the miner’s stock. Like the billionaire, the hedge funds would have put down very little capital in the trade. Their main risk was that the coupons wouldn’t get paid. But it would have astonishing if Agarwal had defaulted.

JPMorgan’s fees aren’t clear. But the huge amount of ancillary banking activity here – effectively the stage management of the whole operation – is a fee in itself.

That leaves Anglo’s rank-and-file shareholders. The stock price has risen 76% since Agarwal popped up, so they seem well-rewarded. Some of them will have also received fees for lending out their stock. But of all the protagonists they were the only ones with direct exposure to the share price.

What’s more, they have suffered a period of uncertainty when it was unclear what Agarwal, with his massive holding, really wanted. They will be relieved that the register is losing an unpredictable force. Their returns are the most deserved.

(By Chris Hughes)

More News

Contract worker dies at Rio Tinto mine in Guinea

Last August, a contract worker died in an incident at the same mine.

February 15, 2026 | 09:20 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments